You’re about to renew your Tennessee contractor license and the board is asking for proof of insurance. Or you just lost a commercial bid because your COI didn’t say the right things. Either way, you need more than a generic answer about what GL covers.

The honest truth is this: two HVAC contractors in Nashville can need completely different policies. Your license class, the size of your contracts and whether you work residential or commercial all determine your legal minimum, your real exposure and what your general liability insurance for HVAC contractors in Tennessee actually needs to include.

This article maps all of it the state law, the residential vs. commercial risk split, the coverage gap that catches most HVAC businesses off guard and what your certificate of insurance (COI) needs to say before a general contractor lets you on a commercial job site in Memphis or Nashville.

General liability insurance for HVAC contractors in Tennessee is a policy that covers third-party bodily injury, property damage and advertising injury claims arising from your work. In Tennessee, it is also a legal requirement tied directly to your contractor license classification and the monetary limit the state assigns to your business.

That definition matters more for HVAC than for most trades. You work inside clients’ homes and commercial buildings every day. You handle refrigerants, high-voltage electrical systems and rooftop equipment in extreme weather. Every job site is someone else’s property. Every system you install or service can generate a claim long after you’ve packed up and left.

Here’s what most people get wrong about HVAC job site liability: they assume a basic GL policy covers everything. It doesn’t. And in Tennessee, the law ties your minimum coverage directly to your license which means the right policy for you depends on details most insurance guides never mention.

Tennessee issues HVAC contractors three relevant license types. Each carries a different legal floor for general liability insurance for HVAC contractors in Tennessee. Getting this wrong doesn’t just leave you underinsured it can cost you your license.

The LLE license covers electrical work on projects valued under $25,000. Some counties in Tennessee require an LLE specifically for the wiring aspects of HVAC installations. At the state level, GL is not mandated for LLE holders. But local jurisdictions, commercial landlords and client contracts routinely require proof of GL before you can pull a permit or start work. Just because the state doesn’t force it doesn’t mean you can skip it.

This is the primary state license for HVAC work on projects at or above $25,000. The Tennessee Board for Licensing Contractors requires proof of GL at both application and renewal for all CMC-C holders. The minimum coverage amount is tied to your monetary limit starting at $100,000 and scaling up to $1,000,000. This is the license most Tennessee HVAC contractors operate under and the one where the insurance requirement bites hardest.

The CMC is the broadest mechanical license in Tennessee. It covers HVAC, refrigeration, gas piping, plumbing, sprinklers and more. It requires Board pre-approval before you can even sit the exam. The GL requirement follows the same monetary limit structure as the CMC-C but CMC holders typically carry higher limits because the scope and value of their work demands it.

