Are you a Florida landscaper tired of worrying that one client accident could destroy your business overnight? You are not alone. Thousands of lawn care owners across the Sunshine State face this exact fear every single day. General liability insurance for landscaping in Florida is the single coverage that stands between you and a financially devastating lawsuit. Without it, one slippery walkway or one broken window becomes your personal problem to pay for.

Landscaping business insurance Florida protects your income, your reputation and your future. Lawn care insurance Florida is no longer optional it is the price of doing serious business. Smart contractors who carry landscaper liability insurance win better contracts, bigger clients and long-term peace of mind. This guide shows you exactly how landscaping contractor insurance works, what it costs and how to get covered today.

General liability insurance for landscaping business in Florida is the most fundamental coverage any lawn care operator can carry. At its core, it protects your business from third-party claims meaning claims filed against you by clients, property owners, or bystanders. It is not health insurance and it is not workers’ comp. It specifically covers other people and their property when something goes wrong because of your work. Think of it as a financial firewall between one bad job and your entire business.

Every serious landscaping general liability policy in Florida covers three core areas: bodily injury coverage, property damage liability and personal and advertising injury. Beyond those three pillars, it also covers your legal defense costs even when a lawsuit turns out to be completely baseless. Attorney fees alone can reach $50,000 or more in cases you ultimately win. Without a policy in place, you pay every cent of that out of pocket.

Florida presents unique risks that landscapers in other states simply do not face at the same level. Heavy afternoon thunderstorms create slippery surfaces daily. Year-round operation means more hours worked and more chances for something to go wrong. Florida’s active legal environment also means clients are more likely to pursue a liability claim settlement through the courts when accidents happen on their property. One wet sidewalk, one flying mower stone, one cracked irrigation line any of these can trigger a lawsuit that costs far more than the job was worth.

Beyond personal protection, lawn care insurance Florida is practically required to win the contracts worth having. Many Florida municipalities, HOA communities and commercial property managers legally demand a valid certificate of insurance (COI) before they allow any contractor on site. Without one, you are locked out of Florida’s most lucrative landscaping work entirely. A landscaping service insurance policy does not just protect you from disaster. It actively opens doors to higher-paying clients.

