You just got rejected from a food truck festival in Austin because you don’t have insurance. Sound familiar? So many Texas food truck owners run into this exact problem and they start searching for general liability insurance for food truck in Texas in a total panic. The good news is, it’s not complicated. Getting covered is faster and cheaper than most people think. General liability coverage protects you from customer injuries, foodborne illness claims, property damage and legal costs. It also unlocks the permits and event spots your business needs to grow.

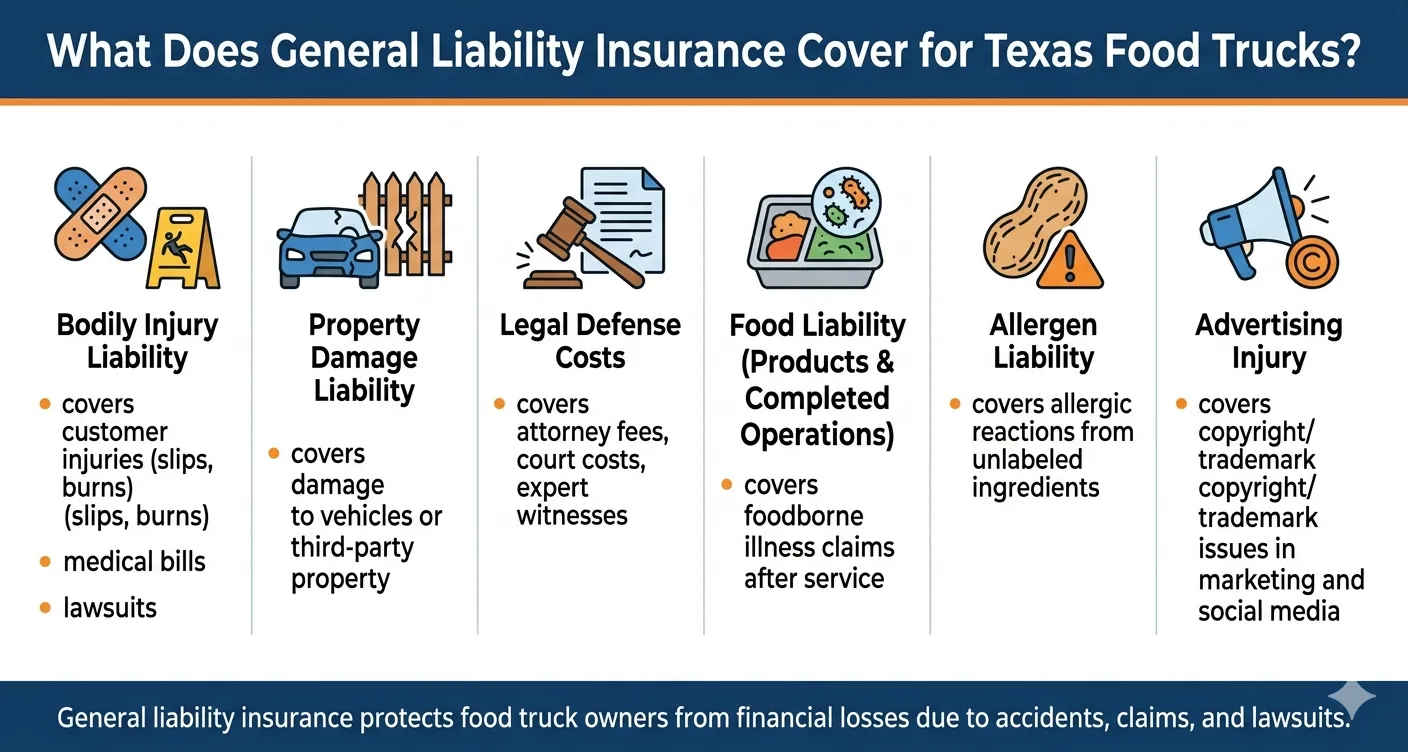

General liability insurance is a policy that pays for losses when someone outside your business gets hurt or suffers damage because of your operation. Think of it like a financial safety net. It catches you when a customer slips near your truck, claims your food made them sick or says your truck damaged their property. Bodily injury liability covers their medical bills and any legal fees that follow. Product liability insurance kicks in when someone says your food caused them harm. This one policy handles more situations than most owners realize and it’s the first thing any permit office or event organizer will ask to see.

The four main protections inside a standard policy are bodily injury, property damage, products-completed operations and advertising injury. Each one matters. If a grease splatter from your grill damages a nearby vendor’s canopy, your property damage coverage handles it. If you accidentally use a copyrighted song in a TikTok video and get sued, advertising injury protection responds. For any mobile food service business operating in Texas whether you sell tacos, lobster rolls or frozen margaritas this coverage is the foundation everything else is built on.

