Did a client just demand proof of insurance before signing your contract and you have nothing to show them? General liability insurance for cleaning business in Texas is not optional anymore it is the price of entry into every serious commercial account. One accident, one broken item, one angry client can wipe out months of hard-earned profit. Cleaning business insurance protects your income, your reputation and your future. Whether you run a residential cleaning service or a full commercial janitorial operation, the right liability coverage for cleaners keeps your Texas business protected, professional and ready to grow without fear.

Cleaning business insurance is a collection of policies designed to protect cleaning professionals from financial losses caused by accidents, lawsuits and unexpected events. Think of it like a safety net stretched under a tightrope walker. You hope you never fall but you would be foolish to work without one. Insurance for cleaning companies covers everything from a client tripping over your equipment to an employee accidentally bleaching an expensive carpet. Texas cleaning businesses face risks every single day chemical spills, broken client property, stolen valuables and slip-and-fall injuries happen far more often than most people expect.

According to the U.S. Bureau of Labor Statistics, the cleaning industry employs over 3.2 million workers across America and every single one of those workers faces real on-the-job risks. Janitorial business insurance gives both employers and employees a financial cushion when things go sideways. Without it, even a minor incident can spiral into a lawsuit that drains your bank account dry. The moment you start accepting clients in Texas, you need proper cleaning services insurance coverage in place. No exceptions.

Here is a scenario that happens more than you think. Your crew is cleaning a high-end Dallas office. One employee moves quickly and knocks a $3,000 laptop off a desk. The client is furious and wants full replacement value today. Without liability insurance for cleaning business, that cost lands squarely on your shoulders. With it, your insurer handles the claim and you keep your client relationship intact. Commercial cleaning insurance exists precisely for moments like this one. A single lawsuit without coverage can cost $15,000 to $45,000 in legal defense fees alone before any settlement is paid.

Beyond accidents, Texas commercial clients property managers, corporate offices, hospitals and government buildings require proof of cleaning company liability insurance before they sign a single contract. It is not a suggestion. It is a hard requirement. Many clients demand a Certificate of Insurance (COI) before you ever set foot on their property. Meeting these contract requirements is not just about protection it is about winning and keeping your biggest accounts. House cleaning business insurance also builds serious trust with residential clients who invite you into their private homes every week.

No single policy covers every risk your cleaning business faces. You need a smart combination of coverage types tailored to your specific operation. A solo housekeeper in Austin needs different coverage than a 20-person commercial janitorial crew in Houston. Understanding your options helps you build a protection plan that fits your budget and your risk level. Business insurance for janitorial services typically involves two to four separate policies working together to provide complete protection.

The table below gives you a quick overview of the most common coverage types for Texas cleaning businesses. Study it carefully knowing what each policy does helps you avoid buying coverage you do not need and missing coverage you absolutely do.

| Policy Type | What It Covers | Who Needs It |

| General Liability Insurance | Third-party injuries and property damage | Every cleaning business |

| Workers’ Compensation | Employee injuries and lost wages | Businesses with employees |

| Commercial Auto Insurance | Work-related vehicle accidents | Businesses driving to job sites |

| Business Owner’s Policy (BOP) | GL + commercial property combined | Businesses with equipment or offices |

| Janitorial Bond | Employee theft from client property | All client-facing cleaning businesses |

| Professional Liability | Negligence or poor workmanship claims | Specialty cleaning companies |

| Umbrella Liability Insurance | Extra coverage above standard limits | High-revenue cleaning businesses |

| Tools and Equipment Insurance | Damage or theft of cleaning equipment | Businesses with expensive gear |

General liability insurance is the foundation of every solid cleaning services insurance coverage plan. It protects you when a third party a client, a visitor, anyone who is not your employee suffers an injury or property damage because of your work. If a client claims your team scratched their hardwood floors, spilled chemicals on their furniture, or caused a slip-and-fall accident, commercial general liability insurance kicks in to cover repair costs, medical bills and legal defense fees. For Texas cleaning businesses, standard limits are $1 million per occurrence and $2 million aggregate. Most small cleaning companies pay between $30 and $60 per month making it the most affordable and most essential piece of cleaning contractor insurance you can carry.

