Are you a photographer in New York wondering why your insurance quote feels so much higher than what your friend in Ohio pays? You are not alone. Thousands of New York photographers search for general liability insurance for photographer in New York cost every single month. They want real numbers, honest answers, and a clear plan. This guide gives you all three. You will learn exactly what general liability insurance costs in New York, what drives your premium up or down, and how to get solid coverage without draining your bank account. From solo freelancers in Queens to busy wedding studios in Manhattan, this guide covers every scenario.

General liability insurance is your financial safety net. It steps in the moment a third party — a client, a venue manager, a wedding guest — suffers a bodily injury or property damage because of your photography business operations. Think of it as a financial bodyguard that shows up when things go sideways on a shoot. You back up to grab a wider angle, knock over a $3,000 vintage floor lamp, and watch it shatter across a newly refinished floor. Without coverage, that bill lands entirely on you.

Beyond the basics, general liability coverage also protects you from personal and advertising injury claims. If someone accuses you of using their image without permission, defaming a competitor on social media, or running an ad with a copyrighted photo, your policy handles the legal fallout. In New York’s notoriously litigious environment, that protection is not optional. It is the absolute baseline every working photographer needs before stepping onto any paid shoot.

If you accept money for photography anywhere in New York — even just occasionally — you need this policy in place. That includes wedding photographers, portrait photographers, commercial photographers, event photographers, real estate photographers, and drone operators alike. Whether you shoot elopements in Central Park or product campaigns in a Soho studio, the risk equation is the same. Clients, venues, and permit authorities all expect proof of coverage before they let you through the door. Not having it does not just expose you financially — it costs you bookings.

Here is the number most people bury deep in their articles. New York photographers pay significantly more than the national average for photographer liability insurance. Nationally, general liability insurance for photographers averages $24 per month or $292 annually. However, New York general liability insurance runs $33 to $560 monthly, varying with your business size, industry risk, and whether you operate in NYC or upstate. That gap is not random. New York has earned it through its dense urban environment, aggressive litigation culture, and strict venue insurance requirements that no other state matches.

Among photographers and videographers, 90% pay less than $50 per month for general liability coverage. In fact, over a third — 35% — pay $25 or less per month. So while the average sits around $29 to $34 monthly, your actual rate depends heavily on your specific business profile. The photography insurance annual cost for a full bundle of GL, workers’ comp, and professional liability can reach $1,355 per year nationally — and meaningfully more in New York due to the state’s elevated risk environment.

| Coverage Type | National Average | New York Average |

|---|---|---|

| General Liability | $24/mo ($292/yr) | $29–$34/mo ($350–$408/yr) |

| Business Owner’s Policy (BOP) | $32/mo ($385/yr) | $47–$49/mo ($564–$588/yr) |

| Workers’ Compensation | $17/mo ($205/yr) | $20/mo ($240/yr) |

| Professional Liability (E&O) | $64/mo ($765/yr) | $74/mo+ ($888/yr+) |

| Full Insurance Bundle | $113/mo ($1,355/yr) | $130–$160/mo |

| Single-Event Policy | $59–$75 one-time | $75–$100 one-time |

The type of photography you do shapes your premium more than most people realize. For example, a home-based portrait photographer shooting two weekend sessions in Queens might pay as little as $408 annually for solid general liability coverage. A full-service wedding photography business New York studio in Manhattan with two employees, $200,000 in annual revenue, and a company van transporting equipment to events could pay $1,500 or more for a comprehensive bundle. Weekend photographers earning $30,000 from occasional family portraits operate quite differently than established studios booking $180,000 in commercial work. Your premium reflects that reality precisely.

📞 Not sure what you’ll pay? Call OLPolicy at (866) 757-5350 — we give you a real number in minutes.