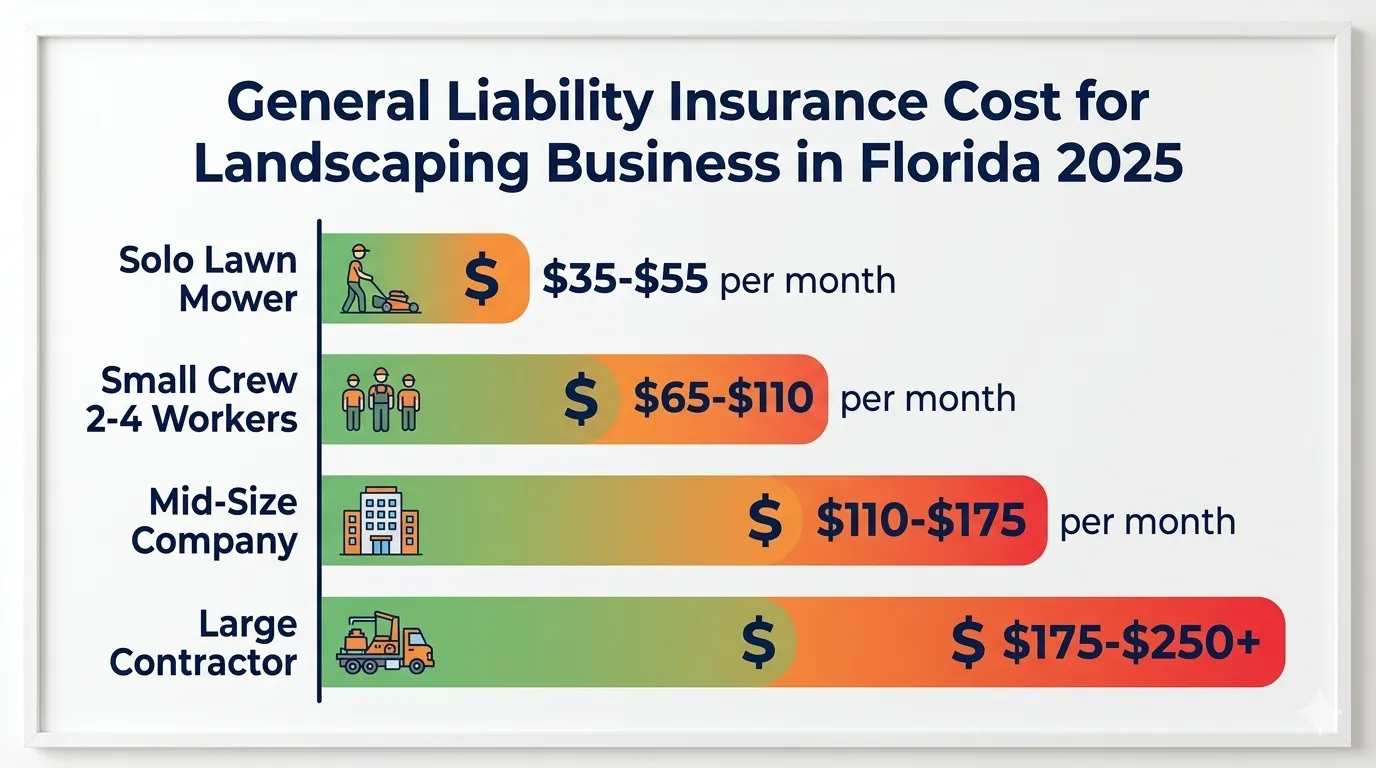

The landscaping business insurance cost Florida depends on several variables, but here are the real numbers most Florida landscapers actually pay in 2025. Solo operators with limited services typically pay between $35 and $65 per month. Small crews with broader service offerings pay closer to $65 to $110 per month. Larger landscaping companies with multiple employees and high-risk services can expect to pay $110 to $250 or more per month. Annual payment options often save Florida landscapers 8 to 12 percent compared to monthly billing cycles.

| Business Type | Est. Monthly Cost | Annual Estimate |

| Solo lawn mower | $35 – $55 | $420 – $660 |

| Small crew (2–4 workers) | $65 – $110 | $780 – $1,320 |

| Mid-size landscaping company | $110 – $175 | $1,320 – $2,100 |

| Large contractor with equipment | $175 – $250+ | $2,100 – $3,000+ |

Getting a proper landscaping insurance quote online from multiple providers remains the best way to find your actual rate. The insurance premium you pay reflects your specific risk profile not just a generic industry number. Even a 15-minute comparison session can save you $300 to $600 annually on your landscaper insurance monthly cost.

A strong landscaping liability coverage policy protects you in four primary ways. Understanding each layer helps you appreciate exactly what your monthly insurance cost is buying every single month. Most Florida landscapers are surprised to learn how much ground a single well-written policy actually covers.

Bodily injury coverage pays for medical bills and legal defense costs if someone gets hurt because of your work or your presence on their property. A client’s visitor trips over your equipment. A neighbor walks through your work zone and gets hit by debris. These are third-party claims not your injuries, but someone else’s. Your policy responds and covers costs up to your policy limits. Without this, you pay medical bills and attorney fees from your own pocket.

Property damage liability covers the cost of repairing or replacing a client’s property that your team accidentally damages. You crack a tile surround near a pool. Your mower throws a stone through a sliding door. You back your trailer into a garden wall. These incidents happen on ordinary workdays to ordinary contractors. Commercial insurance for landscapers with solid property damage liability coverage handles these bills without you writing a personal check.

Personal and advertising injury protection covers claims involving defamation, slander and certain copyright violations. If a competitor claims you copied their marketing materials or a client claims you damaged their reputation, this insurance coverage responds. Most Florida landscapers rarely trigger this protection but it matters when it does get triggered. It is a quiet but valuable layer of your overall landscaping business protection insurance.

Your legal defense costs coverage means the insurance carrier pays your attorneys, court fees and settlement costs even when the lawsuit against you is completely baseless. In Florida’s active legal environment, frivolous claims against contractors are a genuine risk. Defending yourself costs real money whether you win or lose. This may be the single most valuable feature of your entire landscaping general liability policy.

Real-World Example: A Florida landscaping crew trimming hedges near a client’s swimming pool accidentally drops a tool that cracks an expensive tile surround. Proper property damage liability coverage handles that repair bill completely. Without coverage, that landscaper pays out of pocket and loses the client relationship permanently.

Knowing your insurance policy exclusions is just as important as knowing what your policy covers. Many Florida landscapers discover painful gaps only after a claim gets denied. Understanding the limits of your landscaping service insurance policy lets you build a complete protection strategy before something goes wrong. The four most common exclusions are employee injuries, professional errors, your own tools and equipment and commercial vehicle accidents.

