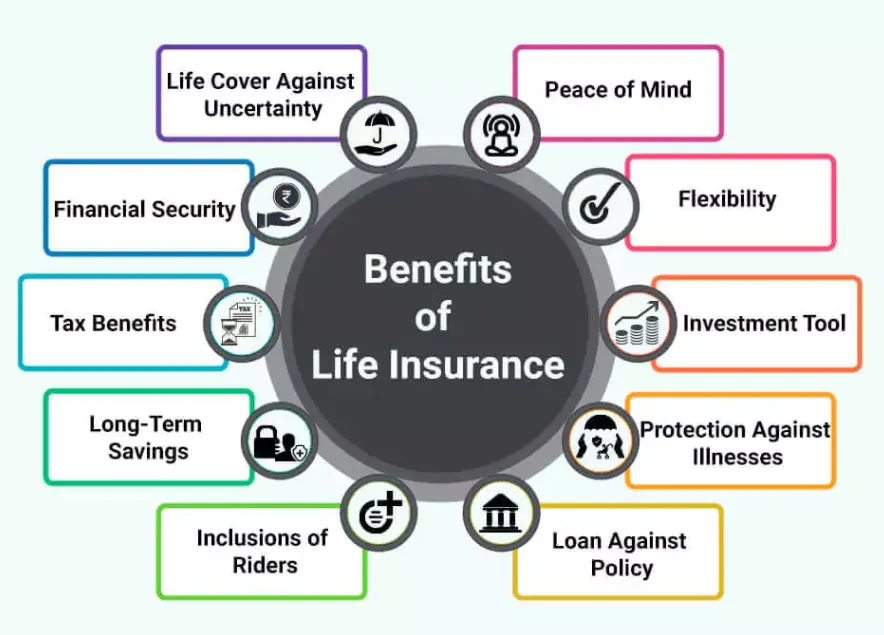

Term life insurance is a form of life insurance coverage that protects you for a defined length of time, commonly called the “term,” such as 10, 20, or 30 years. In contrast to whole life insurance, which can remain active for your entire life, term life insurance only provides a death benefit if the insured individual dies during the selected term. Because of this focused coverage, it is considered a clear and often budget-friendly choice for people who need protection for a temporary period. Term life insurance is widely chosen by individuals who want reassurance that their loved ones will have financial support during important stages, such as while children are growing up or when a home loan is still unpaid. After the term ends, the policy coverage stops unless the policyholder decides to renew it or change it into a permanent life insurance plan. If you want lifelong coverage, consider upgrading to our Whole Life Insurance which also builds cash value over time.

Term life insurance includes several important benefits, making it a sensible option for many households and individuals. One of the primary advantages is affordability. Since term life insurance offers protection for a limited duration and does not accumulate cash value like whole life insurance, the premium costs are typically lower. This allows people to obtain substantial coverage without paying high monthly amounts. Another valuable benefit is flexibility. Policyholders can select a term that aligns with their financial plans or current life phase. For instance, someone may choose a 20-year policy to keep their family protected until their children reach adulthood or until a mortgage balance is cleared. Term life insurance is also straightforward to understand.Seniors or those on a fixed income may also benefit from our Final Expense Insurance — a simple, low-cost plan covering funeral and burial costs.

Term life insurance depends on various conditions. Here are few examples:

Are you a student, just entering the job market or facing your first financial obligations? Then you need financial security for a certain period of time. Then you can apply for term life insurance.

If you are a new parent or expecting a first child, term life insurance will give you financial security.

If you are a new entrepreneur this time will help you achieve your goals through hard work and dedication. As a business owner, also protect your company with a Business Owners Policy (BOP) — covering your business liabilities while your term policy protects your family. Term life insurance can be taken for a short period of time after success.

Benefit from insurance protection supported by strong financial ratings and reinforced by a network of respected global reinsurance partners. Our solutions are created to meet the demands of the modern transportation industry, helping your fleet remain protected in an environment that constantly evolves. With dependable coverage in place, you can focus on operations while minimizing unexpected risks that could disrupt your business.

Our experienced professionals specialize in underwriting, claims assistance and fleet support, bringing valuable industry knowledge to every client we serve. With a clear understanding of trucking operations, our team works closely with you to deliver guidance that improves efficiency and maximizes the value of your investment. Their commitment ensures your fleet receives attentive and informed service at every stage.

Your information belongs to you and safeguarding it is one of our highest priorities. We implement modern security standards and proven protection practices to help keep your data secure at all times. Our approach is built on transparency and trust and we maintain strict policies to ensure your information is never shared without authorization.

Every fleet operates differently, which is why adaptable insurance solutions are essential. Our coverage options are designed to adjust to your operational size, vehicle types and risk exposure. Whether you manage a growing fleet or an established operation, flexible policies allow you to scale protection as your business expands without unnecessary complications.

When challenges arise, a responsive claims process can make all the difference. Our streamlined approach focuses on quick evaluations and clear communication so you can return to business with minimal downtime. By reducing delays and providing consistent updates, we help keep your fleet moving forward with confidence.