Do You Need Home Insurance For Bare Land? Quick Facts: – Not required by law if you fully own the land. – Liability coverage is smart to protect against accidents. – If you have a mortgage, the lender may require insurance.

Ever asked, “Do I need Home Insurance for Bare Land?” Many people do. Owning land feels simple, but risks exist.

Vacant land may look calm, but accidents can happen. Someone could get hurt on your property. Legal trouble can follow. Insurance is not just for buildings—it protects you from surprises.

Even if not required, liability coverage for bare land is wise. It shields you from costs if accidents occur. If your land has a mortgage, insurance might be mandatory. Protecting your land with home insurance for bare land is smart and safe.

Vacant land can have risks. For example, accidents or damage can happen if it’s left unused. That’s why home insurance for bare land is important.

Insurance for bare land may cost more and have limits. Some insurers may even refuse coverage if the land stays vacant too long.

A property may be considered “vacant” if:

For example, if you buy land to build a home later, it may be empty for months. You should tell your insurer. They can explain your options and limits.

Since vacant land isn’t used or maintained, it can have extra risks. That’s why home insurance for bare land is different from regular home insurance. It protects your investment and peace of mind.

Not all insurers treat vacant land the same. But generally, home insurance for bare land can cover risks like:

Standard coverage usually does not cover personal property or water damage. Some policies add endorsements for extra protection.

An insurance agent can help you find the right coverage. They can explain if your insurer offers a separate policy or an endorsement for your bare land.

Insurance companies have different rules for vacant land. You may need home insurance for bare land if you recently bought land but won’t use it soon, inherited property you won’t occupy, or plan to sell the land while it stays empty. It’s also important if you moved out and plan to build or rent in the future, or if your land is under renovation.

For land you own outright, insurance is optional, but it’s wise to protect yourself from unexpected risks. If the land is mortgaged, the lender will likely require home insurance for bare land to safeguard their investment.

Understanding the difference matters when getting home insurance for bare land. Vacant land is empty with no buildings or use. Unoccupied land may have structures but no one lives there. Knowing the difference helps you choose the right coverage.

Vacant land is empty. No homes, buildings, or even sheds. You might wonder, “Do I need insurance for this land?” The answer is yes for safety. Even without structures, you can be responsible if someone gets hurt. Home insurance for bare land helps protect you from these risks.

Unoccupied land has buildings or structures but is not in use. Think of a house for sale or a cabin in winter. The property is ready for use but temporarily empty. Home insurance for bare land can still help protect it from damage or liability.

Vacant and unoccupied land differ by tenants and belongings. Unoccupied land may have furniture, utilities, or signs people will return. Vacant land has none. It’s empty.

This difference matters. Insurance for vacant land focuses on liability. You need protection if someone is hurt. Unoccupied land may need more coverage, including the buildings and their contents.

Insurers see risks differently. Vacant land has mainly liability risks. Unoccupied land can face vandalism, theft, or hidden damage like water leaks.

Policy terms also vary. Always tell your insurer the true status of your land. This ensures the right home insurance for bare land and avoids gaps in coverage.

The key is simple: vacant land is empty, unoccupied land has structures or items. Knowing this helps you pick the right coverage, level of protection, and cost.

Buying insurance for bare land is like buying regular home insurance. You can get a standalone policy or add it to your current policy. Knowing your options helps you find the best coverage and price.

Before requesting quotes, think about your needs and budget. Look for companies with easy online access or good reviews. If money is tight, check for discounts. Knowing what you want makes buying home insurance for bare land easier.

Vacant land may seem safe, but risks are real. Knowing them shows why home insurance for bare land is smart.

Hunters may enter rural land. If they get hurt, you could be liable.

ATVs are fun but risky. Accidents can lead to serious injuries and lawsuits.

Hikers exploring your land may fall or get hurt. You could face medical or legal costs.

Even small incidents can lead to big legal bills. Defense costs rise fast, even if you win.

Medical expenses for injuries on your land can be high. Serious injuries can cost a lot over time.

Accidents don’t care if your land is empty. Whether it’s a forest plot or a wide field, risks exist.

Protecting yourself with home insurance for bare land helps cover liability and unexpected costs. It gives peace of mind and keeps your property safe from financial strain.

Protecting your vacant land starts with the right insurance. Home insurance for bare land gives you peace of mind.

First, check your current homeowners policy. Some policies can be extended to cover vacant land. This is often the easiest and cheapest option.

Know what’s covered. Most extensions include liability but may not cover the land itself.

Check for limits. Coverage might depend on land size or how you use it. Understanding these details ensures you get the protection you need.

