Are you trying to figure out how much is general liability insurance for a small business in Ohio and feeling overwhelmed by confusing quotes, vague answers, and prices that seem to vary wildly? You are not alone. Thousands of Ohio small business owners search for this exact answer every single day, and most end up more confused than when they started. This guide cuts through all of that noise.

The general liability insurance cost Ohio small businesses face typically ranges between $25 and $125 per month. Your final number depends on your industry, how many employees you have, and how much coverage you need. Whether you run a cleaning company in Columbus, a landscaping crew in Cleveland, or a consulting firm in Cincinnati, this complete 2026 guide gives you real numbers, real comparisons, and a clear path to affordable business insurance Ohio owners can actually use. From understanding what commercial general liability insurance Ohio covers to learning how to slash your Ohio business insurance premiums, every answer you need is right here.

General liability insurance protects your Ohio business when someone outside your company gets hurt or their property gets damaged because of your work. It pays for legal defense costs, medical bills, and settlements so you don’t have to drain your savings. Think of it as the foundation of your entire business protection plan.

Every Ohio business big or small faces real risks daily. A customer trips on your wet floor. A contractor accidentally breaks a client’s window. These things happen fast. Small business liability insurance Ohio owners rely on it to stay financially safe when life throws curveballs.

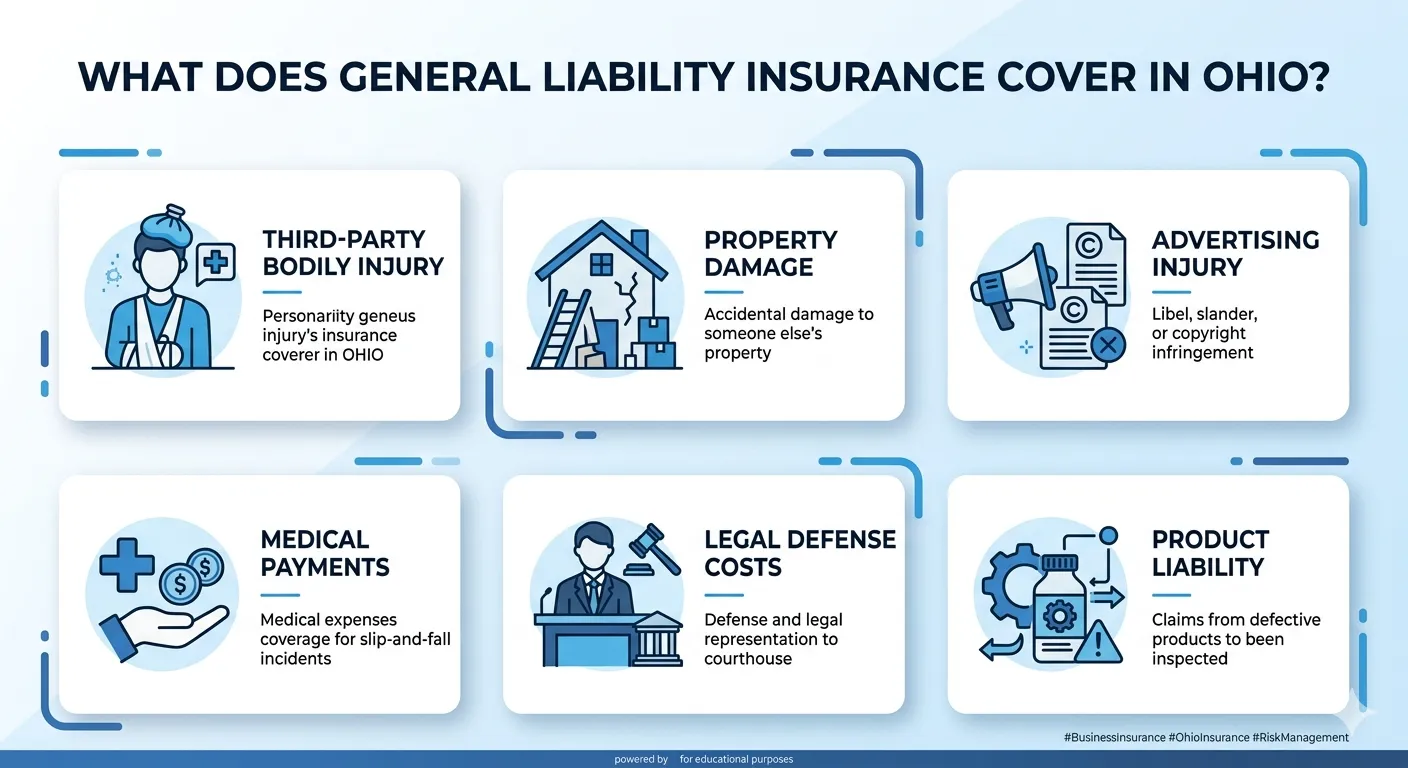

Commercial general liability insurance (CGL) covers four main areas that matter most to business owners. First, it handles third-party bodily injury claims when someone gets hurt at your business location or because of your work. Second, it covers property damage claims if you or your employees accidentally damage someone else’s property during normal business operations.

Third, CGL covers advertising injury claims things like accidental copyright infringement or slander in your marketing materials. Fourth, it pays legal defense costs even if a lawsuit against you turns out to be completely false. Here is a quick overview:

| Coverage Area | Real-World Example |

| Third-party bodily injury | Customer slips and falls in your store |

| Property damage claims | You crack a client’s floor during installation |

| Advertising injury claims | Competitor sues you over a copied tagline |

| Medical payments | Visitor needs stitches at your job site |

| Legal defense costs | Attorney fees for a negligence lawsuit |

| Product liability coverage | Customer gets hurt using your product |

Here is a hard truth. A single customer injury lawsuit can cost your small Ohio business $50,000 to $150,000 in legal fees alone before any settlement. Most small businesses simply cannot absorb that kind of hit without folding completely. Business liability insurance for small businesses exists precisely to prevent that nightmare scenario.