A standard landscaping general liability policy does not cover injuries to your own workers. That requires workers compensation insurance for landscapers a completely separate policy. In Florida, workers’ comp is legally required once your business has four or more employees, including part-time workers. Skipping it is not just risky. It can result in serious legal penalties from the Florida Division of Workers’ Compensation. Even if you only have one helper, this gap deserves immediate attention.

If your work simply fails a drainage system you designed floods a client’s yard, a retaining wall you built collapses general liability insurance will not cover the resulting damage. Professional errors fall outside the scope of a standard landscaping contractor insurance policy. They require professional liability coverage, sometimes called errors and omissions insurance. Some Florida landscapers add a professional liability insurance endorsement to their existing policy to bridge this gap affordably.

Your mower, trimmer, blower and trailer are not covered under general liability insurance for landscaping business in Florida. If someone steals your equipment from a job site or it gets damaged in transit, you bear that loss personally unless you carry tools and equipment insurance or inland marine insurance for landscapers. This coverage typically costs $15 to $40 per month. It protects everything you depend on to do your job and is one of the most overlooked gaps in a Florida landscaper’s coverage options.

Driving your truck to a job site and getting into an accident is not covered by your landscaping liability coverage. Your personal auto insurance almost certainly excludes commercial use as well. You need commercial auto insurance for landscaping business to close this gap. Florida requires it for any vehicle used primarily for business purposes. Typical cost runs $80 to $150 per month depending on your vehicle type and driving history.