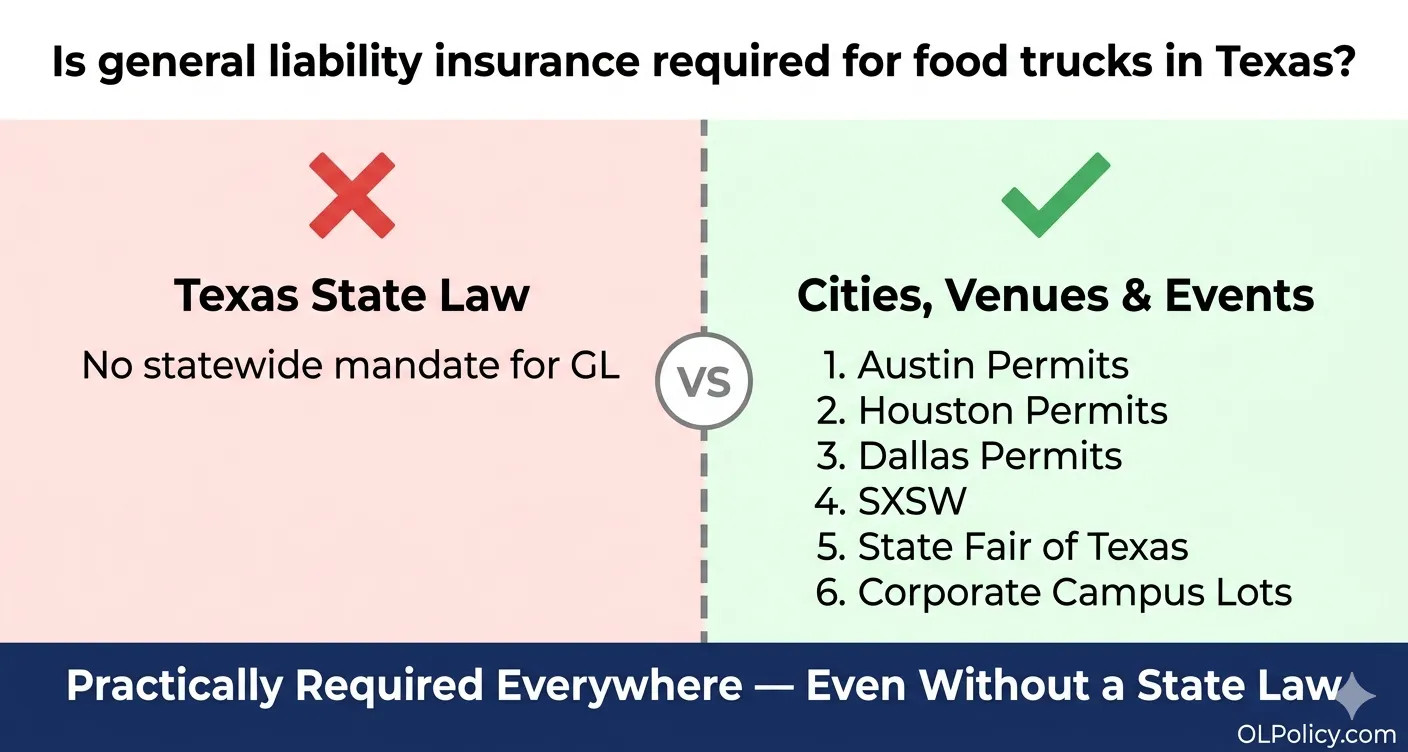

Here is something most people get wrong. Texas has no statewide law that forces every food truck owner to buy general liability insurance for a food truck in Texas. But that doesn’t mean you can skip it. The Texas Department of Insurance doesn’t mandate it at the state level however, cities, counties, private venues and event organizers almost always do. Most major Texas municipalities won’t approve your permit without proof of at least $1 million in coverage. The difference between “legally required” and “practically required” is very, very thin.

Private venue contracts are where it gets serious fast. A farmers market, a corporate office park food truck lot or a weekend music festival will hand you a vendor agreement that demands proof of liability insurance before you can set up. Without a valid certificate of insurance (COI), they simply won’t let you in. Texas local ordinances differ a lot from city to city. What a small Hill Country town requires is nothing like what Houston or Dallas demands. Always call your specific city permit office before assuming you’re already good to go.

Texas gives cities and counties a lot of room to set their own rules. Austin food truck insurance requirements include a minimum $1 million per occurrence limit tied to the city’s mobile food vendor permit. Houston food truck insurance rules are similar but often come with extra requests for coastal weather endorsements from venues near the Gulf. Dallas food truck insurance and San Antonio both follow the $1 million minimum standard. If you plan to operate in any major Texas city, you need at least $1 million in general liability coverage that’s not negotiable.

Big Texas events set the bar high. The State Fair of Texas, SXSW in Austin, the Texas Food Truck Showdown and corporate campus programs all require a valid COI before approving your vendor application. Many of these events also require an additional insured endorsement a document that names the event organizer as a protected party under your policy. This is one of the most requested documents in the food truck world and one of the most overlooked by newer operators. Providers like OLPolicy let you add an additional insured online in minutes, usually at no extra charge.

Walk through a normal week of food truck operations and you’ll find liability risk hiding everywhere. A customer trips on the step near your service window bodily injury liability covers their emergency room visit and the lawsuit that comes with it. A kid burns their hand on the edge of your hot equipment same coverage steps in. A delivery driver says your truck rolled back and scratched their door property damage coverage handles the repair bill and any dispute. These things happen to real Texas food truck owners every single year. It’s not a matter of if it’s when.

