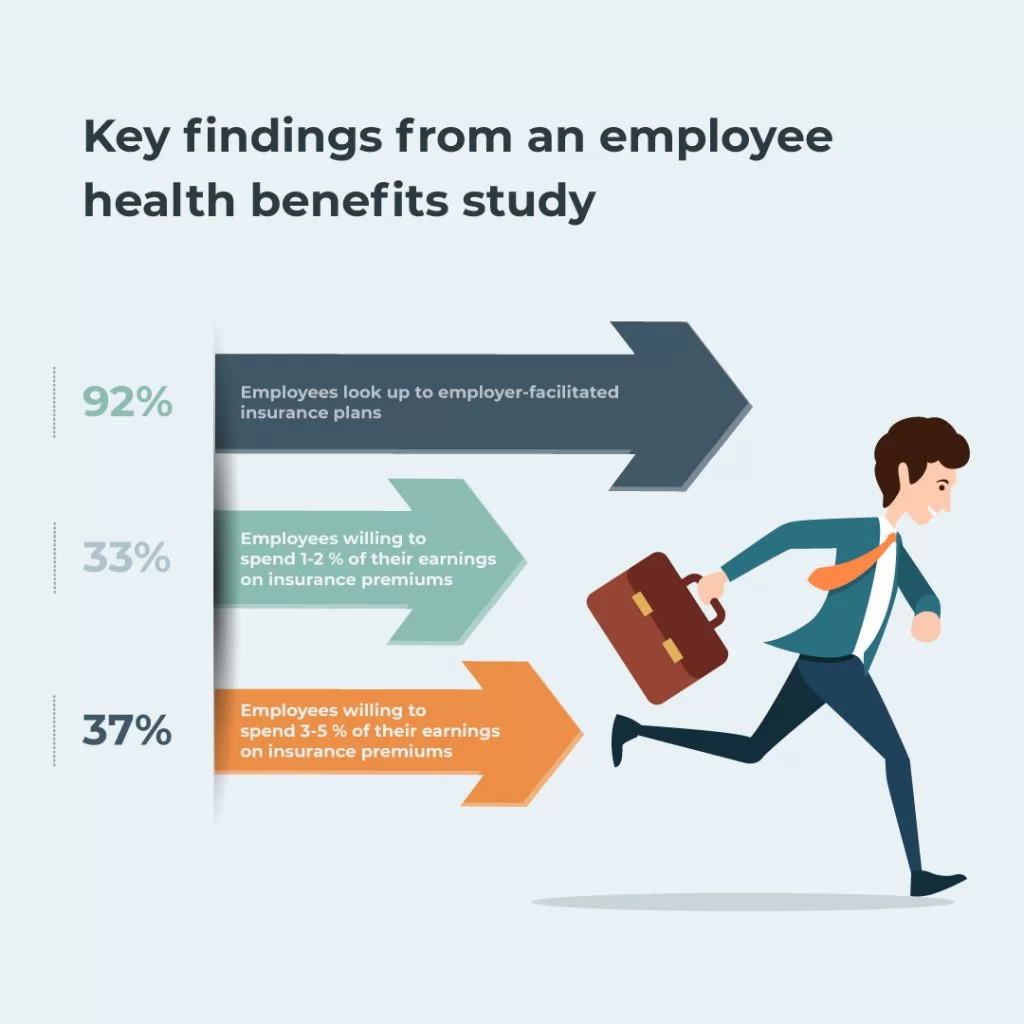

Group health insurance is a type of health coverage that employers offer to their employees, and sometimes to their employees' dependents as well. Instead of each employee buying an individual plan, the company provides one insurance plan that covers the entire group. This is a valuable benefit because it makes health insurance more affordable for everyone involved. The employer usually pays part of the premium, while the rest is shared among the employees. Group health insurance can cover a range of services, including medical expenses, prescription drugs, and in some cases, dental and vision care. For both the employer and the employees, group health insurance offers financial protection, helping to manage healthcare costs without facing huge out-of-pocket expenses.

At OlPolicy, we are committed to delivering comprehensive medical coverage with exceptional service. Our range of insurance options includes Individual and Group Health Insurance, Affordable Care Act (ACA) plans, Dental and Vision Insurance, Medicare Advantage and Supplement plans, as well as Whole Life and Term Life Insurance. We also provide Final Expense coverage, ensuring complete peace of mind for you and your loved ones.

There are many reasons why offering group health insurance is beneficial for employers. First and foremost, it can boost employee satisfaction and morale. When employees have access to good health benefits, they feel more secure and valued, which in turn can lead to higher job satisfaction and loyalty. This can help reduce turnover, as employees are more likely to stay with a company that provides health insurance compared to one that doesn’t. Additionally, group health insurance makes the business more attractive to potential employees. In today’s competitive job market, many workers look for companies that offer solid health benefits, so providing insurance can help attract top talent. From a financial perspective, offering group health insurance can also benefit employers by lowering payroll taxes and making the business eligible for tax deductions or credits.

Group health insurance provides significant advantages for employees, making it one of the most valued benefits in the workplace. One of the primary benefits is lower premiums. Since the employer typically covers a portion of the premium, employees pay much less for their health insurance than they would if they bought individual coverage. Group health plans also offer broader coverage, including not just medical care but often dental, vision, and prescription drugs. In many cases, these plans also cover pre-existing conditions from day one, ensuring that employees with ongoing health issues can get the care they need without delay. Another advantage of group health insurance is the simplified enrollment process. Compared to navigating the individual insurance marketplace, enrolling in a group plan is often faster and easier, saving employees time and reducing stress.

Although offering group health insurance may seem like a significant expense for employers, it can actually save money in the long run. One of the main ways it helps reduce costs is through tax benefits. Employers who provide health insurance can take advantage of tax deductions, and in some cases, small businesses may be eligible for tax credits. This reduces the overall cost of offering the benefit. Additionally, offering health insurance helps lower turnover rates. Employees are more likely to stay with a company that provides health benefits, which means employers spend less time and money recruiting and training new employees. Healthy employees are also more productive, so by offering health insurance, companies help ensure their workers can get the medical care they need to stay healthy. This reduces the number of sick days and boosts overall workplace efficiency. Finally, providing health insurance makes the company more attractive to skilled workers, reducing the time and costs associated with finding and hiring top talent.

Choosing the right group health insurance plan for your business can be a challenge, but focusing on a few key factors can make the decision easier. The first thing to consider is the healthcare needs of your employees. Conducting surveys or asking for feedback can help you understand whether your employees need more comprehensive medical, dental, or vision coverage. Next, it's important to stay within your company’s budget. While you want to offer a good plan, you also need to find one that balances cost and coverage. Comparing the costs of different plans and deciding how much of the premium the company will cover can help you find the right fit. Another factor to consider is whether to offer employees a single plan or multiple plan options, such as a choice between HMO and PPO plans. This allows employees to pick the plan that works best for them. Finally, make sure the plan you choose has a large enough network of doctors, hospitals, and specialists in the areas where your employees live, so they can easily access care. Taking these factors into account can help you select the group health insurance plan that best meets the needs of your business and your employees.