Workers’ compensation insurance covers your employees when they get hurt on the job. Cleaning work involves heavy lifting, chemical exposure, wet floors and repetitive motion all of which cause real injuries. If an employee throws out their back moving furniture in a San Antonio home, workers’ comp pays their medical bills and replaces a portion of their lost wages while they recover. Texas is uniquely the only state in the U.S. where workers’ compensation is technically optional for most private employers. However, skipping it is a massive gamble. Without it, an injured employee can file a civil lawsuit directly against your business with no cap on damages.

Commercial auto insurance fills the gap that your personal auto policy leaves wide open. Your personal auto insurance will not cover accidents that happen while driving to or from a job site a fact most new cleaning business owners discover the hard way. Texas requires minimum auto liability limits of $30,000 per person, $60,000 per accident and $25,000 for property damage. For a cleaning business hauling equipment and driving employees around Houston traffic, higher limits make more sense. Many cleaning services business owners also add inland marine coverage to protect the cleaning supplies and tools stored in their vehicles from theft or damage.

A business owner’s policy (BOP) bundles general liability insurance and commercial property insurance into one convenient, cost-effective package. For small cleaning businesses with an office, storage unit, or equipment depot, a BOP offers broader protection at a lower combined price than buying both policies separately. It typically covers your physical assets equipment, furniture, supplies and your workspace against fire, theft, vandalism and weather damage. Texas cleaning businesses pay an average of $50 to $100 per month for a BOP. If your business owns significant assets beyond just cleaning supplies, this bundle deserves serious consideration as part of your professional cleaning insurance strategy.

A janitorial bond is a surety bond not technically insurance but it is equally critical for any client-facing cleaning operation. It protects your clients financially if one of your employees steals money, jewelry, electronics, or other valuables from their property. Most Texas commercial clients and property managers require a janitorial bond before they will hire a cleaning company. A $10,000 janitorial bond typically costs between $100 and $300 per year a tiny investment that pays massive dividends in client confidence. Janitorial business insurance and bonding together form the complete trust package that separates serious professional cleaning companies from operations clients cannot rely on.