Most owners forget about the cost of just defending a claim. Even if you did nothing wrong, fighting a frivolous lawsuit in Texas can cost between $25,000 and $50,000 in legal defense costs before the case ever sees a courtroom. Your general liability policy covers attorney fees, court costs, expert witnesses and settlement costs all up to your coverage limit. That protection alone is worth more than the monthly premium many times over. One lawsuit can wipe out an entire year of profit for a small food truck operation.

Products-completed operations is the technical term for what most food truck owners call product liability. It covers claims that come up after your food leaves your hands after the customer walks away with their order. The classic example is a foodborne illness lawsuit. A customer eats your shrimp tacos on Friday, gets seriously sick on Saturday and files a claim on Monday. Even if you followed every food safety rule perfectly, you still have to respond to that claim. Your policy covers the investigation, the legal defense and any settlement reached.

Unlabeled allergen claims are rising fast in Texas and across the country. If a customer suffers a serious allergic reaction to an ingredient you didn’t clearly communicate, that’s a product liability event. The average allergen-related lawsuit in food service settles somewhere between $30,000 and $150,000. General liability coverage that includes products-completed operations is not something you choose based on budget it’s something every Texas food truck needs before serving a single customer.

Advertising injury protection is bundled into most standard general liability policies and most owners have never heard of it. It covers you if your marketing materials your social posts, your printed menus, your website accidentally copy someone else’s copyright or trademark. Running a food truck in 2025 means you’re probably posting on Instagram and TikTok every day. Using a popular song in a background video, sharing a photo that includes a copyrighted mural or picking a truck name that looks too much like a competitor’s brand all of these can trigger a claim. Your general liability coverage responds to these situations just like it responds to physical accidents.

Understanding exclusions is just as important as knowing what’s covered. General liability has clear limits. Employee injuries are the biggest one. If your line cook burns their arm on the grill or your cashier slips on a wet floor inside the truck, general liability won’t pay a single dollar. That falls under workers’ compensation insurance a completely separate policy. Vehicle accidents while your truck is on the road are another major exclusion. Those are covered by commercial auto insurance, which Texas law requires for all business vehicles operating on public roads. Texas mandates minimum auto liability limits of $30,000 bodily injury per person, $60,000 per accident and $25,000 in property damage known as the 30/60/25 minimums.

Your own equipment isn’t covered by GL either. If your generator breaks down, your fridge dies in August heat or someone steals your grill overnight, general liability won’t help at all. Food truck equipment coverage through an inland marine policy or a business owner’s policy (BOP) is what handles those losses. Food spoilage coverage is a separate add-on that pays when a power outage destroys your perishable inventory. Employer liability insurance (ELI) is another coverage layer many Texas food truck owners miss it covers negligence claims from employees that go beyond standard workers’ comp protection. Building full protection means stacking several policies together. General liability is the floor, not the ceiling.

There is also one myth worth busting right here. Many first-time operators assume their personal vehicle insurance covers them while running their food truck. It does not not even close. The moment you use your vehicle for commercial purposes, including towing your food trailer, your personal insurer has every right to deny your claim. Food trailer insurance in Texas requires a separate commercial policy entirely. Insurers enforce this exclusion consistently and without sympathy. Don’t find out the hard way.