Ohio has no state law forcing most businesses to carry general liability coverage. However, clients, landlords, and licensing boards frequently demand a certificate of insurance (COI) before they’ll work with you. Without one, you lose contracts. Liability insurance for startups Ohio owners are building is not just smart it’s often the price of entry into the marketplace.

The average cost of general liability insurance in Ohio falls between $300 and $1,500 per year for most small businesses. That breaks down to roughly $25 to $125 per month. However, your actual Ohio general liability insurance rates depend heavily on what you do, how big your operation is, and how much coverage you choose to carry.

Understanding the cost of business insurance in Ohio helps you budget smarter. Most low-risk businesses think consultants, photographers, or software developers sit at the lower end of that range. High-risk trades like contractors or landscaping businesses routinely pay more. The average liability insurance for small business owners in Ohio lands around $42 per month, according to data from top carriers.

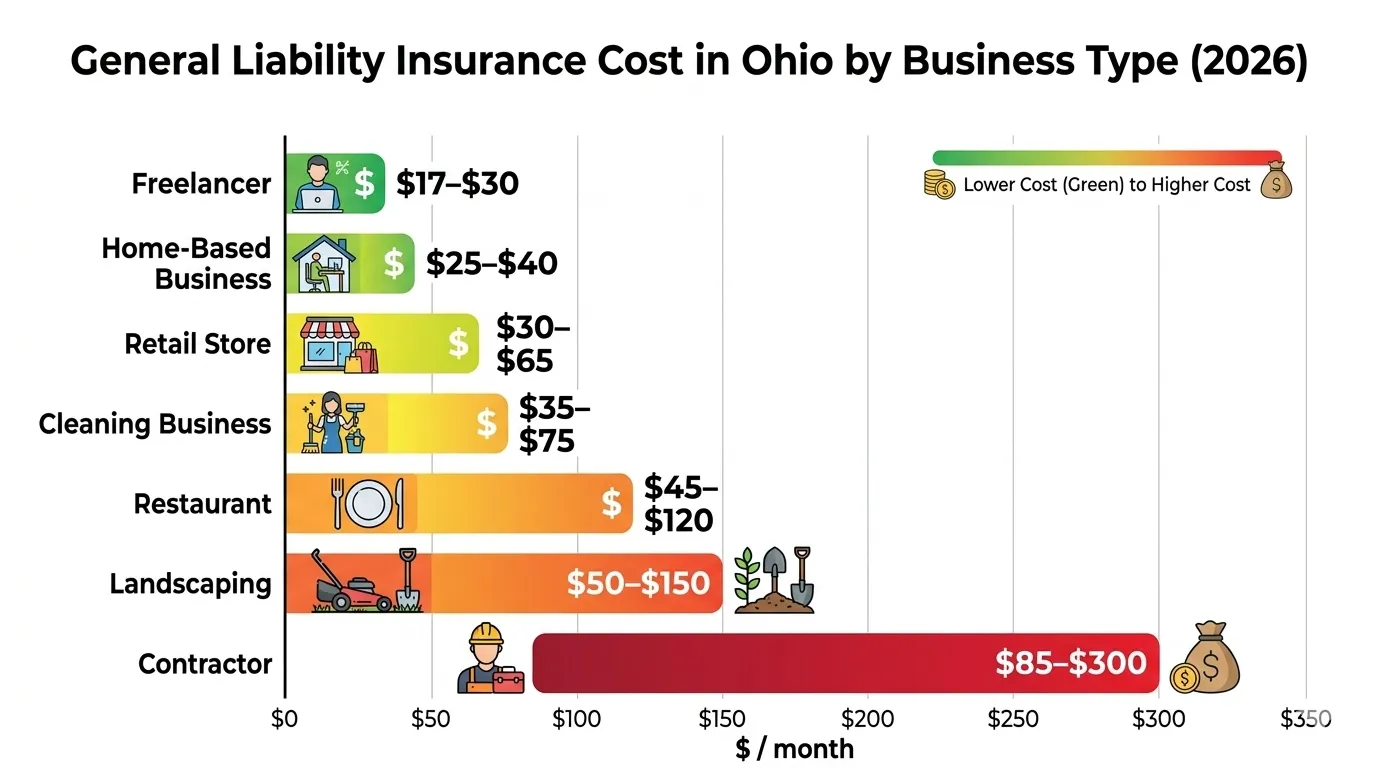

The monthly cost of liability insurance Ohio business owners pay varies widely based on industry and size. Below is a practical breakdown you can use as a starting benchmark when shopping for general liability insurance quotes Ohio providers offer:

| Business Type | Monthly Cost | Annual Cost |

| Freelancer / Solo Consultant | $17 – $30 | $204 – $360 |

| Home-Based Small Business | $25 – $40 | $300 – $480 |

| Retail Store (low risk) | $30 – $65 | $360 – $780 |

| Cleaning Businesses | $35 – $75 | $420 – $900 |

| Restaurants | $45 – $120 | $540 – $1,440 |

| Landscaping Businesses | $50 – $150 | $600 – $1,800 |

| Contractors | $85 – $300 | $1,020 – $3,600 |

The average general liability premium Ohio small businesses pay annually ranges from $400 for very low-risk operations to well over $5,000 for high-risk contractors with large crews. Most businesses fall somewhere in the middle. Ohio small business insurance rates have remained relatively stable in recent years, with modest increases tied to inflation in legal and medical costs.