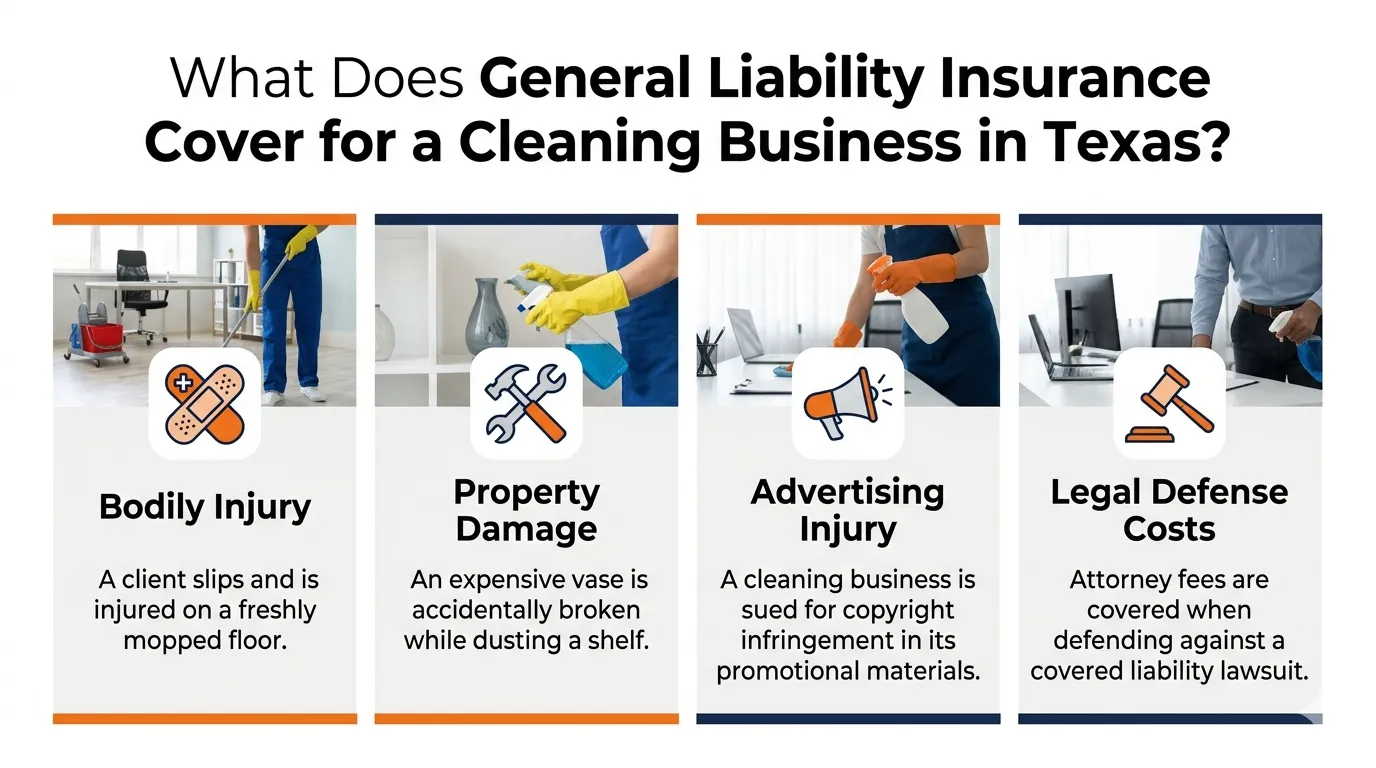

Cleaning services insurance coverage protects your business across four major categories: bodily injury claims, property damage, advertising injury and legal defense costs. Understanding each one helps you appreciate exactly what you are buying and why every category matters in real-world situations. Bodily injury claims kick in when a client or visitor gets hurt because of your work. Property damage claims coverage handles repair or replacement costs when your team accidentally damages a client’s belongings. Advertising injury protection often overlooked protects you if a competitor accuses you of copying their marketing materials or making false claims about their business.

Legal defense costs cover attorney fees and court expenses even if the lawsuit against you turns out to be completely frivolous. One critical point: cleaning company liability insurance does NOT cover injuries to your own employees. That is what workers’ compensation insurance handles. These two policies work as a team neither one alone gives you complete business liability protection. The table below breaks down every major coverage category with real-world examples to show you exactly when each one applies.

| Coverage Category | What It Pays | Real-World Example |

| Bodily Injury | Medical bills, lost wages, legal fees | Client slips on your wet floor |

| Property Damage | Repair and replacement costs | You crack a client’s marble countertop |

| Advertising Injury | Libel, slander, copyright claims | Competitor sues over your marketing |

| Legal Defense Costs | Attorney fees, court costs | Client files a negligence lawsuit |

| Medical Payments | Immediate medical bills, no lawsuit needed | Visitor injured at your office |

| Employee Dishonesty | Theft by employees (via janitorial bond) | Employee steals jewelry from a client |

The honest answer is: it depends but it is almost always more affordable than most cleaning business owners expect. Small cleaning business insurance can cost as little as $25 per month for a solo cleaner with basic general liability coverage. Larger operations with multiple employees, company vehicles and commercial clients will pay more but the protection they receive in return is worth every dollar. Paying annually instead of monthly almost always saves you money. Most commercial insurance providers offer a 5 to 15 percent discount for annual payment. Bundling multiple policies with one insurer cuts your total insurance premium cost by another 10 to 20 percent.

