Finding the Lowest Home Owners’ Insurance can be tough, but not impossible. You want coverage that protects your home without breaking the bank. If disaster strikes, your insurer should help you recover quickly. With rates rising in many states, choosing the cheapest policy can be tempting. But your home is likely your biggest financial asset. Cutting corners could leave you in trouble. OLPolicy insurance experts show how to get the best coverage for your budget.

When looking for Lowest Home Owners Insurance, it’s easy to focus only on price. Rates have risen steadily in recent years, and new tariffs could push them higher. Budget matters, but the right insurance company is more than just cost. You also need to check reliability, claims service, and coverage options. Here’s what to consider when choosing a home insurance company.

When comparing quotes for Lowest Home Owners Insurance, price comes first. But don’t stop there. Make sure all quotes have the same coverage limits and deductibles for a fair comparison.

Focus on three key numbers:

(Coverage A): How much your insurer will pay to rebuild your home. Other limits are based on this, making it very important. Personal liability limit: Covers injuries or property damage caused by you or family members. Includes legal and medical costs. Deductible: The amount you pay out of pocket for a claim.

Also, check if quotes use actual cash value or replacement cost. Cash value costs less but pays less if a claim occurs. Replacement cost is higher but gives a better payout, especially for Coverage A and personal property.

Discounts will help get the Lowest Home Owners Insurance easier. Many insurers have various methods of saving and they can greatly reduce your premium. To determine what discount is applicable to you; always enquire about discounts when seeking quotes.

Other typical discounts are bundling, meaning you take home and auto insurance with the same company. Costs can also be minimized by security systems such as fire or burglar alarms. Special savings may be available on new building or new renovations. There are loyalty discounts available to long time customers and homeowners who have no recent claim may receive a claims-free discount.

The other premium reduction method is to opt to pay a higher deductible. This implies that you make larger out of pocket payments in case of a claim, but your monthly payment will reduce. It is through the comparison of quotes with various deductibles that you can get the balance between savings and coverage.

With the help of the relevant discounts and intelligent deductible options, you can get the Lowest Home Owners Insurance without sacrificing the coverage. Go through all the alternatives of the various carriers to have the best deal in terms of home and budget.

Price is not the only factor to take into account when seeking the Lowest Home Owners Insurance. Third-party ratings put in place by a trusted third party provides a clear understanding of the quality of a company. J.D. Power customer satisfaction scores indicate how the carriers process claims and compare them with each other. The financial strength ratings issued by AM Best and Standard and Poor show the capability of a company to meet its claims. The National association of Insurance Commissioners complain indexes are used to show the number of complaints a company gets relative to other companies of the same size.

Appraisal of how you will handle your policy is also important. You can think of the ease with which you can communicate with the insurer. The carriers that have the best digital tools can be more convenient, in case you reside in a remote area. Time and stress can be saved on online account management, mobile apps and convenient claims submission.

Selection of the appropriate company implies a trade-off between price and quality and reliability of the services. Using ratings, financial durability, complaints, and online access, you are sure to choose the Lowest Home Owners Insurance that can secure your home and give you convenient assistance whenever you require it.

Buying homeowners insurance involves more than paying a premium. Policy reviews, customer service, and claims all affect satisfaction. Surveys show that premium cost and claims handling have the biggest impact on customer happiness. Premiums have risen sharply in recent years, making price an important factor when choosing the Lowest Home Owners Insurance.

You can check ratings to see how the 28 top insurers perform in claims, service, advice, and pricing. Some state insurance departments also provide rate comparisons. For example, Floridians can visit the Florida Office of Insurance Regulation website, and Californians can check the California Department of Insurance site.

Keep in mind, some top-rated insurers—like NJM, Erie, and USAA (for military members and eligible relatives)—use their own agents. Their policies may not appear on comparison sites, so you must apply directly.

By reviewing ratings, comparing quotes, and checking top insurers, you can find the Lowest Home Owners Insurance that balances cost with strong coverage and reliable service.

Extra options, add-ons, and separate coverages can raise the cost of a standard policy. But they may save you money if disaster strikes. When shopping for the Lowest Home Owners Insurance, check if carriers include these extras or charge extra. Here are some add-ons to consider.

