You signed a client contract and now they’re asking for proof of insurance. Or a customer slipped on your property and you have no idea if you’re covered. Either way, you need a straight answer about what does general liability insurance cover for small business and what it doesn’t.

This article gives you the full picture. We’ll break down every coverage your policy includes, every gap you need to know about and the real numbers behind what a claim can cost you. By the end, you’ll know exactly what you have, what you’re missing and what to do next. Commercial general liability (CGL) coverage isn’t complicated once someone explains it plainly. Let’s do that now.

General liability insurance for small business is a policy that protects you from the financial impact of third-party claims meaning claims made by people outside your company. It typically covers bodily injury, property damage, personal and advertising injury and related legal defense costs, depending on your specific policy and insurer.

That definition is the foundation. Everything else builds from it. Here’s a breakdown of each coverage type you’ll find inside a standard GL policy.

This is the coverage most people picture first. It pays for medical bills, hospital costs and legal fees when a non-employee gets injured because of your business. Think customers, vendors, or passersby not your own staff.

In practice, what we see is third-party injury claims topping the list for small businesses. A single slip-and-fall incident can generate tens of thousands in medical costs before any lawsuit even gets filed.

Property damage liability covers the cost to repair or replace someone else’s property when your operations cause the damage. If your employee backs a work van into a client’s fence, this is the coverage that steps in.

This applies to both real property like a building and personal property, like a client’s furniture or electronics. The coverage follows your business wherever it operates, not just at your primary location.

This one surprises most small business owners. Advertising injury coverage protects you if someone claims your business defamed them, committed libel or slander, or infringed on their copyright through an advertisement. It has nothing to do with physical harm.

For example, if a competitor claims your social media post copied their tagline, your GL policy can step in and cover your legal defense. Intellectual property disputes escalate fast this protection matters more than most people realize.

Medical payments coverage is a smaller, fast-acting benefit built into most GL policies. It pays for immediate medical expenses when someone is injured on your property regardless of who was at fault.

This differs from bodily injury coverage. Medical payments are typically capped at lower limits (ofte

n $5,000 to $10,000), but they help resolve minor incidents quickly. That speed can prevent a small accident from becoming a major lawsuit.

If your product causes harm after it’s sold or your completed work causes damage after you leave the job site this is the coverage that applies. Contractors, manufacturers and food businesses rely on it heavily.

Here’s what most people get wrong about this: they assume their liability ends when the job ends. It doesn’t. A plumber who finishes an installation is still potentially liable if that work fails two months later and floods a client’s home.

Let’s be real GL is broad, but it has firm limits. The most common misconception is that it acts as a catch-all for everything that can go wrong in your business. It doesn’t.

Your own employees are not covered under GL. If a worker gets hurt on the job, that falls under workers’ compensation insurance which most states legally require the moment you bring on your first hire. Confusing the two is one of the costliest mistakes a small business owner can make.

GL also won’t touch your own business property. If your equipment is stolen or your office floods, you need commercial property insurance for that. If a client claims your professional advice cost them money, professional errors and omissions insurance is the right policy not GL.

Two more gaps to know. Your GL policy won’t cover auto accidents involving business vehicles that requires commercial auto coverage. And cyberattacks or data breaches need a separate cyber liability policy entirely. Coverage always has a boundary. Knowing yours before a claim hits is what actually protects you.

Most small business owners start with a $1 million per-occurrence limit and a $2 million aggregate limit. Here’s what that actually means: your insurer pays up to $1 million for any single covered incident and no more than $2 million total across all claims in the policy year.

The per-occurrence limit is the number most landlords and clients check first. Many commercial leases and vendor contracts require at least $1 million before you can sign. Industry data puts the national median GL cost for small businesses at around $60 per month with lower-risk businesses sometimes paying closer to $30.

That said, $1 million isn’t always enough. High-risk trades, public-facing businesses and companies working on large-value contracts often need higher aggregate limits or a commercial umbrella policy to cover what sits above those caps. The right limit isn’t about what sounds safe it’s about what your contracts, your industry and your real risk exposure demand.

Let’s say Marcus owns a small painting company in Columbus, Ohio. He has two employees and mostly works on residential homes. One afternoon, his crew is painting an interior room when a ladder tips and shatters the homeowner’s antique mirror. The homeowner trips on the drop cloth trying to get out of the way and sprains her wrist.

She files a claim covering her medical bills and the cost of the mirror. Without GL, Marcus pays every dollar out of pocket plus legal fees if she decides to sue. With a $1 million GL policy in place, his insurer takes the call. They cover the medical costs, the property damage and the legal defense. Marcus pays his deductible. His business stays intact, his cash flow is untouched and he’s back on the job the following week. That’s exactly what this coverage is designed to do absorb the hit so your business doesn’t have to.

