Planning for the future is more than saving money or building a career. It means securing your loved ones and making your assets grow. One powerful tool for this is Insurance Life Universal. Unlike term life insurance, it offers lifelong protection. It also provides flexible premiums and a cash value that grows over time.

Insurance Life Universal is more than a safety net. It adapts to your changing financial needs. Whether protecting your family, building wealth, or leaving a legacy, this insurance can form the foundation of long-term security.

Let’s look at the key features of Insurance Life Universal and why it stands out from other financial options.

Insurance Life Universal is a permanent life insurance. It gives lifelong coverage with flexible premiums. It also has a tax-deferred savings component.

This insurance is for people who want control. You decide how much to pay and how your cash value grows.

Unlike term life insurance, Insurance Life Universal offers permanent protection. Coverage lasts as long as premiums are paid.

The main advantage is flexibility. You can adjust premiums and death benefits. It adapts to your changing financial needs.

Understanding Insurance Life Universal is key for smart financial choices. This insurance combines life coverage with a cash value. You save money over time while securing your family’s future.

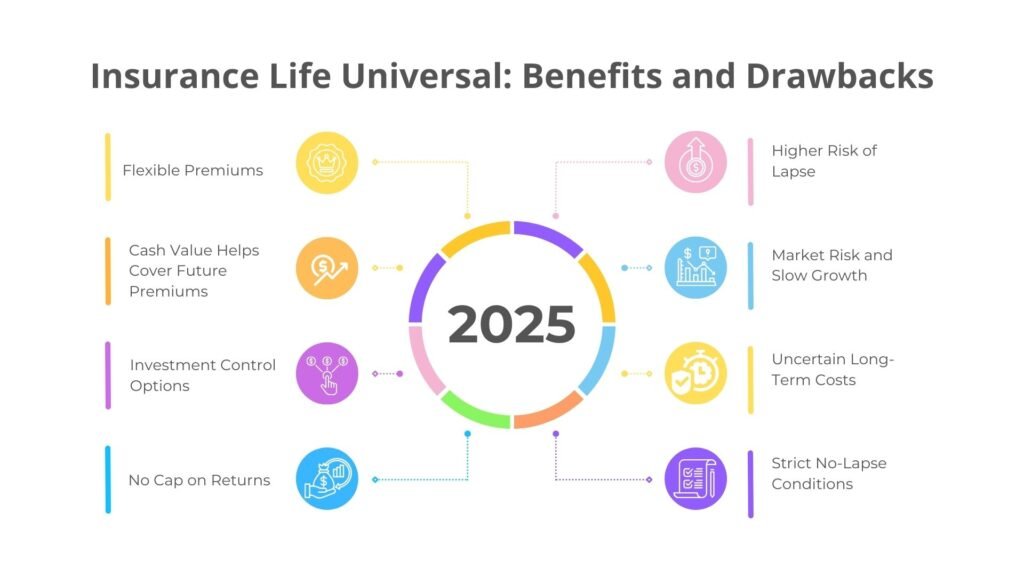

Insurance Life Universal offers flexible premiums. Unlike whole life insurance with fixed payments, you can adjust the amount and frequency. This helps if your financial situation changes.

Cost of Insurance (COI): This covers your life insurance costs, including mortality charges and fees.

Cash Value Component: The rest goes into a cash value account. It grows over time with interest. You may borrow against it or make withdrawals, depending on your policy.

Flexible Premiums With Insurance Life Universal, you can adjust payments. Pay more to grow cash value. Pay less when money is tight. For example, increase $300 to $500 after a bonus to boost savings. Reduce to $150 during hard times if cash value covers it. Whole life policies don’t offer this flexibility.

Investment Component: Part of your premium goes into a cash value account. It may grow based on market performance. Gains or losses depend on how funds are managed.

Transparency Costs, fees, and performance are clear. You see exactly what you pay and how your policy performs.

Insurance Life Universal is ideal for those who want control over life insurance as their financial needs change.

Benefits of Insurance Life Universal

Drawbacks of Insurance Life Universal

Insurance Life Universal offers flexibility and growth, but it requires careful management to avoid risks.

Young, Newlywed Couples Young couples get low rates and time to build cash value. Early higher payments can grow savings. Later, premiums can be reduced or death benefits increased. Cash value can help cover child care or family costs.

Decision: Choose Insurance Life Universal if you can afford higher early premiums and want investment growth.

Business Owners Business owners can select indexed or variable universal policies. Cash value can grow fast and pay future premiums. It can also finance business expenses or expand life coverage.

Decision: Choose Insurance Life Universal for tax-deferred growth and business or estate planning.

Sole Financial Providers If your family depends on your income, flexible premiums help during financial stress. Coverage adjusts as needed.