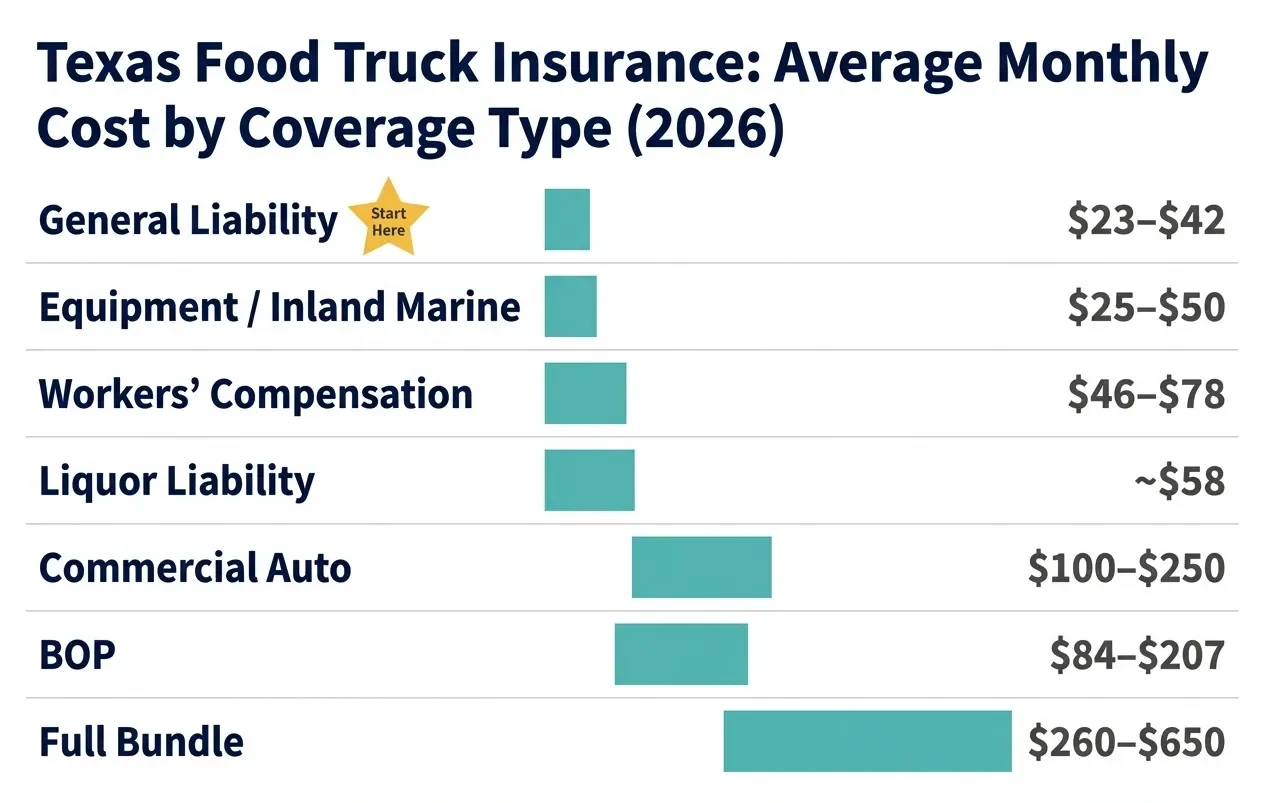

Let’s talk real numbers. According to data from Insureon, food trucks pay an average of about $42 per month or roughly $500 a year for standalone general liability coverage with a $1 million per occurrence limit. NEXT Insurance reports that 70% of their food truck customers pay between $23 and $31 per month. A full coverage package that bundles general liability, commercial auto insurance, workers’ comp and equipment protection runs most operators between $3,000 and $8,000 per year. That’s a wide range and it depends on several factors specific to your operation.

General liability insurance for a food truck in Texas costs more or less depending on your menu type, your annual revenue, how many locations you operate from and your city. A taco truck run by one person in a small East Texas town pays far less than a cocktail-and-bites truck working the Austin festival circuit six nights a week. High-heat cooking deep fryers, open-flame grilling triggers higher rates because the fire risk is greater. Insurance premium factors like claims history also matter. One past claim can raise your rate noticeably at renewal. The cleaner your record, the better your pricing.

| Coverage Type | Average Monthly Cost | Average Annual Cost | Typical Limit |

| General Liability | $23 – $42 | $300 – $500 | $1M per occurrence / $2M aggregate |

| Commercial Auto | $100 – $250 | $1,500 – $3,000 | 30/60/25 minimum (Texas law) |

| Workers’ Compensation | $46 – $78 | $548 – $940 | Per state requirements |

| Business Owner’s Policy (BOP) | $84 – $207 | $1,000 – $2,485 | $1M per occurrence / $2M aggregate |

| Liquor Liability | ~$58 | ~$700 | $1M per occurrence / $2M aggregate |

| Equipment / Inland Marine | $25 – $50 | $300 – $600 | Actual replacement value |

| Full Bundle (Recommended) | $260 – $650 | $3,000 – $8,000 | Combined |

The $1 million per occurrence limit means your insurer pays up to $1 million for a single covered incident. The $2 million aggregate limit means they pay up to $2 million in total claims across your full policy year. Most Texas city permits require a $1 million minimum that’s enough for standard street vending and small market work. However, high-traffic events like SXSW and the State Fair of Texas often require $2 million aggregate as a condition of participation. The good news moving from $1M to $2M coverage typically costs only $10 to $20 more per month. It’s almost always worth it if you plan to work large events.

