Are you a contractor in Georgia struggling to figure out how much general liability insurance actually costs and worried one lawsuit could wipe out everything you have built? You are not alone. Thousands of tradespeople across the Peach State search for answers on general liability insurance for contractors in Georgia cost every single month and most of them feel overwhelmed by confusing quotes, vague policy language and wildly different price ranges. This guide cuts through all of that. It breaks down the real costs, the exact coverage details, the key money-saving tactics and the smartest way to get covered fast so you can protect your business today without overpaying for a single dollar of protection.

General liability insurance for contractors in Georgia cost is one of the most searched topics among small business owners and tradespeople across the Peach State. Whether you swing a hammer in Savannah or run a roofing crew in Atlanta, one lawsuit can wipe out everything you have built. This guide breaks down every cost, every coverage detail and every money-saving trick you need to know so you can protect your business without overpaying.

Commercial general liability insurance is the foundation of any smart business protection plan. Think of it as a financial shield. It steps in when a third party a client, visitor, or bystander suffers an injury or property loss because of your business operations. Without it, you pay every legal bill and settlement out of your own pocket.

Every contractor, tradesperson and small business owner in Georgia needs liability protection for businesses from day one. Georgia courts handle business liability lawsuits every single year. A single slip and fall injury at your job site can trigger a six-figure lawsuit before you finish your morning coffee. Small business liability coverage is not a luxury it is the smartest financial decision you will make.

A CGL insurance coverage policy is a standardized insurance contract that protects your business from third-party claims involving bodily injury coverage, property damage liability and advertising injury claims. Insurance companies across the U.S. use this format as the backbone of contractor insurance solutions. It covers incidents that happen at your job site, your office, or anywhere you conduct business.

“One lawsuit without insurance is all it takes to close a business that took a decade to build.” Independent Insurance Agents & Brokers of America

Small businesses are actually more vulnerable than large corporations. Big companies have legal teams and deep reserves. You do not. A business liability insurance policy gives you access to legal defense, settlement funds and lawsuit protection the moment a claim is filed. In Georgia, many property owners and general contractors will not even let you on a job site without proof of coverage.

Almost every trade and service business needs liability insurance for contractors or some form of business insurance policy. Here is a quick look at who needs it most:

| Business Type | Why They Need It |

| General Contractors | Job site accidents, property damage, client lawsuits |

| Roofing Contractors | High-risk work, falling debris, structural damage |

| Electricians | Fire risk, equipment failures, client injury |

| Plumbers | Water damage, flooding, third-party property loss |

| Landscapers | Equipment damage, chemical exposure, customer injury |

| Cleaning Services | Slip and fall, chemical damage, broken valuables |

| Handymen | Broad exposure across multiple trade tasks |

| Retail Businesses | Customer injuries, product liability, advertising claims |

A solid contractor insurance policy covers far more than most business owners realize. It handles the financial fallout from a wide range of real-world incidents from a client tripping over your toolbox to a copyright claim tied to your social media ad. Understanding your coverage means you will never be caught off guard when a claim lands on your desk.

Liability insurance coverage works by paying covered claims on your behalf. You pay your monthly insurance premium and in return the insurer handles legal defense costs, settlement costs and medical payments coverage when qualifying incidents occur. The right CGL insurance coverage policy can cover events that would otherwise cost you tens of thousands of dollars overnight.

Bodily injury coverage kicks in when someone who is not your employee gets hurt because of your business activity. Imagine you are a plumber in Marietta and a homeowner trips over your pipe fittings left in a hallway. They break their wrist. They sue you for $85,000. Your general liability insurance pays for their medical bills, your attorney fees and the settlement up to your coverage limits. Without it, that $85,000 comes straight from your bank account.

Property damage liability covers the cost of repairing or replacing a client’s property that your business accidentally damages. Say you are a painter in Alpharetta and you knock over a client’s $4,000 antique vase. Or your crew leaves a door open and rain damages a freshly finished hardwood floor. Your contractor liability insurance handles those customer property damage and equipment damage claims without you writing a personal check.

Advertising injury claims are surprisingly common in the digital age. If your company posts a Facebook ad that unintentionally copies a competitor’s slogan or uses a copyrighted image, you could face an advertising copyright infringement lawsuit. Personal injury liability under a CGL policy covers libel, slander and false advertising claims too. It is the kind of coverage most contractors never think about until they need it desperately.