To give you a real-world sense of scale, consider this. A solo fitness trainer running private sessions pays around $400–$600 yearly. A janitorial services company with five employees pays $900–$1,500. A general contractor managing multiple job sites could easily pay $3,000–$6,000+ annually. The general liability policy cost Ohio businesses face truly depends on the risk they bring to the table.

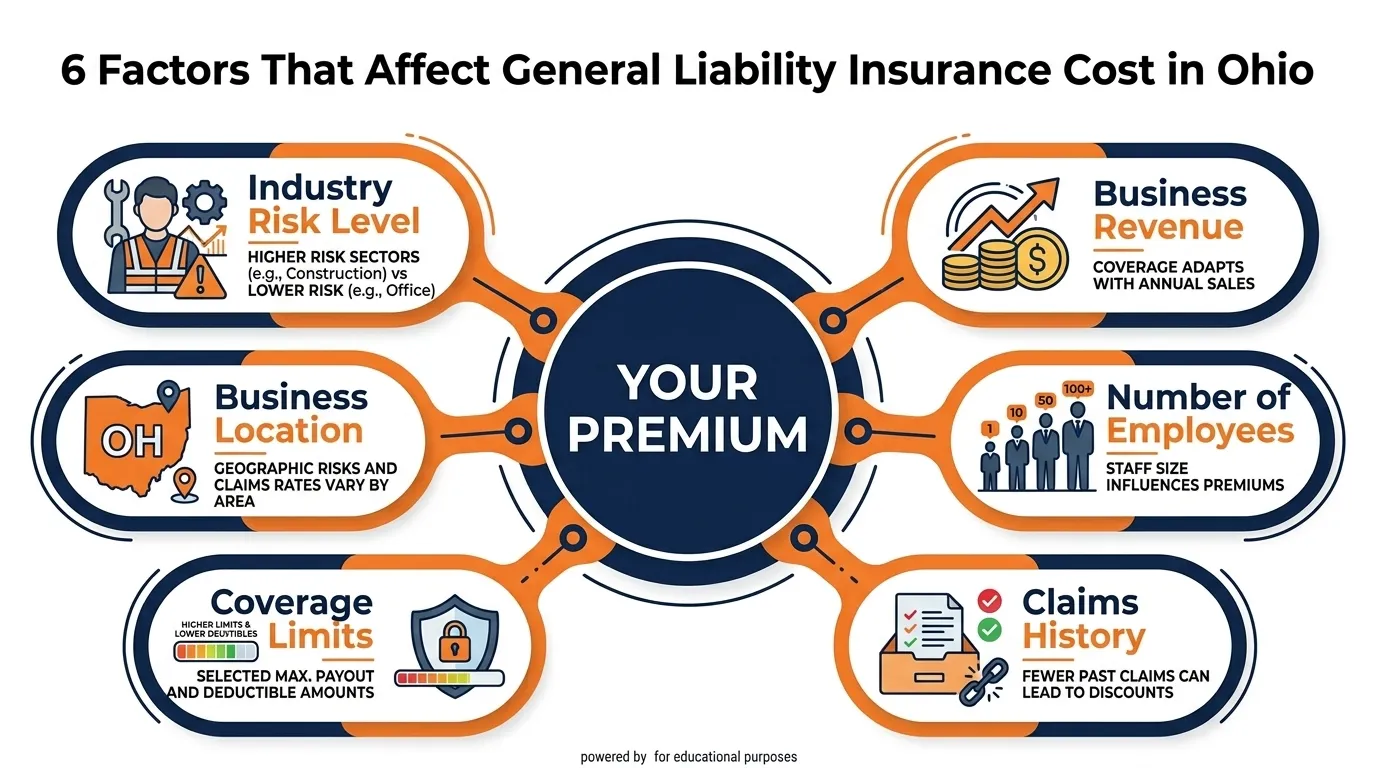

Insurers do not pick your premium out of thin air. They use a precise formula based on multiple risk factors tied directly to your business. Knowing what affects general liability insurance premiums Ohio carriers calculate helps you understand your quote and potentially lower it.

Every factor below feeds into your final Ohio business insurance premiums. Some you can control. Others you cannot. Either way, knowing them puts you in a stronger negotiating position when you shop for affordable business insurance Ohio carriers provide.

Your industry classification code is the single most influential factor in your premium. Insurers assign every business a classification based on historical claim data for that trade. A software developer working remotely carries almost no physical risk. A roofing contractor working 30 feet off the ground is a completely different story.

High-risk industries construction, tree trimming, demolition pay the most because claims happen more often and cost more to settle. Low-risk industries like consultants or photographers pay significantly less. Your industry code is essentially your risk reputation with every insurance carrier.

Your annual revenue tells insurers how much exposure your business creates in the marketplace. A business earning $1 million annually interacts with far more customers, contracts, and job sites than one earning $80,000. More activity means more chances for something to go wrong.

Business size also matters in terms of physical footprint. A larger operation typically means more locations, more equipment, and more moving parts for insurers to price. This is why Ohio commercial insurance cost rises predictably as businesses grow. It is not personal it is pure math from an underwriter’s perspective.

Every employee you add expands your liability exposure. Your team represents your business in the field, in client spaces, and on the road. The more people working under your name, the more chances exist for accidents. Insurers factor in your payroll amount and headcount directly when calculating your premium.