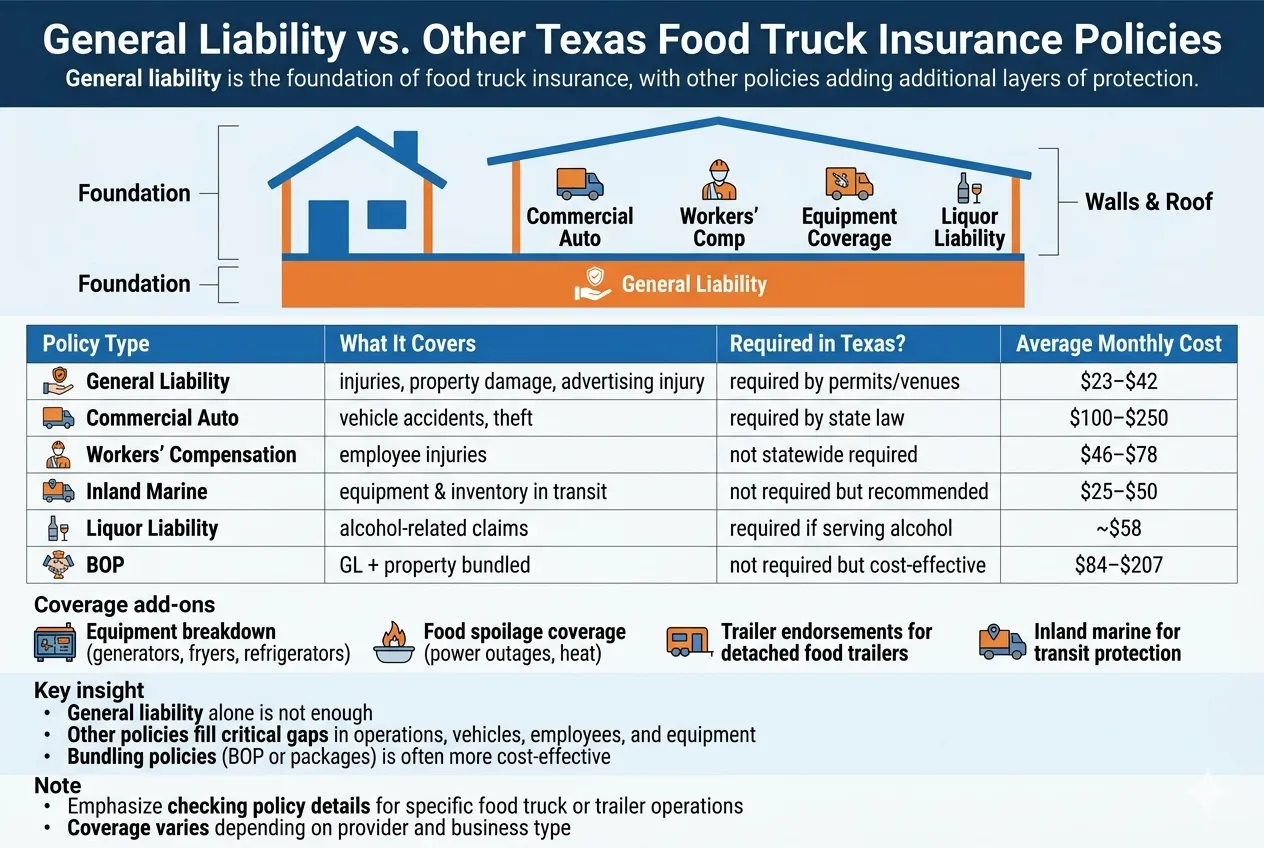

General liability is your starting point. Every other policy stacks on top of it. Think of your full coverage package like building a house GL is the foundation and commercial auto, workers’ comp, equipment coverage and liquor liability are the walls and the roof. A business owner’s policy (BOP) combines general liability and commercial property coverage into one discounted package and is often the smartest buy for established Texas food truck operators. Inland marine insurance protects your equipment and inventory while in transit between locations something a standard BOP may not fully cover.

Some providers make bundling very easy. OLPolicy food truck insurance includes general liability, business personal property and products-completed operations in one package. NEXT Insurance offers tiered Basic, Pro and Pro+ plans where you add commercial auto and workers’ comp without starting a new application. Equipment breakdown coverage for your generator, refrigerators and fryers is often available as a BOP endorsement. Food spoilage coverage can be added to protect thousands of dollars in perishable inventory from Texas summer heat events and power outages. Catering truck insurance and food vendor insurance policies follow a similar structure always ask your provider whether your specific operation type is explicitly named on the policy.

| Policy Type | What It Covers | Required in Texas? | Avg Monthly Cost |

| General Liability | Customer injuries, property damage, advertising injury | By city permit / venue contract | $23 – $42 |

| Commercial Auto | Vehicle accidents, theft, road damage | Yes state law | $100 – $250 |

| Workers’ Compensation | Employee on-the-job injuries | Not mandated statewide, but venues often require it | $46 – $78 |

| Inland Marine | Equipment and inventory in transit | No but strongly recommended | $25 – $50 |

| Liquor Liability | Alcohol-related injuries and claims | Required if serving alcohol (TABC) | ~$58 |

| BOP | GL + commercial property bundled | No but most cost-effective option | $84 – $207 |

This coverage gap trips up more Texas food truck owners than almost any other issue and most competing insurance guides skip right over it. Here is the problem. When your trailer is physically attached to your truck and moving down the road, your commercial auto policy covers both. The moment you detach that trailer and leave it sitting stationary at an event, a commissary kitchen or overnight storage your commercial auto policy may stop covering it entirely.

A food trailer endorsement added to your general liability or BOP policy specifically extends protection to a stationary, detached trailer. Without it, a theft overnight or a storm that flattens your trailer leaves you with nothing. FLIP even offers a dedicated food trailer endorsement for $12.50 per month that covers incidents occurring in, on or around your trailer when it’s detached and parked. That’s a very small price to close a very large gap. If you run a trailer-based operation anywhere in Texas, talk to your insurer about this specifically don’t assume you’re covered.