Medical payments coverage is a goodwill feature built into most commercial general liability insurance policies. It pays a visitor’s immediate medical expenses regardless of who was at fault. Typical limits run from $5,000 to $10,000 per incident. If a client bumps their head at your shop in Augusta and needs stitches, this coverage pays right away no lawsuit required. It keeps small incidents from turning into big legal battles.

Here is a number that should get your attention. The average cost of defending a business liability lawsuit in the U.S. runs between $75,000 and $150,000 even if you win. Your general liability insurance policy covers attorney fees, court filing costs, expert witness fees and final settlement costs. That is the real power of lawsuit protection. The policy fights the battle so you can keep running your business.

No business insurance policy covers everything. Knowing the gaps in your CGL insurance coverage is just as important as knowing what it does cover. Many Georgia contractors get blindsided by uncovered claims because they assumed their GL policy handled everything. It does not and the exclusions matter enormously.

The four biggest coverage gaps are employee injuries, contractor negligence claims, vehicle accidents and damage to your own property. Each one requires a separate policy to fill the gap. Understanding these exclusions helps you build a complete risk management plan that leaves no dangerous holes in your protection.

Workers compensation insurance not general liability covers your employees when they get hurt on the job. Georgia law requires workers compensation insurance for any business with three or more employees. The Georgia State Board of Workers’ Compensation enforces this requirement strictly. Roofing and construction businesses face the steepest premiums because fall injuries are so common. If you skip this coverage, you face both civil lawsuits and state penalties.

Professional liability insurance also called errors and omissions insurance covers financial losses caused by your mistakes, bad advice, or faulty workmanship. Say an Atlanta architect miscalculates load-bearing specs and a deck collapses. General liability will not touch that claim. Errors and omissions insurance is what steps in. Design-build contractors, engineers and consultants absolutely need this separate layer of coverage in addition to their contractor insurance policy.

Your work truck is not covered by general liability insurance. Period. If your crew causes an accident on I-285 in Atlanta while hauling equipment, only a commercial auto insurance policy covers the damage and injuries. Georgia’s minimum commercial auto liability requirements are $25,000 per person, $50,000 per accident and $25,000 for property damage. Personal auto insurance explicitly excludes business use in most Georgia policies so do not assume you are covered.

Property damage liability under a GL policy only protects third-party property not yours. If a fire destroys your tools, your trailer, or your office, that is a commercial property insurance claim. Smart contractors bundle GL with commercial property coverage through a business owner’s policy (BOP), which typically saves 10–20% compared to buying each policy separately. Your tools and equipment deserve their own protection under a contractors tools and equipment insurance policy too.

General liability insurance for contractors in Georgia cost sits right around $50 to $200 per month for most small businesses and independent tradespeople. That is $600 to $2,400 per year for solid, foundational protection. The exact number depends on your trade, your revenue, your location in Georgia and a handful of other insurance pricing factors covered in the next section.

The average general liability insurance cost for contractors nationwide runs slightly lower than for Georgia-based businesses in urban markets like Atlanta or Savannah. Higher property values, denser job sites and increased court activity in metro areas push monthly insurance premium rates up. Rural Georgia contractors in areas like Valdosta or Tifton typically pay less. Understanding this geography helps you set a realistic budget.

| Business Size | Monthly Premium | Annual Premium |

| Sole Proprietor / Freelancer | $25 – $50 | $300 – $600 |

| Small Contractor (1–5 employees) | $50 – $150 | $600 – $1,800 |

| Mid-Size Construction Firm | $150 – $400 | $1,800 – $4,800 |

| Large Construction Company | $400 – $1,000+ | $4,800 – $12,000+ |

These figures represent the average general liability insurance cost for contractors across Georgia. Your actual insurance policy premium may fall above or below these ranges based on your specific risk profile.

Contractor insurance cost varies significantly by trade. Roofing contractors pay the most because their work carries the highest injury and property damage risk. Painters and cleaning businesses pay far less. Here is a practical breakdown of contractor insurance cost per month by trade in Georgia:

| Trade | Monthly Cost | Risk Level |

| Roofing Contractors | $150 – $400 | Very High |

| General Contractors | $100 – $250 | High |

| Electricians | $75 – $175 | High |

| Plumbers | $65 – $150 | Medium-High |

| Painters | $40 – $90 | Medium |

| Landscapers | $45 – $120 | Medium |

| Handymen | $40 – $90 | Medium |

| Cleaning Businesses | $30 – $65 | Low |

The $1 million liability policy is the industry standard in Georgia. Most general contractors, property managers and commercial clients require it before work begins. A $1 million liability policy typically costs $50 to $150 per month for small contractors. $2 million liability coverage which doubles the aggregate limit usually runs only $20 to $40 more per month. That small additional cost makes the jump to $2 million liability coverage a smart and easy decision for most contractors.