A solo landscaping operator in Akron pays far less than a landscaping company with eight crew members driving company trucks daily. The difference can be $600 versus $2,500 annually for similar coverage limits. Managing your team well keeps your Ohio small business insurance cost under control over time.

Your claims history works exactly like your driving record works for car insurance. One serious claim can raise your premium by 20–40% at renewal. Two claims within three years? Some carriers will non-renew your policy entirely. A clean record often qualifies you for preferred pricing and loyalty discounts.

Start documenting every safety measure you take. Keep incident logs. Train your staff properly. These habits build the clean record that translates directly into cheap general liability insurance Ohio business owners with good histories enjoy at renewal time.

Most small businesses carry a $1 million per occurrence / $2 million aggregate general liability policy. Bumping up to $2M/$4M provides stronger protection but raises your premium. Dropping to $500K/$1M saves money but leaves gaps that clients may reject.

Your deductible is the amount you pay out-of-pocket before insurance kicks in. A $500 deductible means higher monthly premiums. A $2,500 deductible drops your premium noticeably. The right balance depends on your cash reserves. General liability insurance coverage limits are not one-size-fits-all decisions.

Even within Ohio, business location in Ohio affects your rate. Urban areas like Columbus, Cleveland, and Cincinnati carry higher premiums than rural counties. Dense populations mean more foot traffic, more potential claimants, and local court systems that historically award higher settlements.

Local factors like crime rates, building codes, and municipal lawsuit trends all feed into how insurers price liability coverage for Ohio businesses in specific ZIP codes. If you operate in multiple cities, expect underwriters to price your policy based on your highest-risk location.

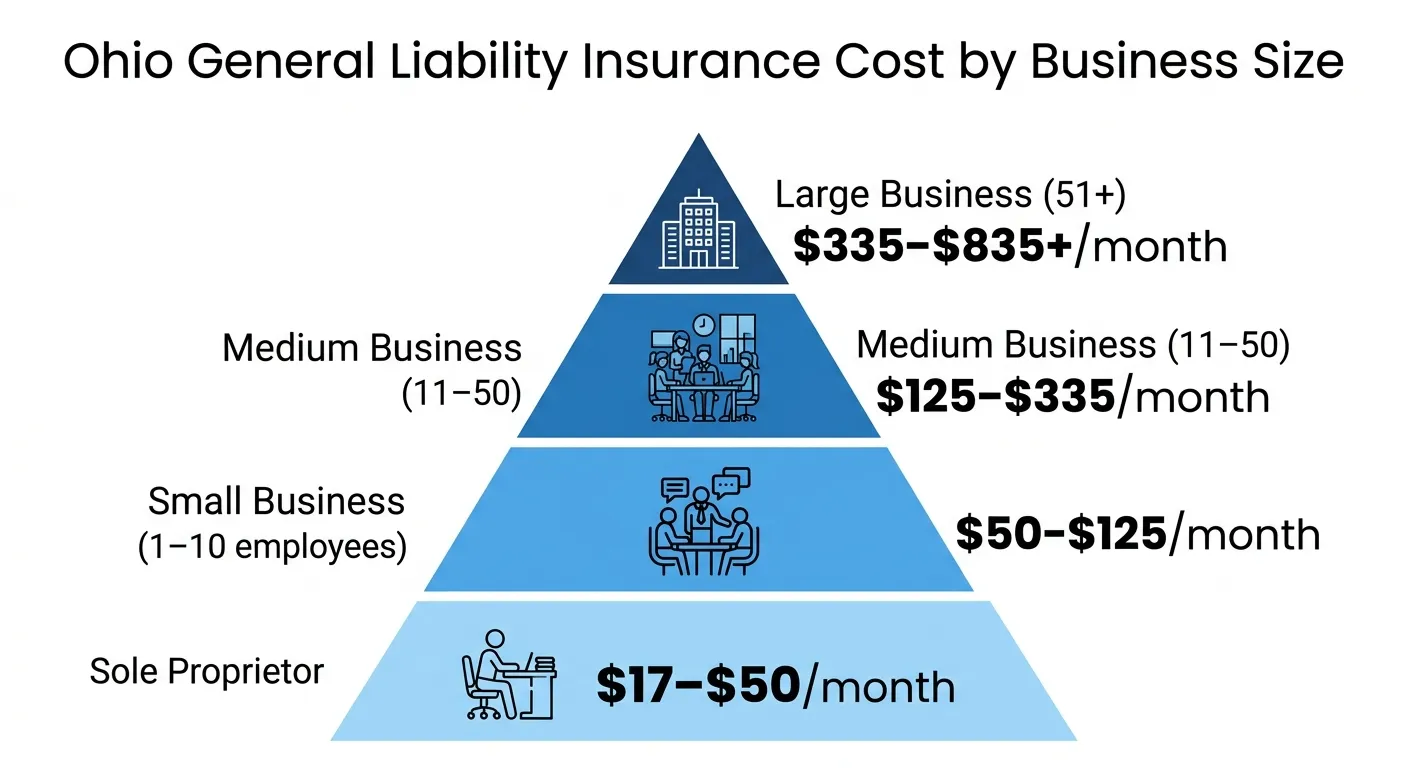

Business size creates dramatic differences in Ohio small business insurance cost. The table below gives you a realistic picture of what Ohio businesses at different stages typically pay for standard commercial general liability insurance Ohio carriers offer:

| Business Size | Employees | Monthly Cost | Annual Cost |

| Sole Proprietor | 0 | $17 – $50 | $204 – $600 |

| Small Business | 1 – 10 | $50 – $125 | $600 – $1,500 |

| Medium Business | 11 – 50 | $125 – $335 | $1,500 – $4,000 |

| Large Business | 51+ | $335 – $835+ | $4,000 – $10,000+ |

Sole proprietors running low-risk businesses enjoy the most affordable business insurance Ohio rates available. A freelance photographer or independent consultant operating from home can often find solid coverage under $30/month. There is almost no reason for a solo professional to go uninsured given how accessible these rates are today.