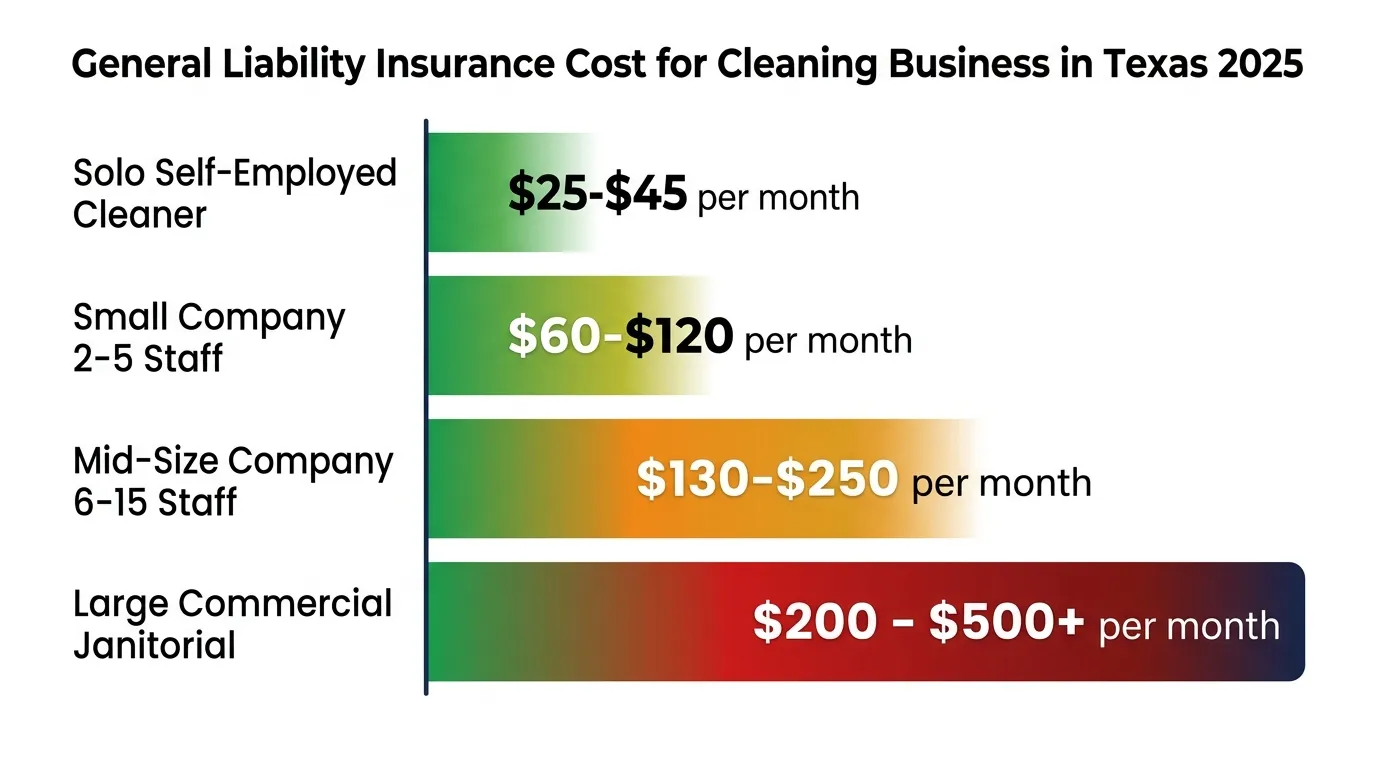

Here is a practical cost breakdown for Texas cleaning businesses. Use this as your baseline when you start comparing affordable cleaning business insurance quotes from different providers. Keep in mind that these are averages your actual premium depends on your specific risk profile, claims history and coverage limits chosen.

| Business Type | Monthly Cost | Annual Cost |

| Solo / Self-Employed Cleaner | $25 – $45 | $300 – $540 |

| Small Cleaning Company (2–5 staff) | $60 – $120 | $720 – $1,440 |

| Mid-Size Cleaning Company (6–15 staff) | $130 – $250 | $1,560 – $3,000 |

| Large Commercial Janitorial Business | $200 – $500+ | $2,400 – $6,000+ |

| Business Owner’s Policy (BOP) | $50 – $100 | $600 – $1,200 |

| Workers’ Comp (per $100 payroll) | $1.00 – $2.50 | Varies by payroll |

Insurance underwriting factors are the variables that insurance companies use to calculate your insurance premium cost. The more risk your business represents, the higher your premium. Understanding these factors helps you manage costs proactively and avoid surprises when your renewal arrives. Texas-specific risks like mold liability exposure in humid Gulf Coast cities such as Houston and Corpus Christi can affect your cleaning contractor insurance rates in ways that competitors rarely mention. Specialty cleaning services like biohazard remediation, post-construction cleanup and pressure washing carry significantly higher risk than standard residential or office cleaning.

Your claims history is one of the most powerful factors affecting your rate. Even one past claim can increase your renewal premium by 20 to 40 percent. A clean claims history is genuinely worth protecting practice thorough risk management on every job. The number of employees you carry also matters significantly. More people on job sites means more chances for accidents and higher workers’ compensation premiums. New businesses typically pay higher rates too. After three to five years with a clean record, most cleaning services business owners qualify for valuable experience discounts that reduce their annual costs.