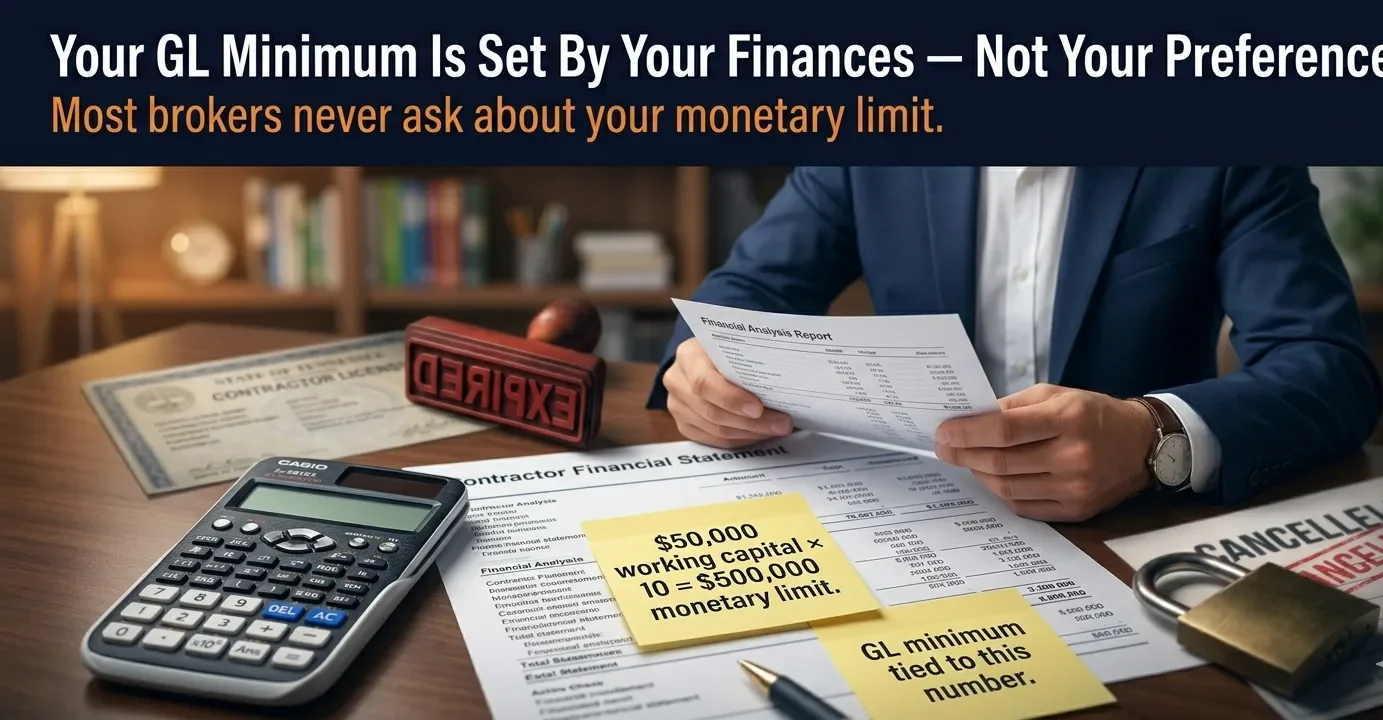

Your monetary limit the maximum contract value you’re licensed to bid is calculated at 10 times the lesser of your working capital or net worth, based on a CPA-prepared financial statement. If your working capital is $50,000 and your net worth is $70,000, your monetary limit is $500,000. And your required GL minimum is tied to that number.

That connection between your finances, your license limit and your insurance minimum is something your broker needs to know. Most don’t ask. Most Tennessee HVAC contractors don’t tell them. The result is a policy that’s priced for a $100,000 monetary limit when your license actually requires more.