Medium and large businesses face more complex pricing. They often layer a base commercial general liability insurance (CGL) policy with an umbrella liability insurance policy on top to fill coverage gaps above standard limits. This layered approach is standard practice for Ohio businesses with significant assets, multiple locations, or government contracts requiring higher general liability insurance coverage limits.

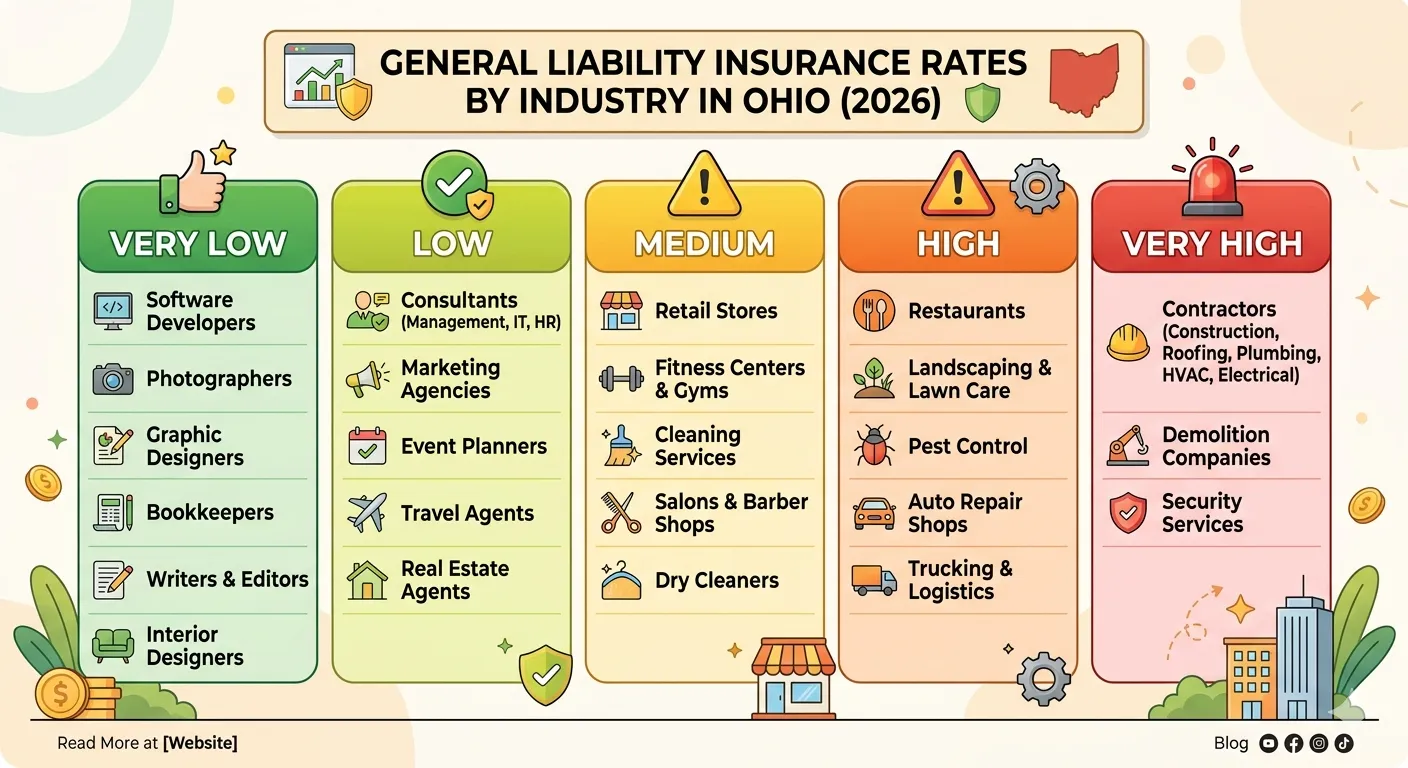

Industry is destiny when it comes to insurance pricing. The cost of liability insurance for contractors Ohio is dramatically higher than what an office-based consultant pays for the same coverage limits. Here is a comprehensive industry-by-industry breakdown of Ohio general liability insurance rates across the most common small business categories:

| Industry | Avg. Monthly | Avg. Annual | Risk Level |

| Contractors / Construction | $85 – $300 | $1,020 – $3,600 | Very High |

| Restaurants | $45 – $120 | $540 – $1,440 | High |

| Landscaping Businesses | $50 – $150 | $600 – $1,800 | High |

| Cleaning / Janitorial | $35 – $75 | $420 – $900 | Medium |

| Retail Stores | $30 – $80 | $360 – $960 | Medium |

| Fitness Trainers | $25 – $60 | $300 – $720 | Medium |

| Consultants / Professionals | $17 – $45 | $204 – $540 | Low |

| Software Developers | $17 – $40 | $204 – $480 | Very Low |

| Photographers | $20 – $40 | $240 – $480 | Very Low |

Contractors pay the highest general liability insurance cost Ohio rates because their work creates constant physical risk. Heavy equipment, structural changes, and multiple subcontractors on a single job site create layered liability. A framing carpenter who accidentally causes a fire during a renovation can face claims exceeding $500,000.