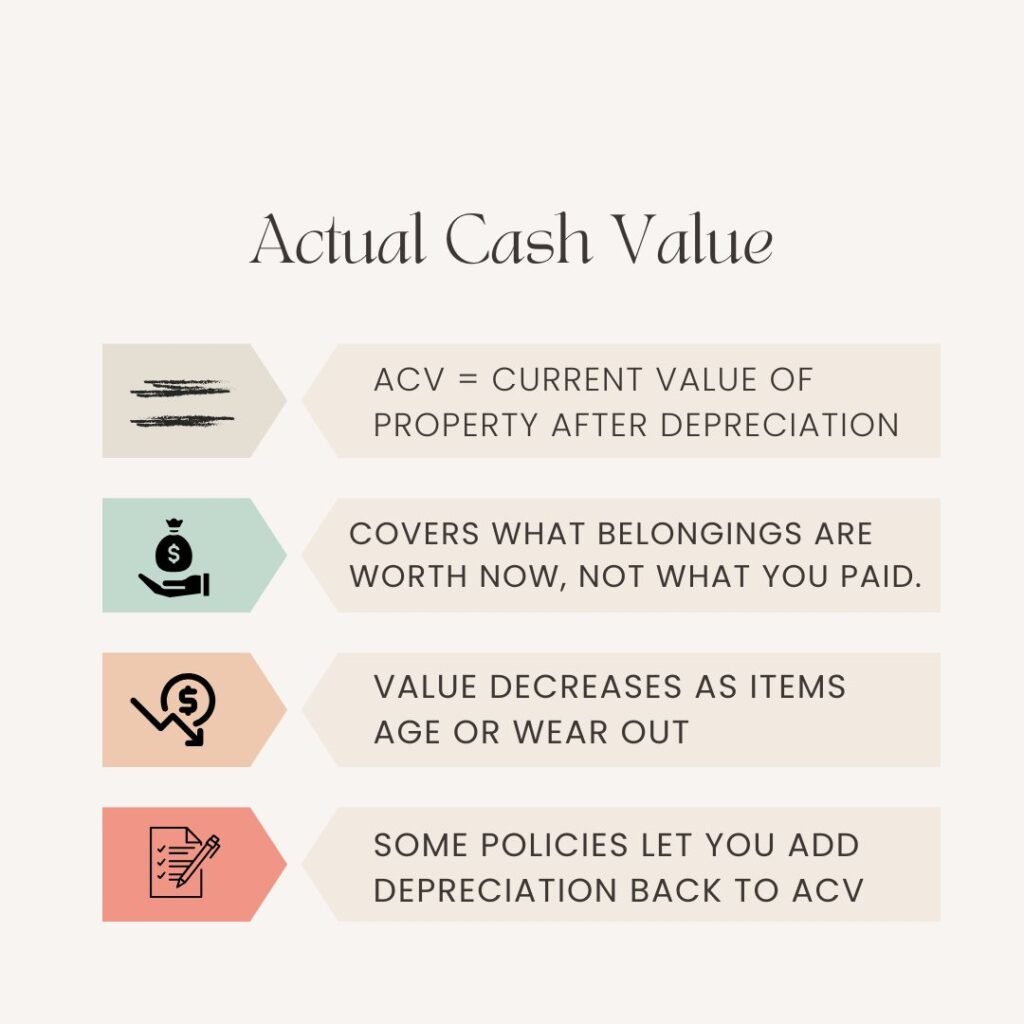

Actual cash value (ACV) covers what your property and belongings are worth now, not what you paid. It accounts for depreciation. Some policies let you recover depreciation, adding it back to the ACV. Home insurance for bare land may include this if you have structures or improvements on the property.

Replacement cost covers the value of your property and belongings without subtracting depreciation. It lets you repair or rebuild up to the original value. Home insurance for bare land with structures may offer this to fully protect your investment.

This is the most complete coverage. It pays to repair or rebuild your home even if costs go above your policy limit. Some insurers offer an extended version, usually 20–25% above the limit.

Experts suggest all homeowners choose guaranteed replacement cost. Prices rise over time, and this coverage ensures you can rebuild at today’s cost. For home insurance for bare land with structures, this gives extra protection and peace of mind.

Owning vacant or bare land may seem low-risk, but accidents and liabilities can happen. Home insurance for bare land protects you from unexpected costs, whether someone gets hurt, property is damaged, or legal claims arise.

Vacant land is empty with no structures, while unoccupied land may have buildings or belongings but is temporarily unused. This difference affects the type of coverage you need. Vacant land often requires liability coverage, while unoccupied land may need broader protection for structures and contents.

Insurance for bare land can cover risks like fire, lightning, hail, wind, explosions, and civil unrest. Policies vary: some offer actual cash value (ACV), replacement cost, or guaranteed/extended replacement cost for structures or improvements.

Buying home insurance for bare land is like standard home insurance. You can get a standalone policy or an extension of your current policy. Before buying, consider your budget, coverage needs, and provider options. Always disclose the correct status of your land to avoid coverage gaps.

Common risks include injuries to hunters, hikers, or ATV riders, as well as potential legal and medical costs. Insurance gives peace of mind and protects your investment, whether the land is empty or has structures.

Overall, home insurance for bare land is optional if you own land outright, but it’s wise. If mortgaged, lenders usually require it. Proper coverage ensures your property remains safe from liability, damage, and financial strain.