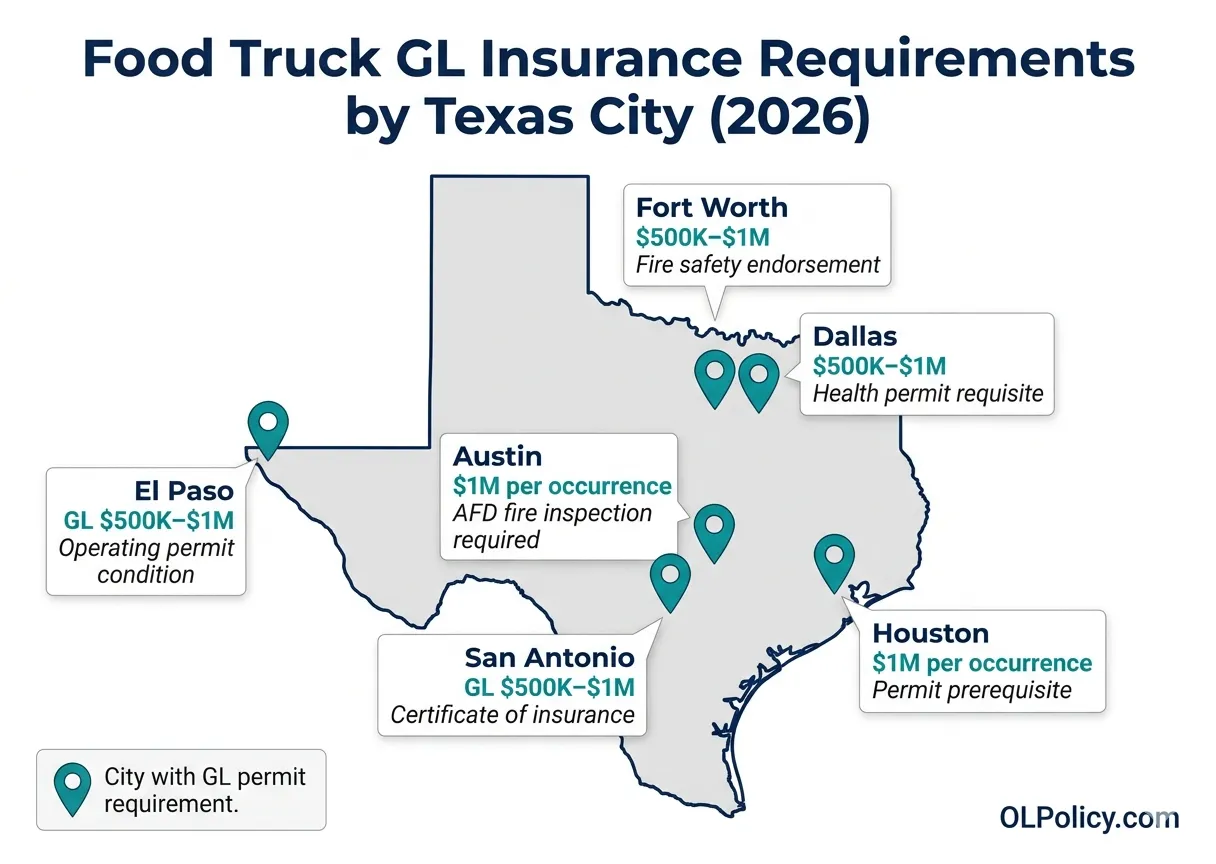

Texas is a regulatory patchwork. What works in a small Panhandle town won’t cut it on a Houston food truck park or an Austin entertainment district. Every major Texas city has its own permit rules, minimum coverage amounts and required documentation. The smartest move is calling the permit office of your specific city before you apply not after you get rejected. Austin food truck insurance requirements and Houston food truck insurance rules differ in meaningful ways and getting it wrong means delayed permits and lost business.

Dallas food truck insurance requirements follow the $1 million minimum per occurrence standard used across most major Texas cities. San Antonio mirrors that. Fort Worth uses the Tarrant County health department permitting structure. Beyond the paperwork, geography matters to your insurer too. North Texas tornado hail coverage is a real concern for DFW-area operators a single severe hail event can total a truck roof. Houston hurricane flood coverage is a separate issue standard commercial auto explicitly excludes flood damage and Gulf Coast operators need a specific endorsement or surplus lines carrier to close that gap. Commissary kitchen requirements vary by city too San Antonio, for example, requires food trucks to have a signed commissary agreement before the city will issue an operating permit.

| City | Minimum GL Required | Permit Authority | Notable Requirement |

| Austin | $1M per occurrence | Austin Development Services | AFD fire inspection + specific COI wording |

| Houston | $1M per occurrence | Houston Health Dept. | Hurricane / flood endorsement recommended |

| Dallas | $1M per occurrence | Dallas Environmental Health | Tornado / hail coverage strongly advised |

| San Antonio | $1M per occurrence | SA Metro Health | Commissary agreement required |

| Fort Worth | $1M per occurrence | Tarrant County Public Health | Annual health permit + COI |

| El Paso | $500K – $1M | El Paso Dept. of Public Health | Cross-border endorsements for Mexico ops |

This section catches Austin food truck operators off guard more than almost anything else. The Austin Fire Department requires a fire safety inspection for any food truck using open flames or gas equipment before issuing an operating permit. Your insurer needs to know your fuel type, your suppression system and your ventilation setup. These affect your risk classification and your rate.

If you plan to serve beer, wine, cocktails or any alcoholic beverages at Texas events or private parties, the Texas Alcoholic Beverage Commission (TABC) requires liquor liability insurance as a condition of your license. Standard general liability does not cover alcohol-related claims. This is a separate policy averaging around $58 per month that specifically covers incidents where an intoxicated customer injures themselves or others after being served at your truck. Skipping it and getting caught serving alcohol without it can result in your TABC license being revoked. Having a valid food safety certification like ServSafe can also lower your premium with some carriers, as it signals lower risk to underwriters.