“A $1M/$2M policy is the minimum most Georgia general contractors will accept from subcontractors. It is the price of entry for serious work.” Georgia Licensed Insurance Broker

Several variables drive your insurance policy premium up or down and knowing them puts you in control. Insurers do not pull your rate from thin air. They run a detailed analysis of your industry risk classification, your location, your team size and your financial history. Each factor feeds into a formula that determines what you will pay for affordable contractor insurance.

Your risk management plan plays a huge role here. Contractors who document safety protocols, maintain clean claims history and operate in lower-risk counties pay significantly less than those who do not. Understanding the factors affecting liability insurance premiums gives you real leverage when you get insurance quotes and compare insurance companies.

| Risk Tier | Example Trades | Premium Impact |

| Very High | Roofing, Demolition, Structural Steel | +60–100% above base |

| High | General Contracting, Electrical, Plumbing | +30–60% above base |

| Medium | Landscaping, HVAC, Painting | +10–30% above base |

| Low | Cleaning, Consulting, Retail | Base rate |

Georgia’s geography directly affects your monthly insurance premium. Atlanta metro contractors especially those working in Buckhead, Midtown, or Sandy Springs where property values are extremely high pay more than contractors in rural South Georgia. Business location affects your exposure to high-value property damage, court costs and jury award tendencies in local courts.

Every employee you add increases your insurance policy premium. More people on a job site means more chances for a job site accident, a slip and fall injury, or a customer property damage incident. Insurers look at your total payroll amount and number of employees as direct measures of exposure. Solo operators consistently receive the most affordable contractor insurance rates.

Higher revenue signals more jobs, more job sites and more overall exposure. Insurers use business revenue as a key insurance premium driver. A Georgia contractor earning $500,000 per year pays more than one earning $100,000 even for identical trade work. Always report your revenue accurately on applications. Underreporting can give an insurer grounds to deny a claim when you need it most.

Your claims history follows you from insurer to insurer. Three or more claims in five years can push you into a high-risk insurance pool with premium rates 40–70% above standard. A clean record, on the other hand, unlocks loyalty discounts and preferred pricing. Think carefully before filing small claims. A $1,500 equipment repair claim today could cost you $4,000 in extra premiums over the next three years.

Coverage limits and deductibles are the two dials you control most directly. Higher insurance coverage limits cost more but protect you better on large projects. Higher liability insurance deductibles lower your premium but increase your out-of-pocket cost per incident. Most Georgia contractors find the sweet spot at a $500 to $1,000 deductible paired with a $1M/$2M liability insurance coverage limit.

Insurance for construction businesses and service trades varies enormously across Georgia. Comparing costs by industry gives you a realistic benchmark before you get insurance quotes. The table below reflects average annual contractor insurance cost figures across the most common trades and service industries in the state.

Use this table as your starting reference when you compare general liability insurance quotes online. Actual rates from your chosen carrier may vary based on your specific risk profile, claims history and business location.

| Industry | Monthly Cost | Annual Cost | Risk Level |

| General Contractors (Georgia) | $100 – $250 | $1,200 – $3,000 | High |

| Roofing Contractors | $150 – $400 | $1,800 – $4,800 | Very High |

| Electricians | $75 – $175 | $900 – $2,100 | High |

| Plumbers | $65 – $150 | $780 – $1,800 | Medium-High |

| Landscaping Businesses | $45 – $120 | $540 – $1,440 | Medium |

| Handyman Services | $40 – $90 | $480 – $1,080 | Medium |

| Cleaning Businesses | $30 – $65 | $360 – $780 | Low |

| Retail / E-commerce | $25 – $60 | $300 – $720 | Low |

General contractor insurance and insurance for construction businesses carry the highest premiums in Georgia and for good reason. Construction job sites are dynamic, dangerous environments where job site accidents happen regularly. General liability insurance for construction companies must account for heavy equipment, multiple subcontractors and high-value property exposure on every single project.

Roofing contractors face the steepest rates in Georgia’s construction sector. Working at height means bodily injury coverage claims are frequent and expensive. A roofing crew in Gwinnett County can expect to pay $150 to $400 per month. A contractor insurance program specifically designed for roofers including contractors pollution liability insurance for chemical sealants and coatings gives the most comprehensive protection.