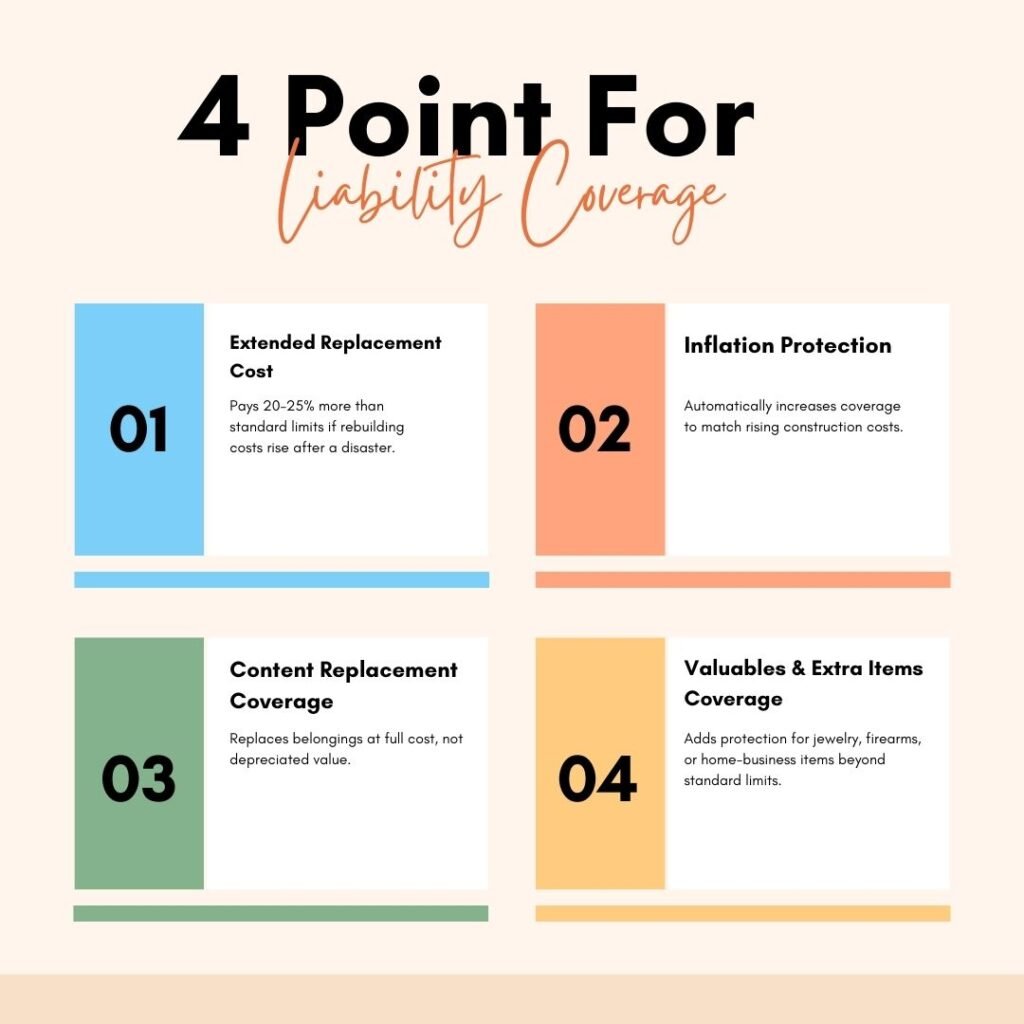

Extended replacement cost: covers your home beyond standard limits. A standard policy rebuilds your home up to a set amount. Extended replacement cost pays 20–25% more if building costs rise after a disaster. Coverage varies by state and insurer, so check details before buying. This covers standard building materials. Custom features, like stained-glass windows or antique floors, need extra riders or a restoration-cost policy.

High-end home policies may offer guaranteed replacement cost. This more expensive coverage pays to fully replace or repair your home, even above policy limits.

When shopping for the Lowest Home Owners Insurance, compare these options carefully. Choosing the right coverage ensures your home is fully protected without overspending.

Inflation protection, or inflation guard, automatically raises your dwelling coverage to match rising building costs. Most homeowners policies include it, but with prices climbing, confirm the coverage with your agent.

When looking for the Lowest Home Owners Insurance, ensure inflation protection is included to keep your home fully covered without paying too much.

Earthquake, hail, and windstorm coverage protects against natural disasters. Many states require separate deductibles or stand-alone coverage for these events.

Content replacement coverage pays to replace your belongings at full cost, not just depreciated value. Make a video inventory of your possessions and store it safely.

Additional valuables like jewelry, furs, firearms, and home-business items often have low limits. Consider a floater to fully cover expensive items.

Sewer backup coverage protects against municipal or septic failures that flood your home. Costs vary from $50 to several hundred per year, and limits can range up to the full cost of your home. Damage from sump pumps is covered, but the pump itself is not.

Ordinance or law coverage helps rebuild your home to meet updated local building codes. This is useful for older homes.

When shopping for the Lowest Home Owners Insurance, check for these extra coverages. Adding them can increase premiums slightly but ensures your home and possessions are fully protected without leaving gaps.

Here are some easy ways to lower your Lowest Home Owners Insurance premiums:

Bundle coverage. Combine home and auto insurance from the same company. You could save up to 30%. Adding boat or motorcycle coverage may save more.

Raise your deductible. Higher deductibles mean lower premiums. For example, moving from $500 to $1,000 can cut your cost by double digits.

Make home improvements. Update plumbing, add a security system, or install water- or gas-leak sensors. Each can save 2–6%. A new impact-resistant roof can save up to 35%. Clearing dry brush in fire-prone areas can earn a 5% discount.

Use these tips to get the Lowest Home Owners Insurance without cutting coverage.