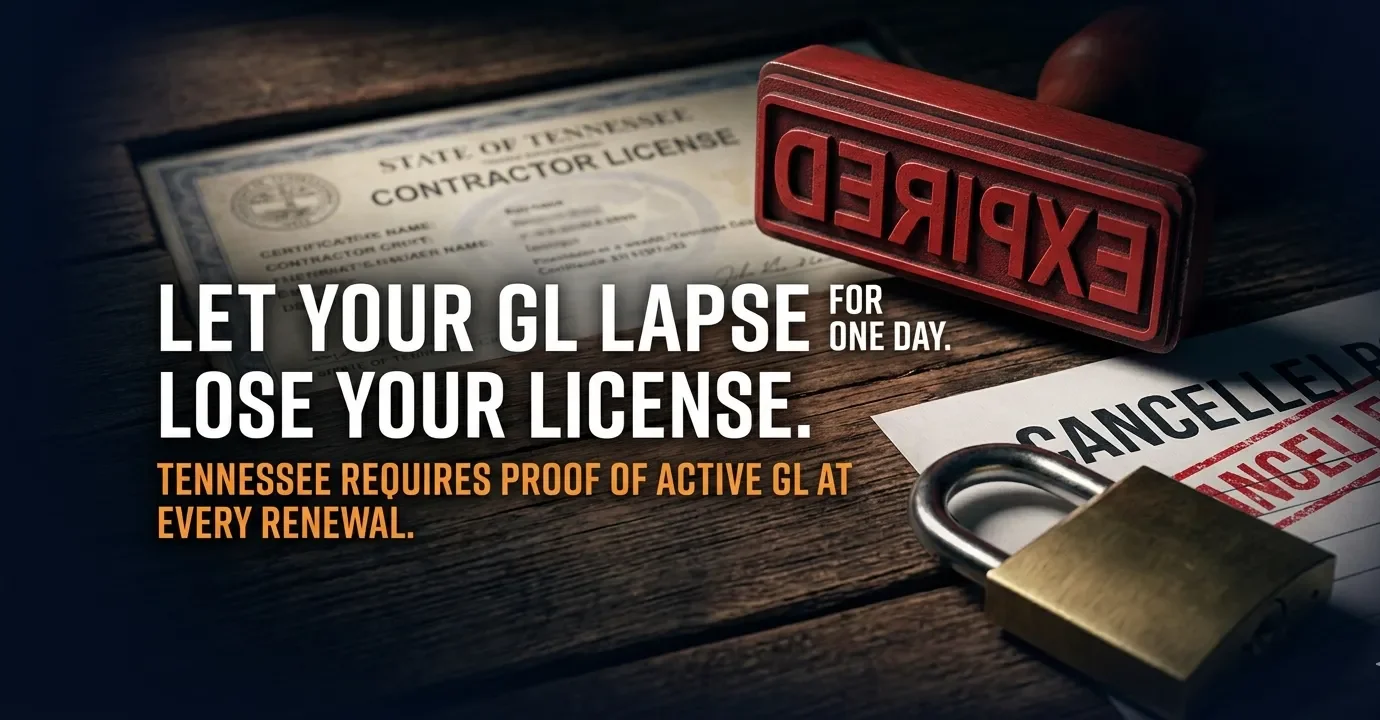

Tennessee contractor licenses expire every two years. Renewal requires a completed application, a $200 fee and critically proof of active GL insurance. If your GL policy lapses even for a single day, you cannot renew. You cannot legally work on licensed projects. Contractor license renewal in Tennessee is directly tied to your insurance status and that dependency catches contractors off guard every renewal cycle.

Most insurance guides treat all HVAC contractors the same. They shouldn’t. A solo tech doing residential tune-ups in Knoxville and a crew running commercial HVAC retrofits in Nashville face completely different exposures and they need completely different policies to match.

Working in homeowners’ houses means your risk is personal and immediate. A customer trips over your equipment. A refrigerant line sweats and damages drywall. A system you installed fails in January and leaves a family without heat. Claims in residential HVAC work typically run $5,000–$50,000. A standard $1 million per-occurrence GL policy is usually sufficient. The homeowner is your claimant. Litigation is less frequent but one bad claim can still wipe out a quarter’s profit.

Commercial work in Nashville office buildings, Memphis restaurants, or Chattanooga hospitals creates a completely different risk profile. A single water damage event from a failed rooftop unit can exceed $100,000 easily. Business interruption losses compound that. Commercial property managers and general contractors require specific COI language additional insured endorsements, primary and non-contributory wording, waivers of subrogation. Many Tennessee HVAC subs lose commercial bids not because they lack insurance but because their COI doesn’t say the right things.

Tennessee summers are punishing. July and August compress HVAC service schedules to their absolute limit. Emergency calls pile up. Technicians work faster, in 95-degree heat, often after hours, under pressure from homeowners who haven’t had air conditioning for two days. Industry data shows emergency HVAC service calls generate claims 3–4 times more frequently than scheduled service work.

What we’ve seen is that the claims that blindside small HVAC businesses in Tennessee don’t come in slow season. They come in August when technicians are exhausted, rushing and skipping steps they’d normally take. That pattern matters when you’re choosing your coverage limits and making sure your completed operations coverage is solid.