Liability insurance for small businesses in the cleaning sector is among the most affordable in Georgia. Cleaning companies deal with customer property damage risks broken valuables, chemical damage to surfaces and occasional slip and fall injuries in commercial spaces. A solo house cleaner in Savannah might pay as little as $30 per month for solid small business liability coverage. Commercial cleaning companies serving office buildings pay more due to higher foot traffic and property value exposure.

Landscaping business insurance sits in the medium-risk category in Georgia. Landscapers use heavy equipment, handle chemicals and work in residential neighborhoods where a wayward stone from a mower can shatter a window or injure a child. Liability insurance for contractors in the landscaping space must also account for contractors pollution liability insurance when pesticides and herbicides are part of the service offering. Annual premiums typically run $540 to $1,440 for most Georgia landscaping companies.

Handyman liability insurance occupies a tricky spot in the insurance market. Because handymen perform multiple types of work plumbing, electrical, carpentry, painting their industry risk classification is broader than a single-trade contractor. Some contractor insurance providers restrict coverage to specific tasks listed on the policy. Always read your contractor insurance policy carefully to confirm that every service you offer is covered. An uncovered task during a claim is just as bad as having no insurance at all.

Retail businesses and e-commerce sellers often overlook liability insurance for small businesses entirely a costly mistake. Georgia-based Amazon sellers and Etsy shop owners face product liability exposure every time a customer buys something. If your product causes injury or property damage, a business liability insurance claim can follow quickly. Small business liability coverage for retail runs just $25 to $60 per month arguably the most cost-effective risk transfer available to any small business owner.

General liability insurance is the foundation but it is not the whole building. A complete risk management plan for Georgia contractors includes several additional policies working together. Think of your business insurance policy as an ecosystem, not a single product. Each policy fills a specific gap that the others cannot cover.

The right combination of contractor insurance solutions protects your people, your vehicles, your professional reputation and your digital assets. Contractor insurance providers across Georgia offer package deals and contractor insurance programs that bundle multiple policies at a discount. Always ask about bundling options before buying policies individually.

Workers compensation insurance is mandatory in Georgia for any business with three or more employees under the Georgia State Board of Workers’ Compensation. For construction companies, the average cost runs $1 to $3 per $100 of payroll. A roofing company with $200,000 in annual payroll could pay $2,000 to $6,000 per year for workers compensation insurance alone. This is non-negotiable Georgia regulators audit construction sites regularly and penalties for non-compliance are severe.

Commercial auto insurance protects your business vehicles, your drivers and any property damage or injuries caused in an accident. Georgia requires minimum liability limits of $25,000 per person, $50,000 per accident and $25,000 for property damage on commercial vehicles. Your personal auto policy excludes business use. Every contractor truck, van, or trailer used for work purposes in Georgia needs a separate commercial auto insurance policy or endorsement to stay legally protected.

Professional liability insurance better known as errors and omissions insurance covers financial losses caused by mistakes, oversights, or negligent advice in your professional services. Design-build contractors, home inspectors, consultants and architects in Georgia need this coverage in addition to their CGL insurance coverage. A design error that costs a client $50,000 in repairs is not covered by GL but errors and omissions insurance handles it directly.

Builder’s risk insurance covers structures currently under construction a coverage gap that standard general liability insurance does not fill. If a fire destroys a half-built home in Decatur, builder’s risk insurance pays for the materials, labor and reconstruction costs. Many Georgia mortgage lenders and property owners require active builder’s risk insurance before a construction loan is approved or a project breaks ground. Project-based policies are available for single jobs while annual policies work better for contractors building multiple homes per year.

Cyber liability insurance is the fastest-growing coverage category in the contractor market. Georgia contractors increasingly use cloud-based project management tools, digital contracts and online payment systems all of which create data breach exposure. A ransomware attack that locks your business files or exposes client data can cost $50,000 to $200,000 to resolve without cyber liability insurance. Monthly premiums start as low as $25 for small contractors a very small price for very significant protection.

