Every call you take puts your truck, your driver, and your business on the line. A fender bender during a roadside pickup, a vehicle damaged on the hook, a driver injured on a dark highway shoulder without the right towing company insurance, any one of these moments can turn into a financial disaster.

This guide covers every coverage a towing business needs in 2026, what it actually costs, and the gaps most operators don’t find until after a claim is denied.

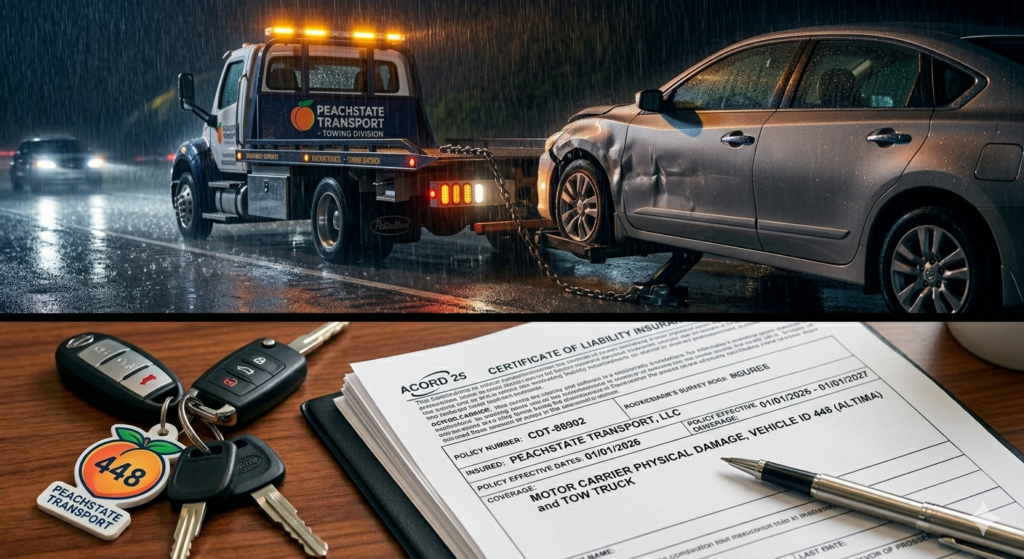

Standard commercial auto insurance was not built for towing. The moment you put another vehicle on your hook or underneath your wheel lift, you’ve taken on liability that a regular policy simply doesn’t cover.

Towing company insurance is a specialized product that accounts for:

Whether you’re running a single light-duty wrecker or managing a heavy-duty fleet, your coverage needs to match the work not just the truck. For a complete look at how commercial trucking policies are structured across vehicle types, visit our commercial trucking insurance page.

This is your foundation. Tow truck liability insurance covers bodily injury and property damage caused to third parties during towing operations. Most states require minimum limits, but clients, municipalities, and motor clubs typically demand $1,000,000 per occurrence or higher before awarding contracts.

This is the coverage most towing operators underestimate and the one that generates the most claims. On-hook coverage protects vehicles that are attached to your truck while in transit. If the towed vehicle is damaged during transport, your liability policy won’t cover it. On-hook insurance does.

Limits should reflect the highest-value vehicles you regularly tow. A $50,000 limit won’t cover a luxury vehicle or a commercial van.

When vehicles are stored at your facility impound lot, repair staging, overnight holding you’re responsible for them. Garage keepers liability covers damage to those vehicles from fire, theft, vandalism, or weather while in your care. Many towing operators skip this and absorb painful losses they didn’t expect.

Tow trucks are expensive. A light-duty wrecker starts around $60,000. A heavy-duty rotator can exceed $500,000. Tow truck physical damage coverage protects your equipment through:

If you offer roadside services jump starts, lockouts, tire changes, fuel delivery you need coverage that extends beyond just towing. Roadside assistance business insurance covers liability during these service calls, which carry their own unique risk profile separate from towing operations.

This is a content gap most towing insurance articles completely miss.

Light duty tow truck insurance covers standard passenger vehicles, motorcycles, and small commercial vans. Premiums are lower, liability exposure is moderate, and most policies follow standard commercial auto structures.

Heavy duty tow truck insurance is an entirely different category. Heavy rotators, underlift trucks, and recovery equipment handling semis, buses, and large commercial vehicles carry:

If you’re running mixed equipment tow trucks alongside dump trucks or flatbeds each vehicle type needs appropriate coverage. Our tri axle dump truck insurance and flatbed truck insurance guides explain how coverage differs across heavy commercial equipment types.

| Coverage Type | Estimated Annual Premium |

| Light duty liability only | $3,500 – $6,500 |

| Light duty full coverage | $7,000 – $12,000 |

| Heavy duty liability only | $6,000 – $11,000 |

| Heavy duty full coverage | $12,000 – $22,000+ |

| Fleet (3+ trucks) per unit | $5,500 – $9,500 |

| On-hook coverage (added) | $800 – $2,500 |

| Garage keepers (added) | $1,200 – $3,500 |

What raises your towing insurance premium:

What lowers your rate:

Q: What is on-hook towing insurance and do I need it? Yes. On-hook coverage protects vehicles attached to your truck during transport. Your liability policy does not cover them on-hook insurance does.

Q: How much liability coverage does a towing company need? Most motor clubs and municipal contracts require a minimum of $1,000,000 per occurrence. Heavy duty operators often need $2,000,000 or more.

Q: Is towing insurance more expensive than regular commercial auto? Yes typically 20–40% higher due to on-hook liability, roadside exposure, and the specialized nature of recovery operations.

Q: Does my policy cover damage to stored vehicles in my impound lot? Not without garage keepers liability coverage. Standard towing policies exclude vehicles in your care at your facility.

Q: Can I get towing company insurance as a new business? Yes. New towing businesses can get coverage, though rates will be higher in year one. A clean personal driving record and proper licensing helps significantly.

Running a towing business means taking on responsibility the moment you dispatch a truck. The right towing company insurance isn’t just about legal compliance it’s about making sure one bad night on the highway doesn’t take down everything you’ve built.

From single-truck operators to growing fleets, OLPolicy specializes in commercial towing coverage that actually fits how you work.

Call OL Policy at (866) 757-5350 today. Get a fast, no-pressure quote and find out exactly what coverage your towing business needs before you need it.