Decision: Essential for sole providers who need adaptable protection.

Individuals With Significant Debts Higher debt increases life insurance needs. Flexibility allows reducing death benefits and premiums as debts are paid. Cash value can help pay down debt faster.

Decision: Choose Insurance Life Universal if you have debt but expect to lower it over time.

Stay-at-Home Parents Life insurance can replace costly household services. Death benefits support the working parent. Cash value can cover debts or premiums.

Decision: Essential if your household role is costly to replace and needs change as children grow.

Insurance Life Universal is ideal for those who want flexible premiums and investment growth. It provides long-term coverage. You must manage the costs carefully. Consider it as part of your financial plan.

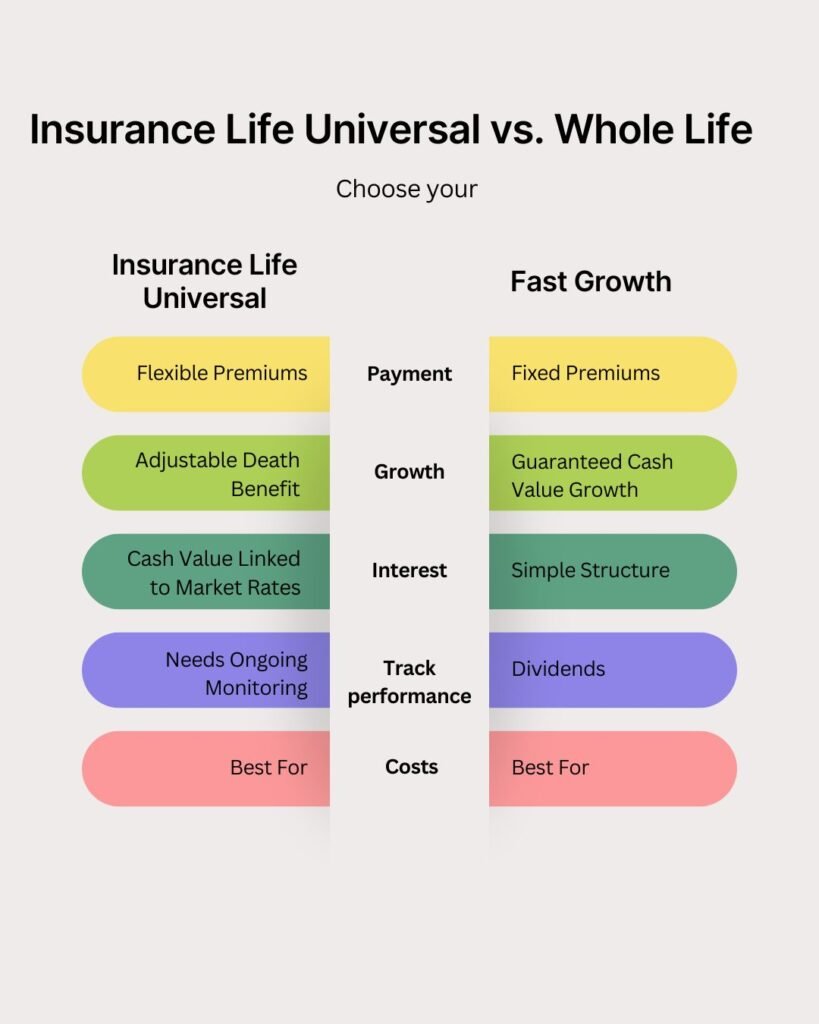

The main difference is flexibility and duration. Term life is affordable and lasts for a set time. Insurance Life Universal offers lifetime coverage and cash value growth.

| Feature | Term Life | Insurance Life Universal |

| Coverage | Fixed term (10–30 years) | Lifetime, as long as premiums are paid |

| Premiums | Low and fixed | Higher but flexible; adjustable |

| Cash Value | None | Builds over time; can borrow or use |

| Complexity | Simple | More complex; needs active management |

| Best For | Temporary needs like income or mortgage | Long-term planning, wealth building, estate strategies |

Term life suits those needing coverage for a set period and low costs. Insurance Life Universal is better for permanent protection, flexible premiums, and cash value growth. It requires active management

Both are permanent life insurance with lifelong coverage and cash value. The key differences are flexibility, investment, and cost.

Insurance Life Universal

Whole Life Insurance

Insurance Life Universal suits those who want flexibility and control. Whole life is ideal for those who prefer predictability and minimal management.

Traditional (Non-Guaranteed) Insurance Life Universal This is the simplest and most affordable type. Premiums are flexible, and death benefits can be adjusted. Cash value grows modestly. No guarantees—policy may lapse if cash value drops or premiums are underfunded. Best for those who want low-cost coverage and can monitor the policy.