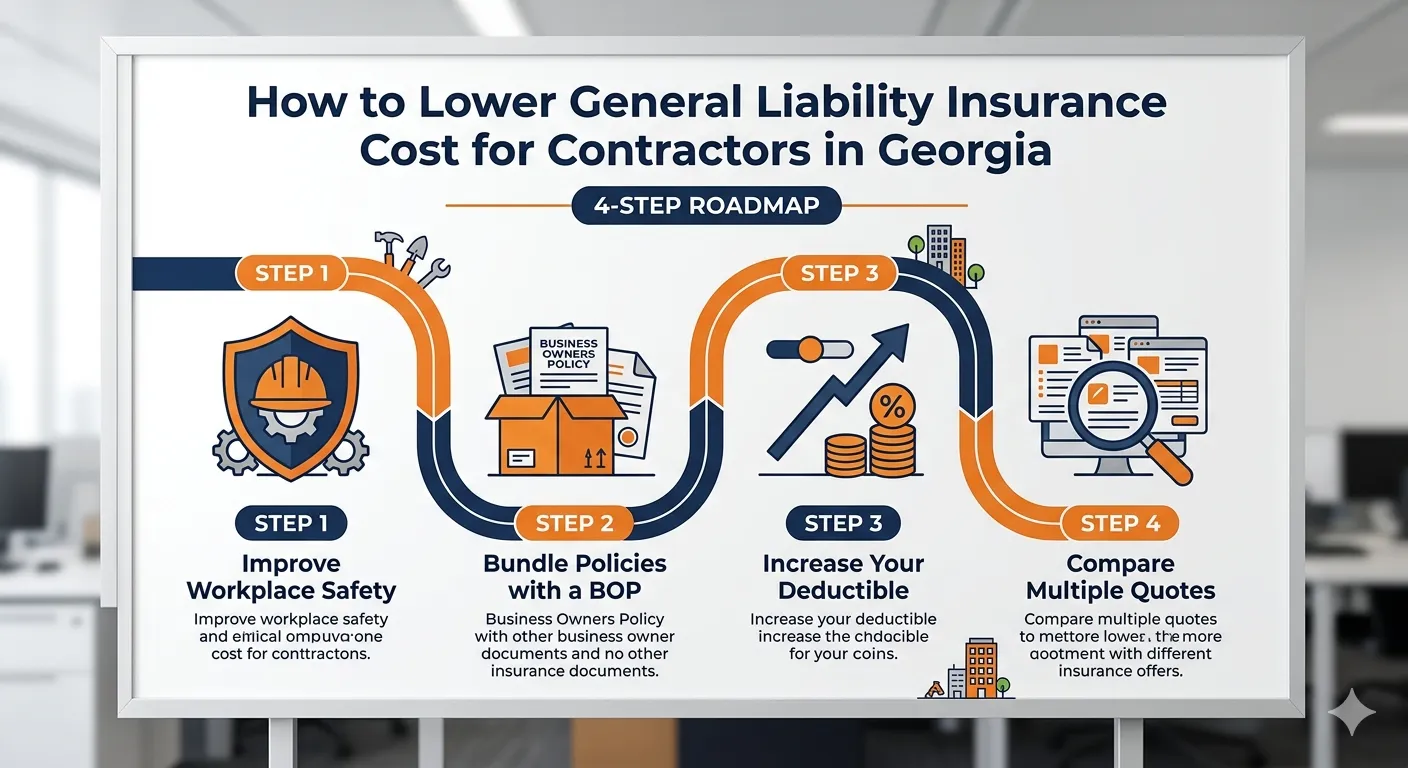

Fortunately, you have real options to trim your insurance policy premium without sacrificing the protection you need. Smart Georgia contractors treat their insurance cost the same way they treat material costs something to be actively managed, not passively accepted. A few deliberate moves can save you hundreds of dollars per year on affordable contractor insurance.

The best savings come from combining three strategies: reducing your actual risk profile, bundling policies intelligently and shopping aggressively across contractor insurance providers. These are not tricks they are the same tactics insurance professionals use when buying coverage for their own businesses. Use them.

Insurers reward low-risk operations with lower monthly insurance premium rates. Document your safety protocols in writing. Conduct regular toolbox talks on your Georgia job sites. Maintain OSHA compliance records. A safety record that shows zero job site accidents over three to five years qualifies you for preferred pricing tiers at most major contractor insurance providers. Your safety culture is literally worth money and it protects your workers too.

A business owner’s policy (BOP) combines commercial general liability insurance with commercial property coverage into one discounted package. Bundling typically saves 10–20% compared to buying each business insurance policy separately. The BOP is ideal for Georgia contractors who have a physical office, a storage yard, or equipment kept at a fixed location. Ask every contractor insurance provider you contact whether a business owner’s policy makes sense for your operation.