| Cost Factor | How It Affects Your Premium |

| Business Size & Revenue | Higher revenue = more exposure = higher premium |

| Number of Employees | More staff = more risk on job sites |

| Services Offered | Specialty services like pressure washing raise rates |

| Location in Texas | Urban markets and Gulf Coast humidity increase rates |

| Claims History | One prior claim raises renewal premium 20–40% |

| Coverage Limits Chosen | Higher limits = higher monthly premium |

| Years in Business | Newer businesses pay more; experience discounts apply |

Texas does not legally require general liability insurance for cleaning business operations. That is the straightforward legal answer. However, the practical reality tells a completely different story. The Texas Department of Licensing and Regulation (TDLR) does not mandate GL coverage for most cleaning operations but the market absolutely does. Almost every commercial client in Texas requires proof of cleaning company liability insurance before awarding a contract. Many require minimum coverage limits of $1 million per occurrence. Government cleaning contracts consistently demand even higher limits and additional endorsements. Texas also remains the only U.S. state where workers’ compensation is technically optional for private employers.

Skipping workers’ compensation means your injured employees can sue your business directly without any cap on damages a risk no smart business owner takes. HOA communities and property management companies across Dallas, Houston and Austin typically require $1 million minimum cleaning service liability coverage before granting access to managed properties. The bottom line: no law requires it, but try winning a meaningful commercial contract in Texas without it. You simply cannot. Here is a clear summary of what is legally required versus what is practically necessary for insurance for cleaning professionals operating in Texas.

| Requirement Type | Legally Required? | Practically Required? |

| General Liability Insurance | No | Yes by most commercial clients |

| Workers’ Compensation | No (optional) | Strongly recommended for all employers |

| Commercial Auto Insurance | Yes | Yes required by Texas law |

| Janitorial Bond | No | Yes required by most commercial clients |

| Certificate of Insurance (COI) | No | Yes required before most contracts begin |

Choosing the right cleaners insurance policy starts with honest self-assessment. Ask yourself: What types of properties do you clean? How many employees do you have? Do you use company vehicles? Do you handle expensive equipment or specialty surfaces? Your answers directly determine which policies you need and at what coverage limits. Liability coverage that works perfectly for a two-person residential cleaning duo will not adequately protect a 15-person commercial janitorial operation. Always match your coverage limits to the value of the properties you service if you clean $500,000 buildings, carry at minimum $2 million aggregate coverage.

When comparing providers, do not just chase the cheapest quote. Compare what is actually included coverage limits, exclusions, deductible amounts and claims support quality. Look for insurers with an AM Best rating of A or better, which signals financial stability. Providers specializing in cleaning service liability coverage like Next Insurance, Thimble and Hiscox understand the specific risks of your industry far better than general business insurers. Always read exclusions carefully. Some standard policies exclude mold damage, chemical damage and subcontractor work all of which are common risks in the Texas cleaning industry. Knowing what your policy does NOT cover is just as important as knowing what it does.

| Selection Criteria | What to Look For |

| Coverage Limits | Minimum $1M per occurrence / $2M aggregate |

| Exclusions | Check for mold, chemical, subcontractor gaps |

| Claims Support | 24/7 claims reporting preferred |

| Provider Rating | AM Best A or better |

| Price Comparison | Compare same limits across 3+ providers |

| Bundling Options | Ask about BOP discounts for combined policies |

| Subcontractor Coverage | Verify explicitly if you use subcontractors |

Getting cleaning business insurance is simpler and faster than most people expect. Many insurance quote online platforms offer instant coverage sometimes within minutes of submitting your application. Following a clear process ensures you get the right coverage at the best available price without leaving dangerous gaps in your protection. Here is the exact step-by-step process that Texas cleaning business owners use to get properly covered quickly and confidently.

Step 1 Gather Your Business Information

Before requesting any quotes, collect your business name, address, EIN, estimated annual revenue, number of employees, types of cleaning services offered and any prior insurance claims history. Accurate information leads to accurate quotes and avoids coverage disputes later.

Step 2 Request Insurance Quotes Online

Use platforms like Next Insurance (nextinsurance.com), Thimble (thimble.com) and Hiscox (hiscox.com) for fast online quotes. You can also contact a local Texas independent insurance agent who can shop multiple carriers on your behalf. Always get a minimum of three quotes for meaningful price and coverage comparison. Never accept the first quote you receive without comparing others.

Step 3 Compare Coverage Options Carefully

Do not let price be your only comparison point. Look at insurance policy coverage limits, deductibles, exclusions and what each policy actually covers. Ask directly: Does this policy cover subcontractors? Does it include mold or chemical damage? What is the claims process like? The cheapest policy with the most exclusions often costs far more when a real claim occurs.