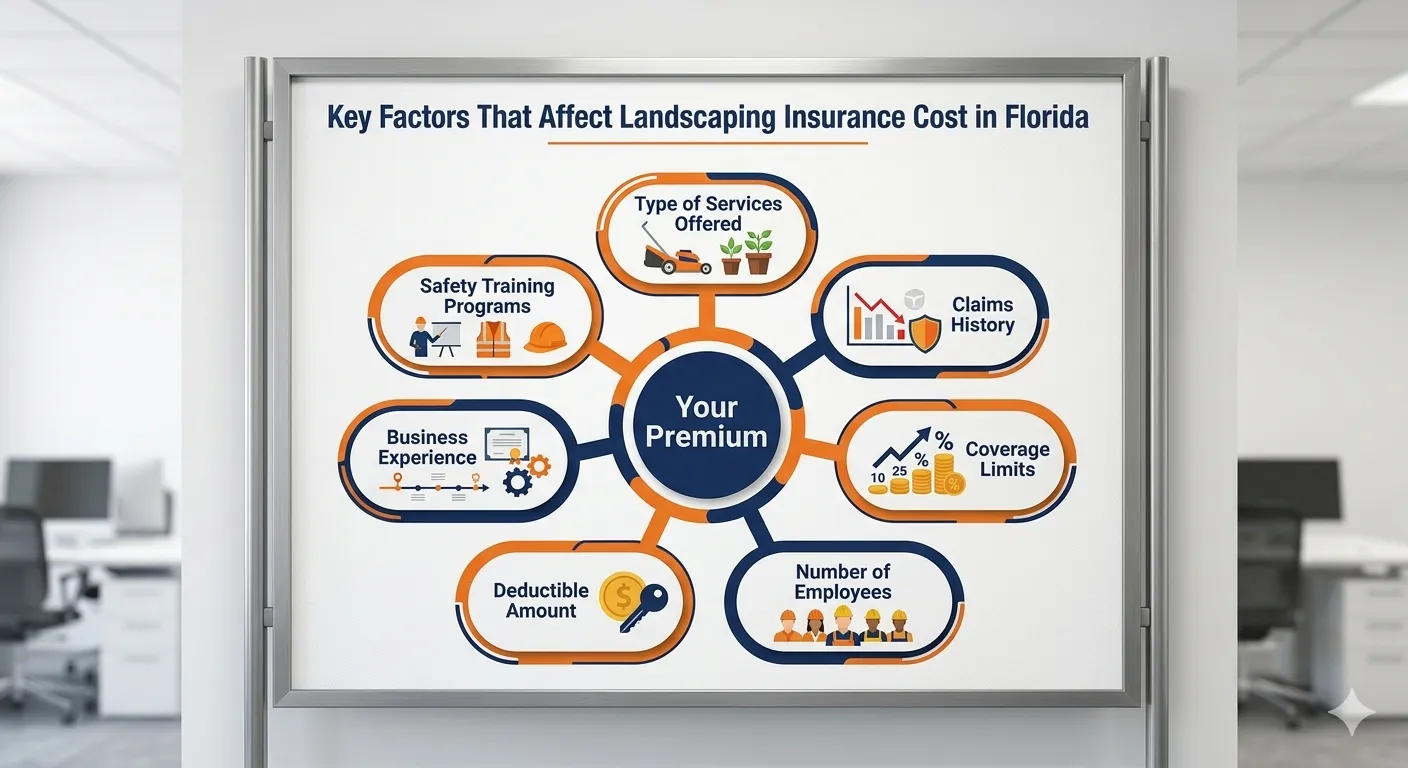

Your landscaper insurance monthly cost is not random. Insurance underwriting algorithms weigh multiple variables to calculate your specific insurance premium. Understanding what drives your rate helps you make smarter decisions when buying coverage and when managing your business day to day. The single biggest factor is the type of work you perform. After that, your claims history carries enormous weight.

| Factor | Impact on Premium |

| Tree trimming / removal services | Significant increase |

| Clean claims history (3+ years) | Meaningful decrease |

| Higher coverage limits ($2M+) | Moderate increase |

| Multiple employees | Moderate increase |

| Urban Florida location | Slight increase |

| Higher deductible chosen | Moderate decrease |

| Safety training programs | Potential decrease |

The services you offer are the most powerful driver of your insurance premium. Basic lawn maintenance mowing, edging, fertilizing carries relatively low risk. Tree trimming, stump removal and irrigation installation carry significantly higher risk. Insurers classify each service into risk tiers and price accordingly. A lawn maintenance business insurance policy for a company that only mows grass will always cost less than one for a contractor who also handles tree work. Only list the services you genuinely perform on your application. Misrepresenting your work to get a lower rate can void your coverage entirely when you need it most.

New businesses pay more because insurers are pricing uncertainty. You have no track record. After three to five clean years in business, your premiums typically decrease. Each prior claim works in the opposite direction. One small claim can raise your insurance renewal period premium by 15 to 30 percent. Multiple claims can push you toward specialty markets with significantly higher rates. Practicing strong liability risk management documenting job conditions, using proper safety gear, getting client sign-offs protects your claims record and your long-term landscaping business insurance cost Florida simultaneously.

Higher policy limits mean higher premiums but the relationship is not dramatic. Raising your coverage from $1 million to $2 million per occurrence typically adds 15 to 25 percent to your monthly cost. Your deductible amount works as a lever in the other direction. Choosing a $1,000 deductible instead of a $500 one can lower your monthly premium by 10 to 15 percent. Just make sure you could realistically pay that deductible if a claim occurred tomorrow. Setting it higher than you could afford creates a different kind of financial exposure.

Small business insurance for landscapers rarely stops at general liability alone. A truly protected Florida contractor carries several policies working together. Each one addresses a specific gap that a landscaping general liability policy does not cover. Together, they form a complete landscaping business protection insurance strategy. The good news is that bundling multiple policies under one commercial insurance provider consistently delivers meaningful discounts.

| Policy Type | What It Covers | Avg. Monthly Cost |

| General Liability | Third-party injury and property damage | $35 – $110 |

| Workers’ Compensation | Employee injuries on the job | $85 – $200+ |

| Commercial Auto | Business vehicle accidents | $80 – $150 |

| Tools & Equipment | Stolen or damaged equipment | $15 – $40 |

| Inland Marine | Equipment in transit | $20 – $50 |

| BOP (Bundled) | Liability + property combined | $80 – $175 |

Workers compensation insurance for landscapers is legally required in Florida once your business has four or more employees, including part-time workers. Skipping it is not just risky it can result in serious fines and penalties. Even below the legal threshold, an injured worker can pursue you in civil court without this coverage in place. The monthly insurance cost for workers’ comp typically runs $85 to $200 depending on your payroll and the risk level of the services your crew performs.

A business owner’s policy (BOP) bundles general liability with commercial property insurance at a discounted combined rate. It is genuinely one of the smartest moves for established Florida landscapers who own office space, store significant equipment, or have been in business long enough to accumulate real assets worth protecting. A BOP typically costs 15 to 25 percent less than buying those landscaping insurance coverage options separately. It also simplifies your insurance renewal period one policy, one renewal date, one carrier to manage.