General liability is the legally required foundation. But for most HVAC contractors in Tennessee, it’s not enough on its own. Here’s how the full policy stack looks and which pieces the state actually requires versus which ones protect your real-world exposure:

| Coverage Type | What It Covers | Required in Tennessee? |

| General Liability | Third-party injury, property damage, advertising injury | Yes all licensed contractors |

| Workers’ Compensation | On-the-job injuries for your employees | Yes from your first employee |

| Commercial Auto | Business vehicles traveling to job sites | Yes business-owned vehicles |

| Contractors Pollution Liability | Refrigerant leaks and environmental claims | Recommended HVAC-specific |

| Tools & Equipment (Inland Marine) | Theft or damage to tools and gear | Recommended |

| Commercial Umbrella | Extra limits above your GL policy | Recommended for commercial jobs |

| Professional Liability (E&O) | System design errors and faulty specs | Recommended |

If you’re running residential-only HVAC work with one or two employees, a business owners policy which bundles GL and commercial property is often the most cost-efficient starting point. If you’re pursuing commercial contracts, you’ll need to add pollution liability and the right COI endorsements before you submit a single bid.

Standard GL policies contain a pollution exclusion. Most HVAC contractors in Tennessee have never been told what that means for their specific trade so here it is plainly.

Refrigerants R-410A, R-22, R-32 and R-454B are classified as pollutants under most standard GL policy language. If a refrigerant leak at a commercial job site triggers an environmental complaint, damages a client’s property, or contaminates a building’s air system, your standard GL policy will likely deny that claim. The exclusion is written into the base policy. It doesn’t appear in the summary your broker hands you.

Your EPA Section 608 certification covers your legal right to handle refrigerants. It does not cover your liability when something goes wrong with them. The coverage you need is contractors professional liability a separate policy that most Tennessee HVAC contractors have never been offered because most brokers don’t specialize in the trade.

Here’s the honest truth: a denied claim on a refrigerant incident doesn’t just cost you the repair bill. It costs you the legal fees, the environmental response costs and often the client relationship all while your GL insurer walks away citing an exclusion you didn’t know existed. Contractors pollution liability for HVAC work typically adds $150–$500 per year to your premium. That number looks very different after a $22,000 refrigerant claim denial.

Commercial HVAC jobs in Tennessee hospitals, schools, government buildings increasingly require pollution liability as a condition of the contract itself. Before you bid those projects, confirm what your COI actually needs to list.

| Derek owns a four-person HVAC company in Nashville, Tennessee. He mostly handles residential work but has started taking on small commercial retrofits. In August, his crew is replacing a rooftop unit at a restaurant in East Nashville. The job runs long in 98-degree heat. Under time pressure, a technician makes a rushed connection on the refrigerant lines. A slow R-410A leak goes undetected overnight. By morning, the restaurant’s walk-in cooler is compromised $22,000 in spoiled inventory. The building owner reports a refrigerant release to the city. Derek files a GL claim. The insurer reviews the policy. The pollution exclusion applies. The claim is denied. Derek’s company pays the full $22,000 out of pocket, plus $4,000 in legal fees to respond to the municipal notice. Contractors pollution liability would have covered the entire loss. His GL premium was $95 a month. The pollution add-on would have cost him roughly $180 a year. |

Most Tennessee HVAC contractors have a certificate of insurance. Many of them lose commercial bids anyway not because they lack coverage but because their COI says the wrong things.

Here’s what Nashville and Memphis general contractors and commercial property managers typically require before an HVAC subcontractor steps on site. First, additional insured status for the property owner and GC listed by name on the COI, not just by a vague contractual clause. Second, primary and non-contributory language meaning your GL policy pays before theirs and doesn’t seek contribution from the GC’s insurer if both policies apply to a claim.

Third, a waiver of subrogation your insurer agrees not to pursue the general contractor after paying a claim your work caused. Fourth, a 30-day notice of cancellation clause your insurer must notify the certificate holder directly if your policy lapses or cancels. A standard COI from a basic GL policy often has none of this language built in.

Getting these endorsements added is not complicated but only if you ask before you buy the policy. In our experience, the HVAC contractors who lose bids on insurance paperwork are the ones who got the cheapest GL policy without checking what endorsements it included. A policy without the right language isn’t a small problem. It’s a lost contract.

General liability for Tennessee HVAC contractors starts at approximately $39 per month for solo operators focused exclusively on residential work with a clean claims history. According to Simply Business data from actual HVAC contractor policies purchased in the second half of 2024, the national median cost for HVAC contractors across all policy packages runs around $68 per month.