No-Lapse Guaranteed Insurance Life Universal (GUL) Provides long-term coverage with a no-lapse guarantee if minimum premiums are paid. Cash value growth is small. Less monitoring is needed. Ideal for those who want flexibility but a set-it-and-forget-it policy.

Indexed Insurance Life Universal (IUL) Cash value growth links to a market index, like the S&P 500. Returns have a guaranteed minimum and a cap. Growth can be faster than traditional UL but carries market risk. Suitable for those comfortable with market trends or using a financial advisor.

Variable Insurance Life Universal (VUL) Allows direct investment of cash value in stocks, bonds, or money markets. Offers high growth potential but high risk. Poor performance can cause lapses or need extra payments. Best for experienced investors seeking long-term tax-deferred growth.

Riders add flexibility and extra protection to Insurance Life Universal policies. They help your coverage adapt to life changes.

Accelerated Death Benefit Rider: Access part of the death benefit early if diagnosed with a terminal illness. Provides financial relief when needed.

Waiver of Premium Rider: If you become disabled, premiums are waived. Coverage continues without financial strain.

Guaranteed Insurability Rider: Buy more insurance at certain times without a medical exam. Increases coverage as life changes.

Child Term Rider: Adds temporary coverage for your children. Can convert to permanent insurance later without exams.

Long-Term Care Rider: Use part of the death benefit to pay for long-term care. Helps manage costs during tough times.

Riders make Insurance Life Universal policies more adaptable and secure for long-term planning.

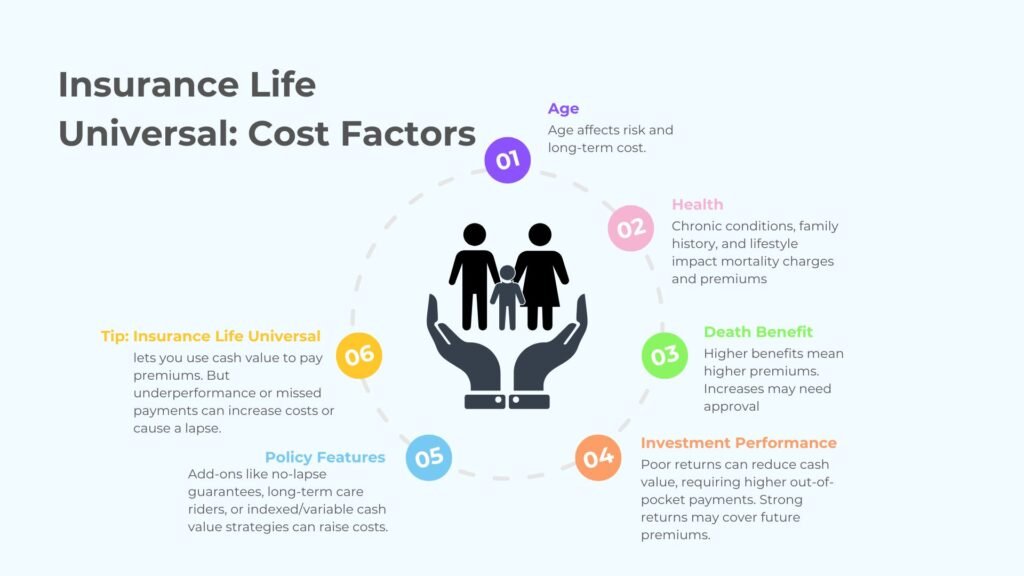

Insurance Life Universal usually costs more than term life. It combines lifelong coverage with an investment component. Premiums are flexible and can change based on policy performance.

Age: Younger buyers pay lower premiums. Age affects risk and long-term cost.

Health: Chronic conditions, family history, and lifestyle impact mortality charges and premiums.

Death Benefit: Higher benefits mean higher premiums. Increases may need approval.

Investment Performance: Poor returns can reduce cash value, requiring higher out-of-pocket payments. Strong returns may cover future premiums.

Policy Features: Add-ons like no-lapse guarantees, long-term care riders, or indexed/variable cash value strategies can raise costs.

Tip: Insurance Life Universal lets you use cash value to pay premiums. But underperformance or missed payments can increase costs or cause a lapse.

Weigh your goals, risk tolerance, and willingness to manage your policy. Flexibility comes at a price but offers long-term benefits.

Managing Insurance Life Universal requires regular checks. Adjustments keep coverage on track, prevent lapses, and grow cash value.

Insurance Life Universal combines permanent coverage with flexible premiums and a cash value component. It gives more control than whole life policies but is more complex.

This policy works well for long-term protection. You must manage cash value and monitor performance. Make sure the benefits fit your goals and your willingness to adjust the policy over time.