Getting covered is faster than most people expect. The days of calling an agent and waiting a week for paperwork are over. Before you start an online application, gather four things: your truck’s VIN number, your estimated annual gross revenue, your menu type (because fire risk classification depends on it) and the names of any cities or venues where you plan to operate. With that information ready, you can get a bindable quote in about five minutes on most platforms. General liability insurance for a food truck in Texas can be purchased entirely online with a same-day COI delivered to your inbox the moment payment goes through.

When you’re comparing options, don’t just look at the monthly price. Look at exactly what each policy includes. FLIP food truck insurance starts at around $25.92 per month and bundles GL, personal property coverage and products-completed operations into one policy. NEXT Insurance offers tiered packages with the option to add commercial auto and workers’ comp. Insureon connects you with multiple carriers and lets a licensed agent help you pick the right limits for your specific Texas operation. Always and this is important request an additional insured endorsement at the time you purchase. Venues will ask for it. Getting it added later can delay your event approval by days. You can get your free Texas food truck insurance quote at OLPolicy right now.

Choosing the right provider is just as important as choosing the right limits. The best food truck insurance providers for Texas combine fair pricing with fast COI delivery, Texas-specific underwriting knowledge and simple online management. An independent insurance agent in Texas can also help you compare multiple carriers and spot coverage gaps that a quick online purchase might miss especially if your operation is more complex.

| Provider | Starting Monthly Cost | Texas Coverage | Same-Day COI | Best For |

| FLIP | ~$25.92 | Yes includes products-completed ops | Yes | Solo operators and startups |

| NEXT Insurance | $23 – $31 | Yes Texas-tailored packages | Yes | Fast digital purchase |

| Insureon | ~$42 avg | Yes multiple carrier comparison | Yes | Comparing quotes side-by-side |

| The Hartford | Varies | Yes strong BOP options | Agent-assisted | Established multi-truck operations |

| Hiscox | Varies | Yes customizable coverage | Yes | Flexible policy needs |

| Progressive Commercial | Varies | Yes strong commercial auto bundle | Agent-assisted | Truck + auto combination |

An additional insured endorsement extends your policy’s protection to a third party the venue, event organizer or property owner that requires it. Most Texas festivals and corporate venues will hand you a vendor contract with a line that reads something like: “Vendor must name Lucy as an additional insured on their general liability policy.” Here is exactly how you handle it, step by step.

First, log into your insurer’s online portal or call your agent. Second, request an additional insured endorsement for the specific entity named in the contract use their exact legal name. Third, download the updated certificate of insurance (COI) that shows the additional insured on the declarations page. Fourth, submit that COI to the venue before their approval deadline. FLIP and NEXT both complete this in under five minutes online at no extra charge. The Hartford and Progressive may require a phone call and up to 24 hours processing time. Always double-check the venue’s required legal name even a small wording difference can get the COI rejected.