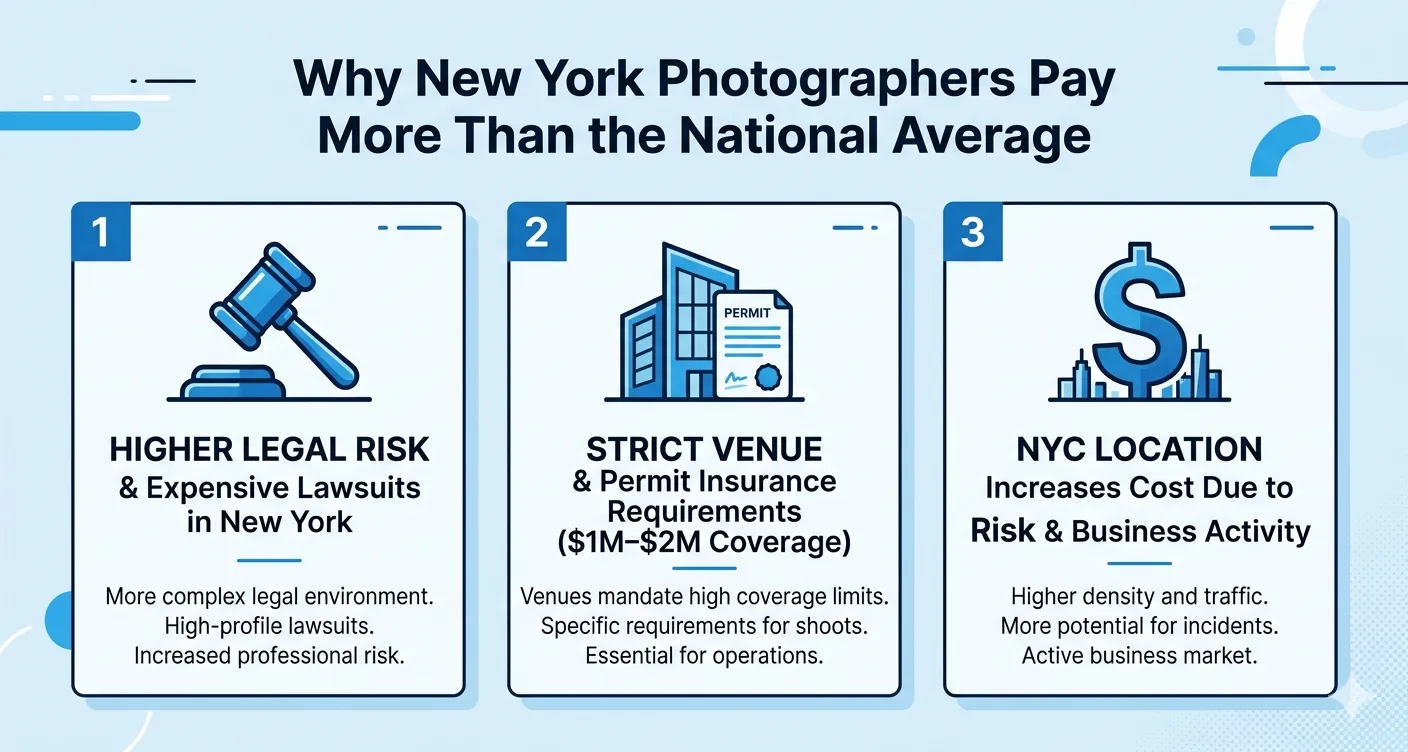

New York is not just expensive to live in — it is expensive to get sued in. The state carries one of the most plaintiff-friendly legal environments in America. Manhattan juries regularly hand down what insurance analysts call nuclear verdicts — settlements large enough to obliterate any small photography business that lacks adequate protection. New York’s premium sits $57 above the national average, making it the second-most expensive state for general liability insurance in the entire country. That legal reality bakes itself directly into every underwriting calculation for New York-based businesses.

Beyond the courtroom, New York venues enforce some of the strictest insurance thresholds in the country. Premium rooftop venues in Tribeca, luxury ballrooms in Midtown, and historic estates in the Hudson Valley routinely require $2 million in general liability coverage aggregate before handing you a vendor agreement. DCAS requires general liability insurance of $1,000,000 with an aggregate of $2,000,000, with the City of New York named as additional insured. Photographers in other states simply do not face these institutional demands. You do, every single booking season.

Location within New York is one of the most powerful price multipliers underwriters apply. New York sole proprietors pay $88 monthly on average, while businesses with one to four employees pay $180 monthly. A solo freelance photographer based in Syracuse pays a fraction of what a two-person photography studio small business in Midtown Manhattan shells out each quarter. NYC’s crowded streets, dense pedestrian traffic, and high-rise construction environments create elevated third-party injury risk that underwriters price into every New York City ZIP code. Location is not just a detail on your application. It is a permanent price multiplier.

Your premium is not a random number. Underwriters build it from a specific checklist of variables, and knowing what they evaluate puts you in a stronger position when shopping for coverage. Your photography specialty matters enormously. Insurance carriers consider your line of work, the size of your business, your annual revenue, and the types of additional insured endorsements your clients and venues demand. Wedding and event photographers face higher perceived risk than product or portrait shooters because they operate in uncontrolled environments with large crowds, alcohol service, and expensive venue décor.