Cleaning businesses and janitorial services sit in the middle range. They work inside clients’ properties regularly, handling expensive belongings and slippery surfaces. One broken antique or one slip-and-fall accident on a freshly mopped floor creates serious exposure. Fortunately, cheap general liability insurance Ohio cleaning companies can find starts around $35/month making it genuinely accessible for even the smallest operations.

Ohio does not legally require most businesses to carry general liability insurance. However, that statement needs important context. While the state itself may not mandate it, dozens of other requirements from licensing boards to client contracts effectively make it non-negotiable for operating in the real world.

Understanding business insurance requirements in Ohio protects you from licensing penalties, contract disqualification, and personal financial exposure. The three most commonly required coverage types are workers’ compensation, commercial auto insurance, and liability coverage tied to specific contracts or licenses. Each serves a distinct protective purpose.

Ohio takes workers’ compensation insurance seriously and it handles it differently from most states. Nearly every Ohio employer with one or more employees must carry workers’ comp coverage. Ohio runs a state-funded system through the Ohio Bureau of Workers’ Compensation (BWC). Private workers’ comp is not available here. You buy through the state or qualify as a certified self-insurer.

Failure to maintain coverage triggers serious consequences. The Ohio Bureau of Workers’ Compensation can assess penalties, issue stop-work orders, and hold business owners personally liable. The penalty for non-compliance can reach double the premium amount you should have paid. Getting compliant is far cheaper than getting caught uninsured.

Ohio requires all vehicles personal or commercial to carry minimum auto liability coverage. For business vehicles, the state requires at least $25,000 per person / $50,000 per accident for bodily injury plus $25,000 for property damage. These are minimums, not recommendations. Most business advisors push Ohio companies to carry significantly higher limits.

Commercial auto insurance matters because personal auto policies almost universally exclude business use. If your employee drives a company van to a job site and causes an accident, your personal policy won’t cover it. Commercial auto liability limits Ohio businesses should carry depend on vehicle type, cargo, and how frequently employees drive for work.

Many Ohio licensing requirements across specific trades demand proof of general liability insurance before issuing or renewing a license. Ohio contractors, electricians, plumbers, and HVAC technicians frequently face this requirement at the municipal or county level. Commercial property landlords almost always require tenants to carry active coverage.

Contract liability requirements from corporate clients and government agencies often demand $1M, $2M, or even $5M in general liability limits. Showing up without a certificate of insurance (COI) matching those requirements means losing the contract period. This reality is why liability insurance for startups Ohio entrepreneurs are building matters from day one.