Commercial HVAC work costs more to insure. Higher coverage limits, additional insured endorsements, pollution liability add-ons and the complexity of multi-crew commercial jobs all push premiums up. A full commercial HVAC insurance operation in Tennessee with several employees can realistically expect GL in the $100–$150 per month range before adding workers’ compensation and commercial auto.

Workers’ compensation for HVAC technicians in Tennessee runs approximately $102 per month per worker based on a rate of $2.43 per $100 of payroll. Tennessee requires workers’ comp from the moment you have one employee not five, not three. One. The moment you hire your first technician, you are legally required to carry it.

The single biggest lever you have on your HVAC insurance cost in Tennessee is your claims history. A clean record keeps your experience modification rate (EMR) below 1.0 and earns you lower premiums. One paid claim even a small one can push your EMR above 1.0 and raise your renewal premium across every policy you carry. Protecting your claims record is not just good practice. It’s a direct cost control strategy.

Getting properly covered doesn’t need to take long. Here’s the process that actually works for Tennessee HVAC contractors not the generic five-step list every other site publishes:

Is general liability insurance required for HVAC contractors in Tennessee?

General liability insurance is required for HVAC contractors in Tennessee who hold a state contractor license. The Tennessee Board for Licensing Contractors mandates proof of active GL at both application and renewal. Your minimum coverage amount depends on your license’s monetary limit ranging from $100,000 to $1,000,000. Working without it puts your license and your ability to bid jobs at serious legal risk.

Does my Tennessee HVAC license class affect how much GL coverage I need?

Your Tennessee HVAC license class directly determines your minimum required GL coverage. CMC and CMC-C holders must carry GL tied to their state-assigned monetary limit calculated at 10 times the lesser of your working capital or net worth from your CPA-prepared financial statement. LLE holders face no identical state mandate but routinely encounter GL requirements from local jurisdictions and client contracts.

Does standard general liability cover refrigerant leaks for HVAC contractors?

Standard general liability insurance typically does not cover refrigerant leaks for HVAC contractors. Most GL policies include a pollution exclusion that classifies refrigerants as pollutants. If a refrigerant release damages a client’s property or triggers an environmental complaint, that claim will likely be denied under standard GL. Contractors pollution liability is the correct coverage for this specific HVAC exposure.

What does a Tennessee HVAC contractor’s COI need to say for commercial jobs?

A Tennessee HVAC contractor’s COI for commercial work typically needs to list the property owner and general contractor as additional insureds by name, include primary and non-contributory language, carry a waiver of subrogation and provide 30-day notice of cancellation to the certificate holder. Many HVAC subcontractors lose commercial bids because their COI is missing these endorsements not because they lack insurance entirely.

How much does general liability insurance cost for an HVAC contractor in Tennessee?

General liability insurance for HVAC contractors in Tennessee generally starts around $39 per month for solo residential operators and runs $80–$150 per month for commercial-focused businesses with employees. Your premium depends on your annual revenue, number of employees, ratio of residential to commercial work and your claims history. A clean EMR is the most powerful tool you have for keeping premiums manageable at renewal.

| Coverage requirements vary by license classification, monetary limit, municipality and insurer. Always verify current insurance requirements with the Tennessee Board for Licensing Contractors and review your policy documents with a licensed insurance agent before making coverage decisions. This article is for informational purposes only and does not constitute legal or financial advice. |

General liability insurance for HVAC contractors in Tennessee is not a box to check. The right policy depends on your license class, the monetary limit the state assigned you, whether you work residential or commercial jobs and whether your COI language actually matches what your clients require. Get any of those details wrong and you either lose the bid or pay the claim yourself.

The refrigerant exclusion is real. The license lapse risk is real. The COI language requirement is real. None of them show up on a basic GL quote page. They show up in a denied claim or a lost contract usually when the pressure is already at its highest.

Ready to protect what you’ve built? Get a free quote at OLPolicy or call us directly at (866) 757-5350. It takes under 2 minutes and it could save you thousands.