Several additional factors move your number up or down significantly. Your drone photography insurance New York add-on, the number of W-2 employees versus 1099 contractors, and whether you rent commercial studio space all contribute to your final quote. Expensive camera equipment, a history of prior claims, and events involving alcohol all push premiums higher. The good news is that several of these variables are directly within your control — and the right broker helps you structure your coverage to minimize unnecessary cost.

| Rating Factor | Impact on Premium |

|---|---|

| Wedding/event photography specialty | Increases premium |

| NYC location vs. upstate New York | Increases premium significantly |

| Prior claims history (past 3–5 years) | Increases premium 15–30% |

| Annual revenue over $100,000 | Increases premium |

| Drone operations | Adds $200–$500/yr endorsement |

| W-2 employees on staff | Triggers workers’ comp requirement |

| Commercial studio space rental | Adds commercial property exposure |

| Events involving alcohol | Elevates bodily injury risk rating |

| Zero claims history | Reduces premium 15–30% |

| Annual payment vs. monthly billing | Reduces premium 5–10% |

One prior claim can follow your photography business for three to five renewal cycles. If a bodily injury claim from a 2023 wedding shoot still sits in your file, your 2026 renewal premium reflects it — sometimes 15 to 30% above standard market rates. Businesses with documented safety programs, clear on-set hazard prevention protocols, and clean claims histories consistently earn preferred pricing tiers. Maintaining a clean claims history is not just good professionalism. For New York photographers, it is one of the most powerful long-term cost-reduction tools available — and a good broker reminds you of this every renewal cycle.

Think about this for a moment. You are photographing a corporate event in a rented Manhattan ballroom. A guest trips over your extension cord, falls hard, and breaks their wrist. Emergency room costs in Manhattan easily hit $25,000 for that injury alone. Your general liability insurance covers their medical treatment, lost wages they claim, and your full legal defense if they file suit. Without it, every dollar of that comes directly out of your business account. That one protection alone can be the difference between a thriving photography career and financial ruin.

However, bodily injury coverage is just the beginning. General liability policies also include personal and advertising injury, no-fault medical expenses, and damage to rented premises. Personal and advertising injury is the coverage most photographers underestimate. If you accidentally use a copyrighted image in your marketing, publish a post that defames another photographer, or run an ad featuring a client without a signed release, your policy handles the legal fallout. In New York’s competitive photography market — where everyone watches everyone else — that exposure is very real and growing every year.

| What GL Covers | What GL Does NOT Cover |

|---|---|

| Third-party bodily injury | Your own camera equipment |

| Client property damage | Professional errors or missed shots |

| Personal and advertising injury | Data loss from corrupted memory cards |

| Damage to rented venue (up to $100K) | Employee injuries on the job |

| Legal defense costs | Your own vehicle damage |

| No-fault medical payments | Drone incidents without endorsement |

| Copyright infringement defense | Intentional acts or fraud |

These are not hypotheticals. A wedding photographer’s C-stand tips over during a Tribeca reception and fractures a guest’s collarbone — that is a bodily injury claim worth tens of thousands of dollars. A commercial photographer’s equipment bag scuffs a grand piano at a private event venue during setup — that triggers a third-party property damage claim. A portrait photographer runs a Facebook ad campaign using a behind-the-scenes image of a client without a signed release, and that client sues for unauthorized use — that falls squarely under personal and advertising injury coverage. These situations happen more often than most photographers want to admit, and general liability is what keeps the business standing afterward.

Think of your insurance portfolio like your camera bag. General liability is the camera body — fundamental and non-negotiable. Everything else is a lens you add based on the specific work you do. Professional liability insurance — also called errors and omissions — is the first additional lens most New York photographers need. Freelance photographers pay an average of $34 per month for professional liability insurance. A bride who feels her ceremony was inadequately captured can sue for a partial or full refund, and professional liability handles that dispute so it never reaches your personal finances.