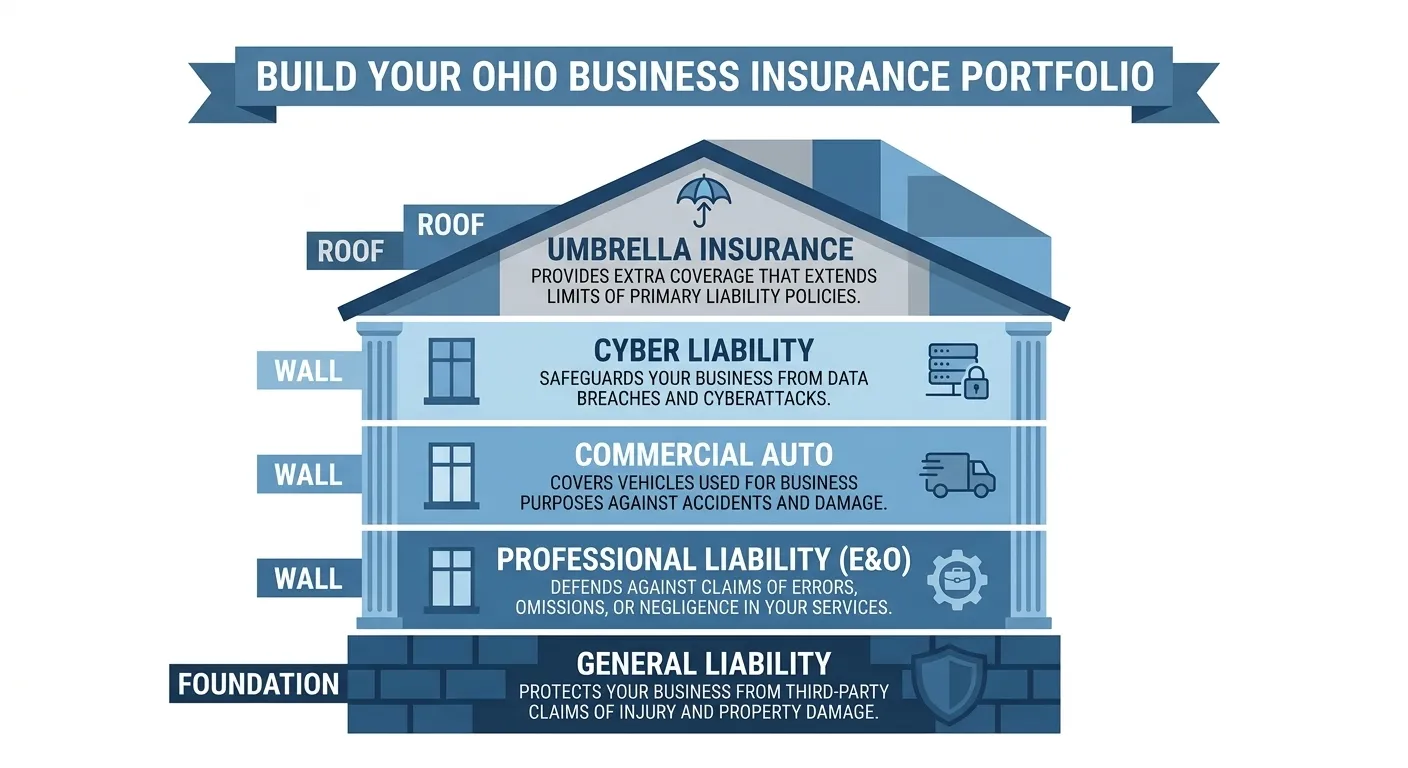

General liability is the foundation but smart Ohio business owners build on top of it. Depending on your industry, operations, and growth stage, several other policies fill critical gaps that commercial general liability insurance (CGL) simply does not address.

Think of your business insurance portfolio like building a house. General liability is the foundation. Everything else professional liability insurance, cyber liability insurance, umbrella liability insurance forms the walls, roof, and security system. You need all the pieces working together for real protection.

A business owner’s policy (BOP) bundles commercial general liability insurance with commercial property coverage into one affordable package. It is designed specifically for small-to-medium businesses. The savings are real BOPs typically cost 10–20% less than buying each policy separately.

For example, an Ohio retail store owner paying $600/year for general liability alone might pay just $900/year for a BOP that also covers $100,000 in business property. That is phenomenal value. Ohio small business insurance rates for BOPs are competitive, and virtually every major carrier offers them.

Professional liability insurance also called errors and omissions insurance (E&O) covers claims arising from professional mistakes, bad advice, or missed deadlines. General liability does not cover this exposure at all. If a consultant gives flawed strategy advice that costs a client $200,000, only an E&O policy pays for the defense and settlement.

Consultants, accountants, real estate agents, marketing agencies, IT professionals, and software developers all need this coverage. Errors and omissions insurance (E&O) typically costs $500–$2,000/year for most Ohio professionals a small price given the exposure it eliminates.

Commercial auto insurance deserves emphasis here as a standalone need beyond the legal minimum. Personal auto policies have a business-use exclusion that most owners don’t discover until after a claim gets denied. If any vehicle touches your business operations deliveries, client visits, hauling equipment you need dedicated coverage.

Landscaping businesses, cleaning businesses, mobile food vendors, and delivery services face the highest commercial auto exposure. A single at-fault accident involving a company vehicle can trigger third-party bodily injury and property damage claims exceeding your minimum state coverage quickly. Carrying $500,000 to $1M in commercial auto liability is standard practice for Ohio businesses with vehicles on the road daily.

Cyber liability insurance is no longer optional for most Ohio businesses. Cybercrime targeting small businesses has skyrocketed and small companies are the preferred target because they typically have weaker defenses. If you store customer data, process credit cards, or use any cloud-based systems, a breach exposes you to notification costs, regulatory fines, and third-party lawsuits.

The average cost of a small business data breach now exceeds $200,000. Most small businesses never recover from a hit that large. Cyber liability insurance covers forensic investigations, customer notification, credit monitoring services, regulatory penalties, and liability claim settlements from affected customers.

Umbrella liability insurance extends the limits of your existing policies when a major claim exhausts them. Imagine a serious accident depletes your $1M general liability limit and you still face $800,000 in additional damages. Your umbrella policy absorbs the overflow. Without it, that $800,000 comes directly from your business assets.

Ohio businesses in high-risk industries contractors, restaurants, event venues benefit most from umbrella coverage. An additional $1M in umbrella coverage typically costs only $500–$1,500/year on top of your base policies. For the protection it provides, it is one of the highest-value insurance purchases available to business liability coverage Ohio owners can make.