Raising your liability insurance deductible from $500 to $1,000 can reduce your insurance policy premium by 10–15% immediately. Increasing it further to $2,500 generates even bigger savings. This strategy only makes sense if you maintain a cash reserve to cover the higher out-of-pocket cost when a claim occurs. Do not raise your deductible beyond what you can realistically afford to pay at short notice that defeats the entire purpose of having liability claim protection.

Never accept the first quote you receive. Contractor insurance cost for identical coverage can vary by 30–50% between different carriers in Georgia. Use independent brokers who specialize in the Georgia contractor market. Compare quotes through platforms like Next Insurance, Simply Business and Insureon. These platforms let you compare general liability insurance quotes online in minutes and often generate an instant insurance quote you can act on the same day.

Getting affordable contractor insurance in Georgia is faster and easier today than ever before. Many contractor insurance providers offer complete online insurance application processes that take under 10 minutes. You can go from zero coverage to a printed certificate of insurance in a single afternoon sometimes within the hour. Here is exactly how the process works.

Buy business insurance online through a reputable platform or work with a licensed Georgia independent agent who knows the contractor market. Either path gets you covered. The online route is faster. The agent route is better for complex operations with multiple employees, subcontractors, or specialized trade exposures. Choose the path that fits your timeline and your risk complexity.

Every insurer will ask for your business name, trade type, Georgia business license number, years in operation, annual revenue, payroll amount and employee count. If you hold a Georgia contractor’s license, have that number ready. Accurate information is critical errors on your online insurance application can create coverage gaps or grounds for claim denial later. Be thorough and honest from the start.

The standard contractor liability insurance coverage limits in Georgia are $1 million per occurrence and $2 million aggregate. Most general contractor insurance requirements from GCs and property owners match these numbers exactly. For larger commercial projects, you may need excess liability coverage or umbrella liability insurance that extends your total protection to $5 million or more. Discuss project-specific requirements with your client before finalizing your insurance coverage limits.

Top contractor insurance providers serving Georgia contractors include Next Insurance, Hiscox, The Hartford, Travelers and Markel. Always check AM Best financial strength ratings before committing. An insurer rated A or better has the financial stability to pay large claims reliably. Compare insurance companies on price, coverage breadth, claims responsiveness and customer reviews from other Georgia contractors not just on premium alone.

Once you select your contractor insurance policy, purchase it and immediately download your certificate of insurance (COI). The business insurance certificate proves your coverage to clients, GCs and Georgia permitting offices. Store your certificate of insurance digitally in your email, your cloud storage and on your phone. Job site supervisors and property managers request it constantly. Having it instantly accessible keeps your projects moving without delay.

Georgia contractors ask the same questions about general liability insurance costs, requirements and processes every day. These answers cut straight to the facts no fluff, no runaround. Whether you are buying your first contractor insurance policy or reviewing your current coverage, these answers give you the clarity you need to make confident decisions.

Liability insurance for contractors does not have to be confusing. The more you understand about business liability insurance requirements, insurance coverage limits and the buying process, the more control you have over what you pay and what you get. Let us tackle the biggest questions head on.

General liability insurance is not state-mandated for all Georgia contractors, but most clients and general contractors require it before you can start any job.

General liability insurance for contractors in Georgia cost for a $1 million policy typically runs $50 to $150 per month, depending on your trade and revenue.

Yes business liability insurance premiums are fully deductible as a business expense under IRS Publication 535, so consult your CPA to claim the deduction.

Many online contractor insurance providers like Next Insurance offer same-day coverage with an instant certificate of insurance (COI) download right after purchase.

General liability insurance for contractors in Georgia cost is one of the most important investments your business will ever make. The monthly premium is small. The protection it provides is enormous. One uncovered lawsuit, one job site accident, one slip and fall injury any of these can cost more than a decade’s worth of premiums in a single afternoon.

Build your risk management plan starting with solid commercial general liability insurance. Layer in workers compensation insurance, commercial auto insurance and builder’s risk insurance as your business grows. The right contractor insurance policy does not have to be complicated or expensive you just need the right people in your corner.

Ready to protect your Georgia contracting business today? The team at OL Policy specializes in affordable contractor insurance built specifically for tradespeople and small business owners across Georgia. Get your free quote in minutes at olpolicy.com or call us directly at (866) 757-5350 we make it simple to get covered fast, so you can get back to work with total peace of mind.

Georgia State Board of Workers’ Compensation

Georgia Secretary of State Contractor Licensing

IRS Publication 535 Business Expenses

NAIC Consumer Insurance Information

Next Insurance Contractor Quotes

Simply Business Compare Quotes

Insureon Small Business Insurance