However, the business owner’s policy for photographers deserves equal attention from anyone running a real photography business. A BOP bundles general liability and property insurance at a discounted rate, and often includes business interruption insurance — which replaces lost income if your studio closes unexpectedly after a covered event like a fire or flood. Then there is inland marine insurance, which your homeowner’s policy almost certainly excludes. Professionals carrying $15,000 or more in camera gear, lenses, and lighting need inland marine coverage, because standard policies simply were not built to protect commercial equipment traveling between job sites.

| Coverage | What It Covers | NY Monthly Cost | Essential? |

|---|---|---|---|

| General Liability | Third-party injury and property damage | $29–$34/mo | Yes — always |

| Professional Liability (E&O) | Client disputes and delivery failures | $34–$74/mo | Yes — strongly recommended |

| BOP (GL + Property) | GL plus studio and equipment on premises | $47–$49/mo | Yes — if you have studio space |

| Inland Marine | Camera gear anywhere it travels | $15–$30/mo | Yes — if gear exceeds $5,000 |

| Workers’ Compensation | Employee injuries on the job | $20/mo (NY avg) | Yes — legally required with employees |

| Commercial Umbrella | Excess liability over base limits | $15–$25/mo | Recommended for commercial shoots |

| Drone Liability | Aerial photography incidents | $200–$500/yr add-on | Yes — if you fly commercially |

For most established New York photographers, a BOP beats standalone general liability on pure math. The $15 to $20 monthly difference between a BOP and standalone GL buys you commercial property protection for your studio space, stored lighting equipment, computers, and backup drives. You can often add business interruption insurance to a BOP to protect against the costs of a temporary shutdown tied to a covered property claim. For example, this would help pay employee wages and temporary studio rental costs if your space closes for renovation after a fire. That level of protection for roughly fifteen extra dollars per month is one of the most straightforward decisions in running a photography business.

Getting the right photography business insurance New York comes down to two things — choosing a broker who understands the photography industry specifically, and shopping across multiple top-rated carriers to find the best rate for your exact risk profile. A generalist broker who handles car insurance, homeowner’s policies, and business coverage all day may not know that NYC venues require specific additional insured language, that MOME permits require broker-submitted COIs, or that drone endorsements are a separate line item most base policies exclude entirely. Working with a specialist makes all the difference when a venue calls you the night before a shoot asking for a same-day certificate.

At OLPolicy, the team works specifically with New York photographers to match each client with the right carrier for their business type, revenue level, and coverage needs. Whether you are a freelance photographer insurance New York client shooting occasional portrait sessions or a photography studio small business owner managing multiple shooters and a commercial lease, the right policy exists at the right price. What changes is knowing where to find it — and having someone in your corner who submits the paperwork correctly the first time.

New York has a regulatory and legal framework that most generic insurance guides completely ignore — and that ignorance costs photographers real money at the worst possible moments. First, workers’ compensation insurance New York photographer requirements are non-negotiable. In New York, workers’ compensation becomes mandatory the moment you hire a single employee — including part-time photo assistants, second shooters paid as W-2 employees, or studio coordinators. Non-compliance with New York’s Workers’ Compensation Board carries steep penalties, and misclassifying employees as independent contractors to sidestep this requirement is a well-documented audit trigger.

At least 48 hours before you file your project application, your insurance broker or agent must email a certificate of insurance (COI), a broker certification, and an additional insured endorsement to the NYC Mayor’s Office of Media and Entertainment (MOME) at insurance@media.nyc.gov. The Film Office will not accept documentation submitted by the photographer directly — it must come from a licensed broker. On the COI, the Descriptions of Operations box must read exactly: “The City of New York, including its officials and employees, is additional insured.” A single word out of place delays your entire permit. OLPolicy handles this submission process for New York photographers every day — call (866) 757-5350 if you have a deadline approaching.

| Requirement | Detail |

|---|---|

| Minimum coverage | $1,000,000 per occurrence |

| Additional insured wording | “The City of New York, including its officials and employees, is additional insured” |

| Who submits COI | Licensed insurance broker only — not the photographer |

| Where to send COI | insurance@media.nyc.gov |

| Submission deadline | At least 48 hours before permit application |

| Business name on COI | Must match permit application exactly — including LLC, Inc., spacing, punctuation |

| DCAS property shoots | $1M per occurrence / $2M aggregate required |

| Workers’ comp | Required alongside GL for any staffed shoot |

Flying a drone commercially in New York City without correct insurance documentation is a genuinely expensive mistake. Beyond FAA Part 107 certification — mandatory for any commercial aerial photographer — New York City has its own regulatory layer. Drone liability insurance protects you if a drone-related accident injures someone or damages property, and also covers legal costs if someone claims your aerial footage violated their privacy. Most baseline general liability policies exclude drone operations entirely unless you add a specific aerial liability endorsement — typically costing $200 to $500 annually. Before your next aerial shoot in Brooklyn, Queens, or any of the five boroughs, confirm that endorsement is active. If it is not, one phone call to OLPolicy at (866) 757-5350 can add it to your policy before you fly.