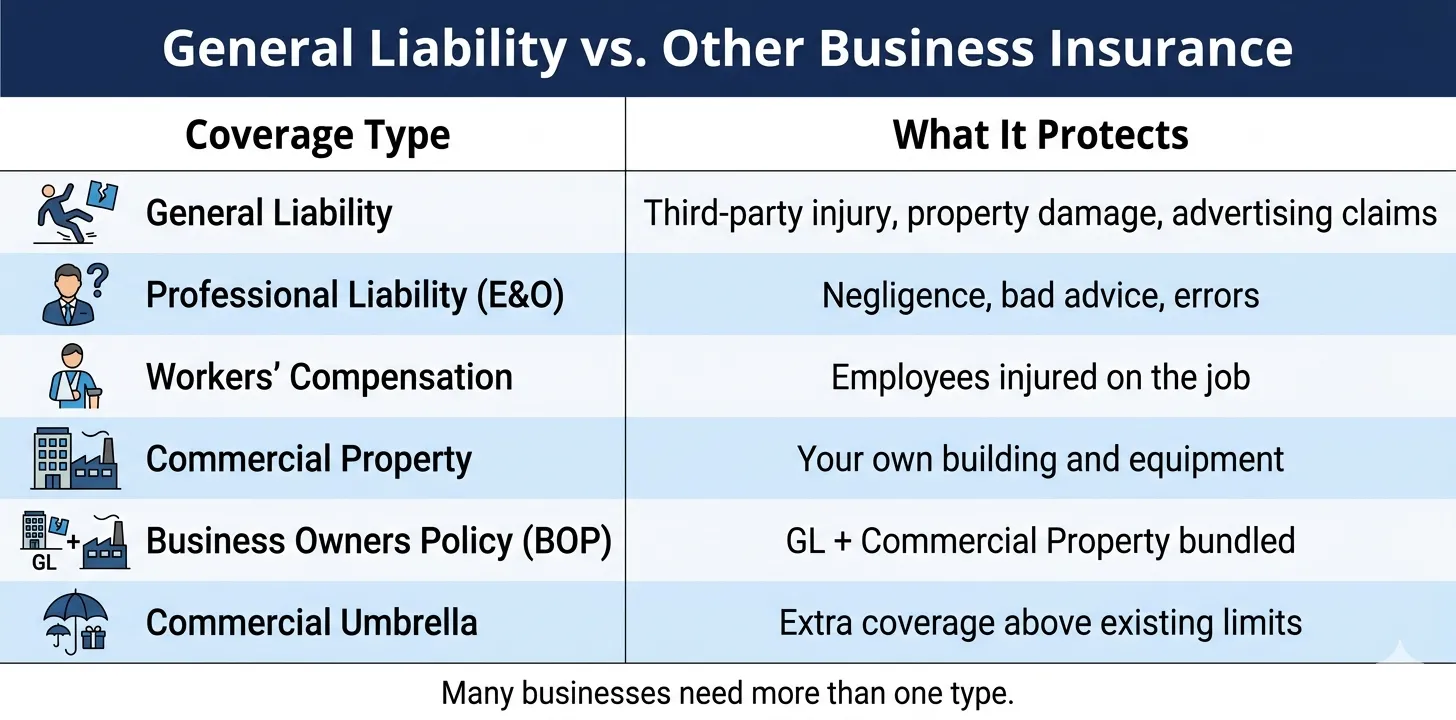

Choosing the right coverage starts with understanding where GL ends and other policies begin. Many small business owners carry GL and assume they’re fully protected. They’re not at least not against every risk.

Here’s how GL stacks up against the other policies your business may need:

| Coverage Type | What It Covers |

| General Liability | Third-party bodily injury, property damage, advertising injury |

| Professional Liability (E&O) | Negligence, professional errors, failure to deliver services |

| Workers’ Compensation | On-the-job injuries or illness for your employees |

| Commercial Property | Your own building, equipment and inventory |

| Business Owners Policy (BOP) | GL + commercial property bundled into one policy |

| Commercial Umbrella | Extra coverage above your existing GL or other policy limits |

If your business owns equipment, rents office space, or has employees, a business owners policy (BOP) typically delivers more complete protection than standalone GL. Think of GL as the foundation the BOP builds the rest of the house on top of it. For service-based businesses that offer expert advice, adding professional liability insurance is usually just as essential as GL itself.

Here’s a statistic that should get every business owner’s attention. The Insurance Information Institute (III.org) notes there are over 8 million small businesses in the United States and the overwhelming majority face third-party liability exposure every single day they operate.

Industry surveys consistently find that 90% of small business owners aren’t confident they’re adequately insured. Only about half of all small businesses actually carry GL coverage. That gap is staggering especially when you consider that a single slip-and-fall lawsuit can generate $50,000 or more in legal fees before any settlement is even discussed.