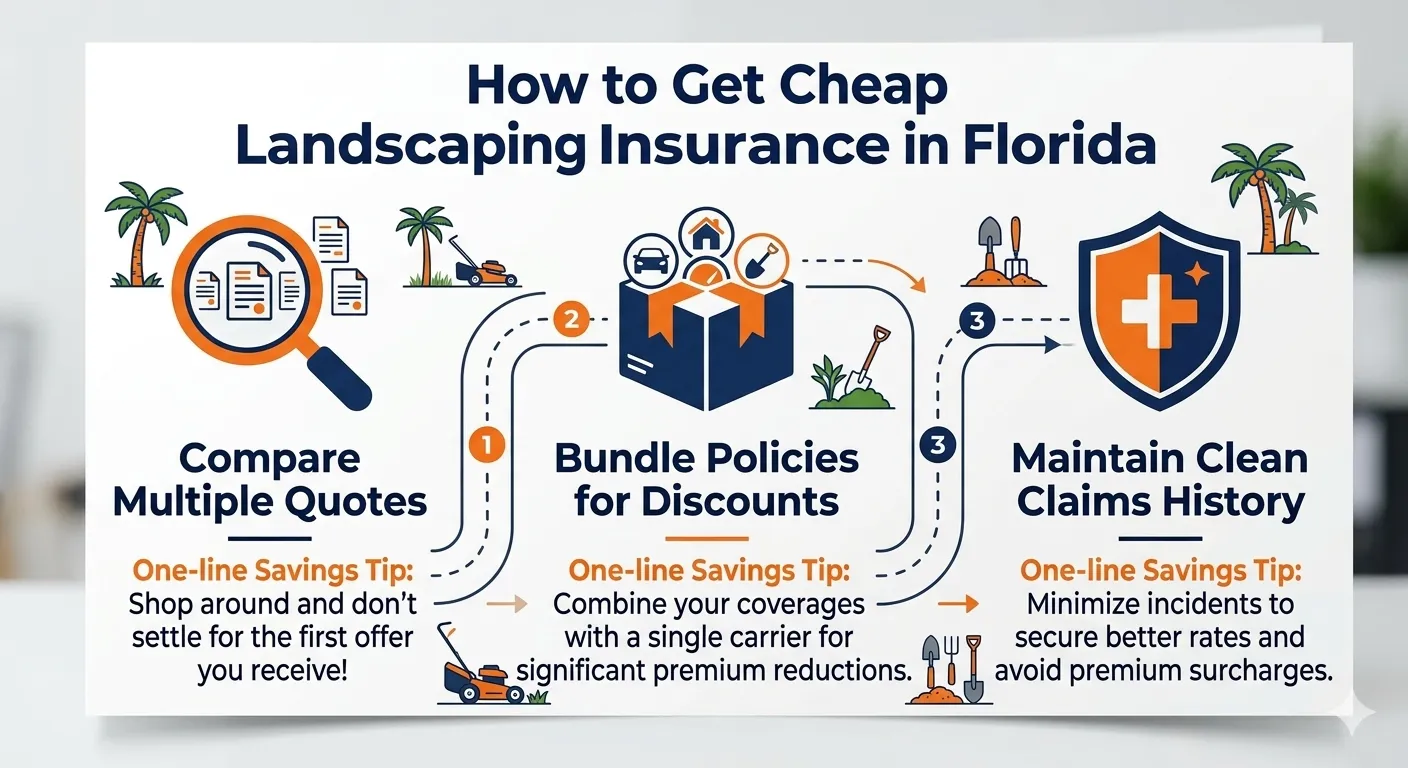

Cheap landscaping insurance Florida does not mean inadequate coverage. It means smart purchasing decisions. The market genuinely rewards shoppers. Carriers compete for your business and that competition works in your favor every time you take 15 minutes to compare options before renewing or buying a new policy.

Use platforms like Simply Business, CoverWallet, or Insureon to run insurance quote comparison results side by side. Even a 15-minute comparison session can save you $300 to $600 annually on your landscaping insurance Florida cost. Never accept the first landscaping insurance quote online you receive. The difference between the highest and lowest quote for identical coverage is often substantial.

Combining general liability insurance for landscaping business in Florida with commercial auto and tools coverage under one commercial insurance provider consistently saves 10 to 20 percent compared to buying separately. Ask every carrier explicitly about multi-policy discounts before you finalize any purchase. Most carriers offer them. Most contractors never ask. A simple question during the insurance application process can save hundreds of dollars annually.

This is the single most powerful long-term lever on your insurance premium. Every year without a claim builds your credibility with insurers. Every claim, however small, works against you at renewal. Practice proactive liability risk management document job-site conditions before you start work, use proper safety equipment and report any incidents accurately and promptly. A clean record over three to five years meaningfully reduces what you pay for affordable landscaping insurance year after year.