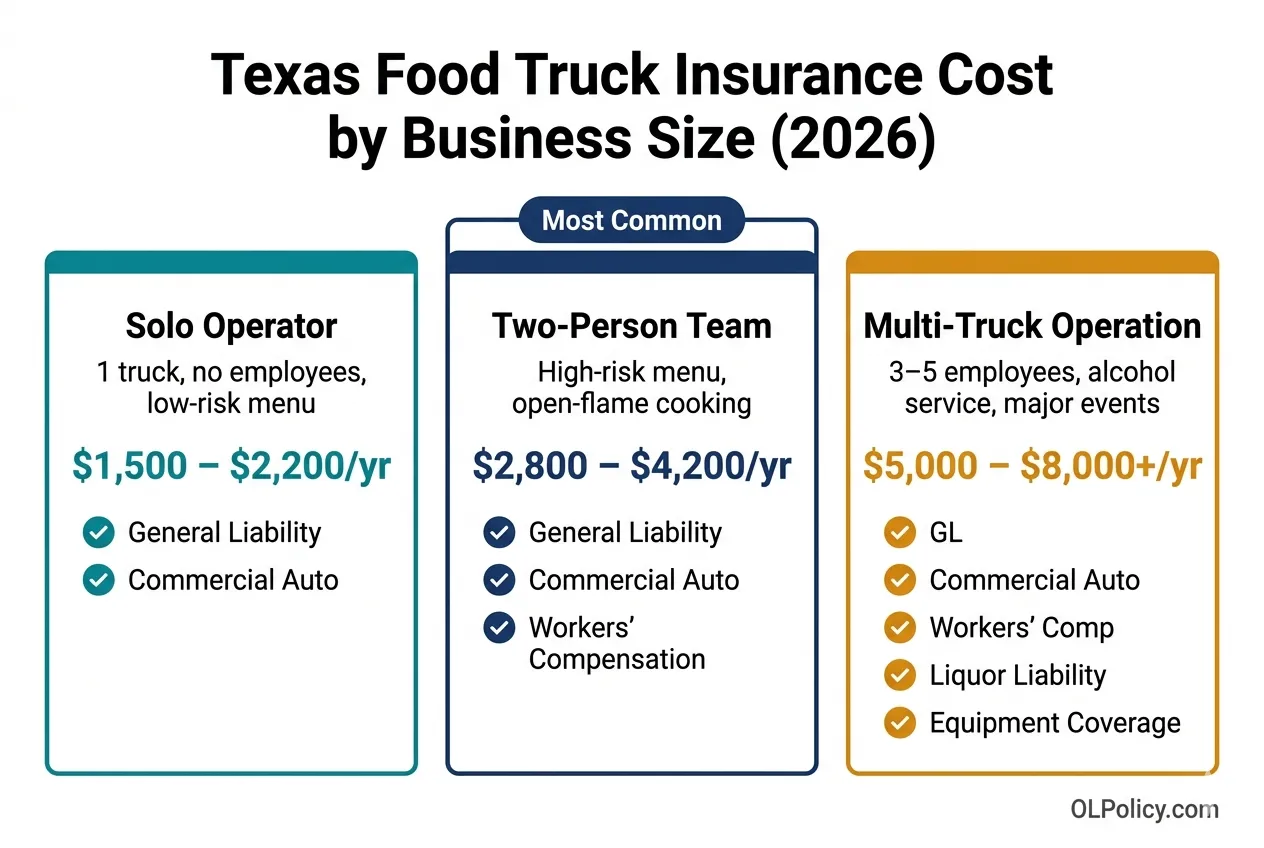

Not every food truck operation is the same. A solo operator working part-time at a single Austin farmers market has a completely different risk profile than a team of five running two trucks across major DFW events every weekend. Here is how annual insurance costs typically break down by operation size in Texas.

Solo operator one truck, no employees, low-risk menu (sandwiches, cold drinks): General liability runs $23 – $30 per month. Commercial auto adds $100 – $150 per month. Total estimated annual spend: $1,500 – $2,200.

Two-person operation one truck, high-risk menu (open-flame grilling, deep fryers): General liability runs $35 – $50 per month. Commercial auto adds $150 – $200. Workers’ compensation adds $46 – $78. Total estimated annual spend: $2,800 – $4,200.

Multi-truck operation 3 to 5 employees, alcohol service, major Texas events: A full bundle including GL, commercial auto, workers’ comp, liquor liability insurance and equipment coverage runs $5,000 – $8,000 or more annually. Events like SXSW and the State Fair of Texas may require temporary limit increases for the event period ask your insurer about event endorsements in advance.

Maria runs a gourmet grilled cheese truck in the Dallas-Fort Worth area. In the summer of 2024, she was set up at a busy outdoor food truck rally in Frisco when a customer tripped on an uneven patch of asphalt near her service window and fractured their elbow. The customer filed a claim within 48 hours. Total medical costs plus legal fees came to $57,000. Maria’s general liability policy a $1 million per occurrence plan she paid $38 per month for covered every dollar. Her out-of-pocket cost was zero beyond her deductible. Without that policy, she would have been staring down a five-figure debt that likely would have forced her to sell the truck.

“I almost skipped buying general liability because I thought nothing that bad would ever happen at my truck. Now I tell every food truck owner I meet buy the policy before you serve your first customer. It’s the best $38 I spend every single month.” Maria T., Dallas food truck owner

Is general liability insurance legally required for food trucks in Texas?

Texas doesn’t require it at the state level, but in reality, you’ll still need it to operate. Most cities, venues, and events require proof of General Liability Insurance for a Food Truck in Texas before issuing permits or allowing you to serve.

How much liability insurance does a Texas food truck need?

Most city permits require at least $1 million in coverage, while large events often expect a $2 million aggregate limit. Since the price difference is usually small, many owners start with $1M and upgrade when needed.

Can I use personal auto insurance for my food truck?

No, personal auto insurance doesn’t cover business use and claims will be denied if you’re operating a food truck. You’ll need a commercial auto policy, which is required for business vehicles in Texas.

Does general liability cover my food trailer when it’s detached?

Not by default, since coverage changes when the trailer isn’t attached to your vehicle. To stay protected, you’ll need an endorsement or a separate inland marine policy.

Can I get same-day coverage for my Texas food truck?

Yes, many providers offer same-day coverage with instant proof of insurance. You can usually go from quote to active policy in minutes, even on the day of an event.

What does a certificate of insurance (COI) show?

A COI is a simple document that outlines your coverage, including limits, policy details, and insured parties. It’s what venues and cities check to confirm you have valid General Liability Insurance for a Food Truck in Texas before letting you operate.

Running a food truck in Texas is genuinely exciting. The opportunity is real from Austin’s street food scene to Houston’s neighborhood food parks to the packed event calendars in Dallas and San Antonio. But that opportunity comes with real risk. One uncovered liability incident can wipe out months of hard work in a matter of days. General liability insurance for a food truck in Texas is the most important financial protection your business can carry. It’s affordable. It’s fast to get. And it is the difference between a bad day and a business-ending catastrophe.

Running a food truck comes with enough to handle getting the right General Liability Insurance for a Food Truck in Texas shouldn’t be one of them. Visit OLPolicy or call (866) 757-5350 and we’ll help you find coverage that actually fits your business.

Always verify specific coverage requirements directly with your city’s permit office and consult a licensed Texas insurance agent for policy guidance tailored to your operation. For official Texas insurance information, visit the Texas Department of Insurance at tdi.texas.gov. For alcohol licensing requirements, visit the Texas Alcoholic Beverage Commission at tabc.texas.gov.