Paying full sticker price on any insurance policy is a choice, not a requirement. Several proven strategies reduce your photographer liability insurance cost without cutting into the protection your business actually needs. The most effective single move is bundling your coverages. Carriers consistently offer discounts when you combine general liability, commercial property, and commercial auto coverage into one policy. A business owner’s policy for photographers combining GL and commercial property consistently costs less than two separate standalone policies, often saving 10 to 15% on your combined annual premium — with the added benefit of one renewal date and one broker to call.

The second most effective strategy is paying your annual premium upfront rather than month to month. Monthly payment plans carry a processing markup of 5 to 10% per year — money that simply disappears without buying you any additional protection. Paying the full annual photography insurance annual cost in one transaction eliminates that surcharge entirely. A written on-set safety checklist is another underutilized tool. Businesses with documented safety programs and clear hazard prevention protocols consistently earn preferred pricing tiers — sometimes 15 to 30% below standard market rates. A good broker, like the team at OLPolicy, knows which carriers reward these behaviors and places your policy accordingly.

| Strategy | Estimated Saving |

|---|---|

| Bundle GL into a BOP | 10–15% on combined premium |

| Pay annual premium upfront | 5–10% vs. monthly billing |

| Maintain zero claims history | 15–30% at renewal |

| Raise deductible from $500 to $1,000–$2,500 | 5–15% monthly reduction |

| Document formal on-set safety protocols | Up to 15–30% preferred pricing |

| Review coverage limits annually | Avoid overpaying for coverage outgrown |

| Work with a photography-specialist broker | Access to preferred photographer rates unavailable to the public |

A specialist broker does more than find you a low premium. They know which carriers offer preferred rates for photographers with clean claims histories, which underwriters are most competitive for NYC-based studios versus upstate freelancers, and which policies include the additional insured endorsement language your venues will actually accept. For any working freelance photographer insurance New York professional, the difference between a generalist broker and a specialist can be $200 to $500 per year on identical coverage — and a specialist also handles the paperwork correctly so you never lose a booking over a missing COI. OLPolicy’s advisors work with New York photographers daily. Call (866) 757-5350 and find out what a specialist can actually save you.

Shopping for insurance without preparation is like showing up to a shoot with a dead battery. You gather what you need before you need it. Before requesting a quote for photography business insurance New York, pull together your legal business name exactly as registered — including LLC, Inc., or DBA designations and punctuation. Underwriters are precise about this because your proof of insurance photographer venue COI must match your business registration character for character. Also prepare two years of annual revenue figures, your total equipment replacement value, the photography specialties you offer, and any prior claims from the past three to five years.

From there, the process moves quickly. Call OLPolicy at (866) 757-5350 or submit a quote request at olpolicy.com — the team compares rates across multiple top-rated carriers for your exact profile and presents you with real options, not a generic quote. Pricing for identical coverage limits can vary 30 to 40% between carriers for the same photographer risk profile, and knowing which carrier to approach for your specific situation is what a specialist broker brings to the table. Then verify the Certificate of Insurance COI issuance timeline before committing to any policy. Many NYC venues and MOME permit applications require same-day COI delivery — OLPolicy issues these same day for most New York photographers.

Insurers are not being nosy when they ask detailed questions. They are building your precise risk profile — and the more accurately you answer, the more closely your quote reflects your actual exposure rather than a worst-case estimate. You will need your legal business name, two years of annual revenue, total employee and assistant count (both W-2 and 1099), the full replacement value of your equipment inventory, the types of photography you perform, whether you operate from a commercial studio or home base, any prior claims history, and your desired coverage limits. For sole proprietor photographer insurance applicants, this process takes under ten minutes. For studio owners with employees, plan for fifteen to twenty minutes to pull everything together before your first call.

General liability insurance for photographer in New York cost runs higher than most of the country — and for good reason. New York’s legal climate, strict venue requirements, and MOME permit mandates create a baseline exposure that photographers in other states simply do not face. But higher risk does not have to mean overpaying. Bundle your coverages into a BOP, pay annually, maintain a clean claims history, and work with a broker who knows the New York photography market inside and out. Your camera captures moments that last a lifetime. Your photography business insurance makes sure one bad moment on set does not erase everything you have built. The team at OLPolicy is ready to help you get that protection locked in today.

OLPolicy helps New York photographers get the right general liability coverage at the right price. Same-day COI. MOME permit submissions handled. Top-rated carriers compared for your specific profile.