Starting your landscaping insurance quote online process is faster than most contractors expect. Digital carriers have made the entire insurance application process something you can complete in under 15 minutes from your phone. The key is having the right information ready before you start so your quotes are accurate rather than preliminary estimates that change later.

Before you start your landscaper insurance quote Florida process, gather these details. You will need your business legal name and structure sole proprietor, LLC, or corporation. You will need an annual revenue estimate and a complete list of services you offer. Have the number of full-time and part-time employees ready, along with any subcontractors you use regularly. Know your prior claims history if any. Finally, decide on your desired coverage limit options $1 million per occurrence is the standard starting point for most Florida landscaping businesses.

The insurance application process follows a consistent pattern across all major carriers. First, choose a carrier or comparison marketplace. Second, enter your business details accurately name, structure, revenue, services, employee count. Third, select your coverage limit options and deductible amount. Fourth, review the generated quotes carefully. Fifth, purchase the policy that best balances cost and coverage for your operation. Sixth, download your certificate of liability insurance immediately after payment. Many digital carriers activate same-day coverage you can start working on new contracts that same afternoon.

Digital carriers like Next Insurance, Thimble and biBERK offer same-day coverage as their standard practice. Complete the online application, pay your first premium and your certificate of insurance (COI) arrives by email within minutes. Traditional carriers working through brokers typically take 24 to 72 hours. If you need proof of coverage for a job starting tomorrow, digital platforms are the only realistic path for fast Florida landscaping contractor insurance activation.

Florida law does not universally mandate liability insurance for lawn care business operations for all operators. However, Florida contractor insurance requirements vary by county and municipality. Many Florida cities require proof of insurance for business licensing. Commercial clients and HOAs almost universally require a valid certificate of insurance (COI) before signing any service contract. Practically speaking, you need coverage to win the contracts worth having in Florida.

A $1 million per-occurrence landscaping general liability policy in Florida typically costs between $45 and $75 per month for a solo operator or small crew. This is the most common coverage limit options choice among Florida landscapers because many commercial clients specifically require this minimum. Annual payment usually drops this to an effective $40 to $65 per month equivalent making it genuinely modest protection against catastrophic financial exposure.

General liability insurance for landscaping business in Florida covers physical accidents someone getting hurt or property getting damaged. Professional liability covers financial losses caused by your professional advice or design decisions. For example, if you recommend a particular irrigation system that fails and floods a client’s yard, professional liability responds where landscaper liability insurance would not. The landscaping insurance coverage options you ultimately need depend on the full range of services your business provides.

Yes though your insurance premium will likely reflect that history. Insurance underwriting algorithms weigh past claims heavily. One small claim typically increases premiums 15 to 25 percent. Multiple claims can make some standard carriers decline your application, pushing you toward specialty markets with higher rates. The solution is practicing strong liability risk management going forward documented safety procedures, employee training and careful policyholder responsibilities around incident reporting all help rebuild your insurability over time.

With digital insurers like Next Insurance, Thimble, or biBERK, same-day coverage is genuinely standard. Complete the insurance application process online, pay your first premium and your certificate of insurance (COI) arrives by email within minutes. Traditional carriers working through brokers typically take 24 to 72 hours. If you need proof of coverage for a job starting tomorrow, digital platforms are clearly the better path for fast landscaping insurance quote online to active coverage turnaround.

General liability insurance for landscaping business in Florida is the single most important investment you make in your business’s long-term survival. Florida’s unique risks, legal environment and client expectations make carrying proper lawn care business liability insurance not just wise but practically unavoidable for any serious operator. The landscaping insurance Florida cost is modest. The financial exposure of going without it is catastrophic.

Start today. Gather your business details. Visit two or three landscaping insurance companies Florida operators recommend Next Insurance, Simply Business, or biBERK are excellent starting points. Request your landscaper insurance quote Florida comparisons. Choose the policy that genuinely fits your operation’s risk profile and budget. Get your certificate of liability insurance in hand. Then go build your Florida landscaping business with the confidence that one bad day will not take everything you have worked for away from you. The best insurance for landscaping contractors is the coverage that is actually there when you need it most.

“The best time to buy insurance is before you need it. The second best time is right now.” Common wisdom in the small business insurance industry.

Still searching for the right general liability insurance for your landscaping business in Florida? Stop guessing and start saving. Call (866) 757-5350 today for a free personalized quote and get covered before your next job.