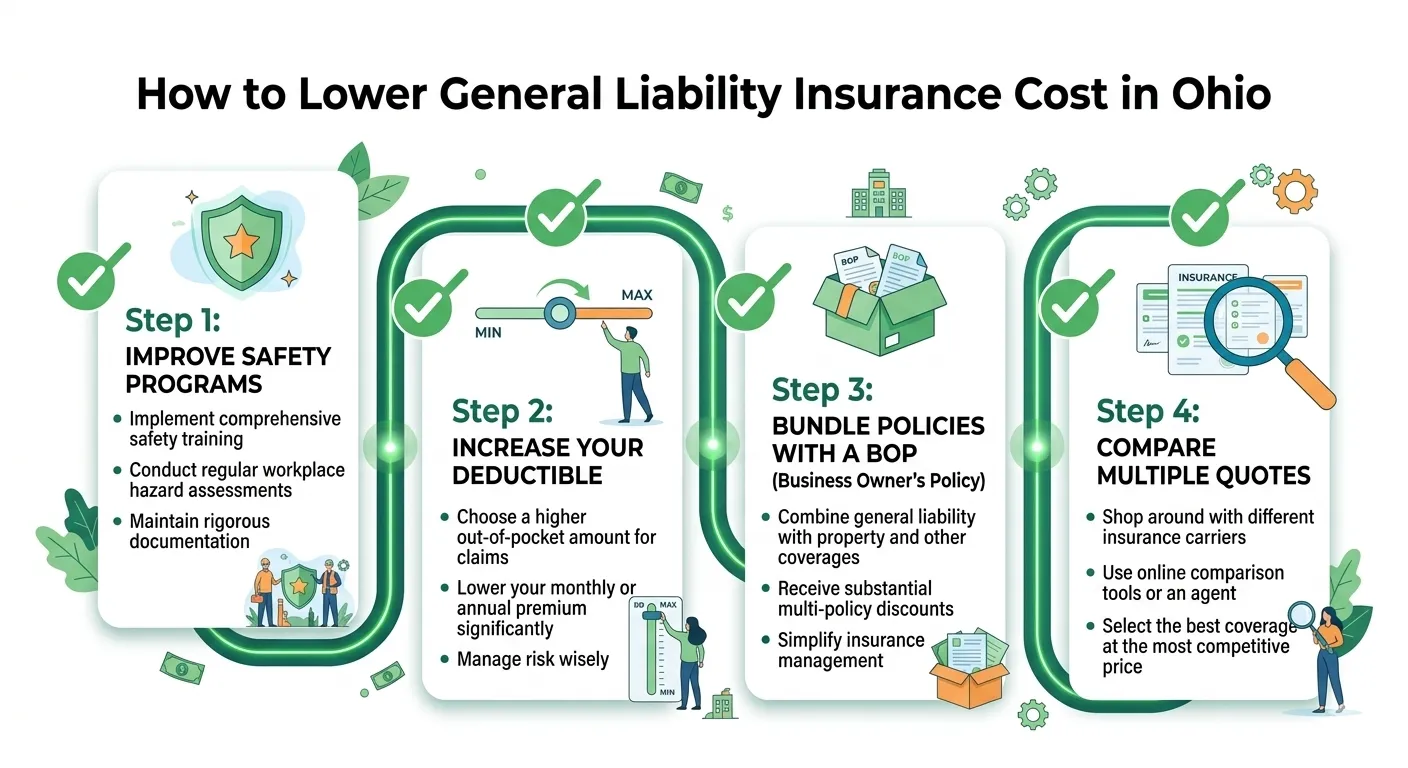

Nobody wants to overpay for insurance. The good news is that how to lower general liability insurance cost Ohio business owners pay is largely within your control. Smart risk management, smart policy choices, and smart shopping all move the needle significantly.

These strategies work together. Combine two or three of them and you can realistically reduce your Ohio business insurance premiums by 20–40% without sacrificing meaningful protection. Every dollar saved on premiums is a dollar that stays in your business.

Insurers price risk. Reduce your risk and your premium follows. Implementing documented safety training programs, installing security systems, maintaining clean job sites, and establishing clear incident reporting procedures all signal lower risk to underwriters. Some Ohio carriers offer formal safety credits discounts up to 10% for businesses with verifiable safety protocols.

A landscaping business that requires helmets, steel-toed boots, and annual equipment training for every employee is statistically less likely to file a third-party bodily injury claim. Insurers know this. Document everything. Keep training records. When your Ohio licensing requirements or carrier asks for proof of your risk management program, having it ready earns you better pricing.

Raising your deductible is one of the fastest ways to lower your general liability insurance cost Ohio small businesses pay. Moving from a $500 deductible to $1,000 or $2,500 can reduce your annual premium by 10–25%. The trade-off is simple: you absorb more cost if a claim occurs, but you pay less every month whether a claim happens or not.

This strategy works best for businesses with a clean claims history and solid cash reserves. If you have gone three or more years without a claim, increasing your deductible is essentially free money you’re paying lower premiums while accepting a risk you statistically don’t encounter.

Combining general liability with commercial property coverage in a business owner’s policy (BOP) delivers real, consistent savings. But the bundling strategy goes further. Many Ohio insurers offer multi-policy discounts when you add commercial auto insurance, workers’ compensation insurance, or cyber liability insurance to the same carrier relationship.

Carriers like The Hartford, Nationwide, and Cincinnati Insurance all strong players in Ohio reward loyalty and multi-policy relationships with meaningful discounts. Consolidating your coverage reduces administrative headaches too. One renewal date, one carrier contact, one bill. Simplicity has financial value when managing Ohio commercial insurance cost across multiple policy types.

This one step alone can save Ohio business owners hundreds of dollars annually. General liability insurance quotes Ohio carriers provide for identical coverage can vary by 30–50% across different companies. The carrier that was cheapest last year may not be cheapest today. Markets shift. Your business profile changes. Always shop at renewal.

Use independent brokers or online marketplaces like Insureon, CoverWallet, or Simply Business to get competing small business insurance quote Ohio providers generate simultaneously. These platforms pull quotes from multiple best general liability insurance companies in Ohio at once saving you hours of research. The cheapest liability insurance companies Ohio business owners find are rarely the ones they started with.

How much does general liability insurance cost per month in Ohio?

Most Ohio small businesses pay between $25 and $125 per month for general liability insurance, with the overall average landing around $42/month for a standard $1M/$2M policy.

Is general liability insurance required in Ohio?

Ohio state law does not require most businesses to carry general liability insurance, but licensing requirements, commercial leases, and client contracts frequently make it a practical necessity.

How much is a $1 million liability insurance policy?

A standard $1 million per occurrence / $2 million aggregate policy costs most Ohio small businesses between $400 and $1,500 per year, depending on industry and risk level.

What does general liability insurance not cover?

General liability insurance does not cover employee injuries, professional mistakes, business vehicle accidents, or data breaches those require separate policies like workers’ comp, E&O, commercial auto, and cyber liability insurance.

Still wondering how much general liability insurance costs for your small business in Ohio? You’re not alone and we’re here to make it simple. Call us today at (866) 757-5350 or visit olpolicy to get a free, no-obligation quote tailored just for your business.