Step 4 Purchase the Policy and Get Your COI

Most policies activate the same day or the next business day. The moment your policy is active, request your certificate of insurance (COI) immediately. Store it digitally. Email it to clients whenever they request it. Commercial clients will ask for it constantly having it ready to send in seconds looks professional and keeps deals moving. Many Texas cleaning businesses keep a template email ready with their COI attached for instant delivery.

Step 5 Review Your Coverage Annually

Your business grows. Your coverage needs to grow with it. Adding employees, expanding services, or landing bigger commercial contracts all change your risk profile. Review your professional cleaning insurance every 12 months and update it whenever your business changes significantly. An outdated policy is almost as dangerous as no policy at all.

These are the questions Texas cleaning business owners ask most often when researching general liability insurance for cleaning business in Texas. The answers below cut through the confusion and give you clear, actionable information you can use today.

Do self-employed cleaners need insurance in Texas?

Absolutely and here is why it matters even more for solo operators. When you work alone, you have no business structure absorbing liability. Every claim goes directly against you personally. Liability insurance for house cleaning business solo operators is available for as little as $25 to $40 per month. Most residential clients feel significantly more comfortable hiring an insured cleaner. Commercial clients will not even consider you without it. A single property damage claim without coverage can cost more than ten years of insurance premiums combined.

What coverage limits should I choose?

For most Texas cleaning businesses, the standard recommendation is $1 million per occurrence and $2 million aggregate for general liability insurance. If you clean high-value commercial properties, luxury homes, hospitals, or government buildings, consider $2 million per occurrence and $4 million aggregate. Higher limits add modest monthly cost often just $10 to $20 more but dramatically increase your credibility with premium clients and your protection against serious claims.

Can cleaning insurance cover subcontractors?

Standard cleaning company liability insurance policies frequently exclude subcontractors and this catches many cleaning business owners off guard. If you use subcontractors regularly, ask your insurer explicitly about subcontractor coverage before purchasing. Some insurers offer endorsements that extend coverage to subcontractors for an additional premium. Alternatively, require every subcontractor you hire to carry their own general liability insurance and provide you with a certificate of insurance naming your business as an additional insured.

What is the difference between a janitorial bond and liability insurance?

These two products serve completely different purposes and you genuinely need both. General liability insurance covers accidental damage and injury claims the kind of incidents that happen by mistake. A janitorial bond covers intentional employee theft from a client’s property. One protects against accidents. The other protects against dishonesty. Together, they give your clients complete peace of mind and your business complete protection across every possible risk scenario.

How do I get a certificate of insurance for my cleaning business?

Once you purchase a cleaning business insurance policy, your insurer issues a certificate of insurance (COI) a standardized one-page document summarizing your coverage details. Request it immediately upon policy activation. Most insurers provide it digitally within minutes. Store it in your email, your phone and a cloud folder so you can send it to any client within seconds. Commercial clients in Texas will request your COI constantly having it instantly ready is one of the simplest ways to look more professional than your competition.

Can I get same-day coverage for my cleaning business?

Yes many online providers like Next Insurance and Thimble offer instant coverage that activates the same day you apply. Traditional insurance agents may take one to three business days to process your policy. Same-day coverage is especially useful when you land a new commercial contract unexpectedly and the client demands a COI before work begins. Keep your business information organized and ready so you can complete any insurance application in under 15 minutes whenever a new opportunity arises.

Running a cleaning business in Texas is a genuine opportunity. The demand for professional cleaning services residential, commercial and specialty keeps growing every year. But growth brings risk. General liability insurance for cleaning business in Texas is not a luxury or an afterthought. It is the foundation of a business that lasts. It protects your income when accidents happen, wins you better clients and proves to the market that you are a serious professional worth trusting.

Start with general liability insurance. Add workers’ comp if you have employees. Consider a business owner’s policy if you have equipment or an office. Get bonded. Review your coverage every year. The cleaning industry rewards professionals who operate with integrity and preparation and the right cleaning services insurance coverage is one of the clearest signals of both. Do not wait until an accident forces your hand. Get covered today and build your Texas cleaning business on a foundation that no lawsuit, no accident and no claim can shake.

Still looking for the right general liability insurance for your cleaning business in Texas? Call (866) 757-5350 or visit OLPolicy today for a free personalized quote and get your business covered in minutes.