Recent commercial insurance research also found that 36% of small businesses saw premium increases in 2024, making it more important than ever to compare quotes rather than staying on auto-renewal. What we’ve seen is that business owners tend to underestimate how fast a claim escalates. Based on how claims typically work, the businesses hurt most are the ones that bought a policy once and never revisited their limits as their company grew.

Mistake #1: Assuming GL covers your employees. This is the most expensive misconception we see. GL is built for third-party claims customers, clients and the general public. The moment an employee gets hurt on the job, you need workers’ compensation. In most states, you’re legally required to carry workers’ comp the second you hire your first employee. Going without it isn’t just risky it can mean state fines, personal lawsuits and liability that pierces right through your business structure.

Mistake #2: Buying the cheapest policy without checking the limits. A $30-a-month GL policy sounds like a win. But if that policy carries a $300,000 per-occurrence limit and a lawsuit demands $800,000, you’re covering the difference yourself. Here’s the honest truth the price of a policy matters far less than the limits inside it. Always read past the premium line and check what your insurer will actually pay, per incident and per year, before you commit.

Mistake #3: Thinking your liability ends when the job ends. Products-completed operations coverage exists for a good reason. Your exposure doesn’t stop when you hand over the finished product or leave the job site. If a contractor installs a water heater and it fails three months later, flooding a client’s home, that’s still a GL claim against you. Many small business owners don’t realize they remain exposed long after the invoice is paid and the project is closed.

Almost every business that interacts with customers, clients, or the public needs some level of GL coverage. But certain businesses face sharper exposure and the stakes of going uninsured are significantly higher for them.

Contractors and tradespeople top that list. Many state licensing boards and client contracts require proof of GL before work can legally begin. Retail stores and restaurants follow closely high foot traffic means high slip-and-fall risk and even a single incident can trigger a claim that wipes out months of profit. Home-based businesses often assume their homeowner’s policy has them covered. In most cases, it doesn’t extend to business activities at all.

If you rent commercial space, your landlord almost certainly requires a GL policy before you sign a lease. If you work with corporate clients, they’ll ask for your certificate of insurance (COI) before engaging you sometimes before the first meeting. In our experience, the businesses most likely to get blindsided by a claim are the ones that thought their industry was too low-risk to bother. No business is too small or too “safe” to need this coverage.

Getting covered doesn’t need to take long. Most small business owners can get a policy in place the same day they start looking. Here’s the process:

You can compare commercial general liability options for your business right now at OLPolicy.com. It takes under two minutes and shows you real quotes side by side.

Does general liability insurance cover my employees?

General liability insurance does not cover your employees. Injuries or illness your workers suffer on the job fall under workers’ compensation insurance which most states legally require as soon as you hire your first employee. GL only applies to third parties: customers, clients and members of the public who are not on your payroll.

Is general liability insurance required by law for small businesses?

General liability insurance is not required by federal law for most small businesses. However, your state’s licensing board, your commercial landlord, or your client contracts may require it. Many contractors cannot legally begin work without proving GL coverage. Always check your specific industry requirements and contract terms before assuming you are exempt from carrying it.

How much does general liability insurance cost for a small business?

General liability insurance typically costs between $30 and $85 per month for most small businesses. Your exact rate depends on your industry, annual revenue, location and coverage limits. Industry data shows the national median GL cost sits around $60 per month for most small businesses. Higher-risk trades like general contractors generally pay more than lower-risk service businesses.

Does general liability cover property damage I accidentally cause to a client?

General liability insurance does cover accidental property damage you cause to someone else. If your employee breaks a client’s equipment during a job, your GL policy can pay to repair or replace it. It does not cover damage to your own business property that protection requires commercial property insurance or a business owners policy that bundles both coverages.

What is the difference between general liability and a business owners policy?

A business owners policy (BOP) combines general liability with commercial property insurance in one bundled policy. General liability alone only covers third-party claims. A BOP adds protection for your own building, equipment and inventory and typically costs less than buying both coverages separately. Most small businesses with physical assets or commercial space benefit from a BOP over standalone GL.

Coverage terms vary by state and insurance provider. Always review your policy documents carefully or speak with a licensed insurance agent before making coverage decisions. This article is for informational purposes only and does not constitute legal or financial advice.

General liability insurance is the foundation every small business needs but only if the limits match your actual risk. A low-premium policy with thin caps can leave you fully exposed at the exact moment you need protection most. Know what your policy covers. Know what it doesn’t. Revisit your limits every time your business grows or your contracts change. That one habit is the difference between a manageable claim and a financial crisis.

Ready to protect what you’ve built? Get a free quote at OLPolicy or call us directly at (866) 757-5350. It takes under 2 minutes and it could save you thousands.